Monday 10th May 2021

"The market always misprices growth and its sustainability".

It was roughly ten years ago now, that Nick Griffin, chief investment officer at Munro Partners, marched into the Melbourne office of Sornem Private Wealth and gave a presentation on how a bookstore would one day turn into a superstore.

We thought he was crazy.

Remember when Amazon sold only books? It’s hard to imagine that it was that same company that exists today. All before Jeff Bezos hatched up a plan for Amazon to become more than just a bookstore and more than just an e-commerce store. Amazon went on to become the biggest internet-based e-commerce company in the world, selling everything via its one-stop shop.

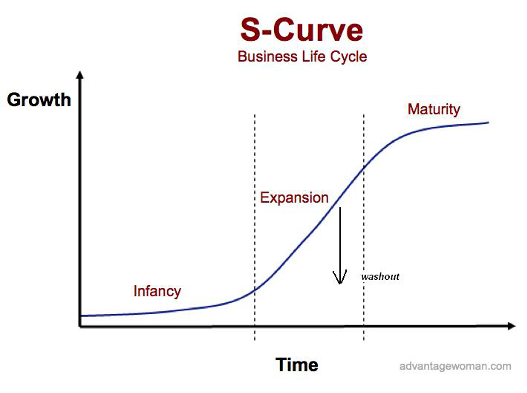

Griffin would say, “This is the S-Curve moment.”

A growth-investing phenomenon in which disruption and dislocation help boost a company’s earnings and share price has driven results for growth managers like Munro in recent years. Linear profit growth assumptions almost never work with a growth company. When a growth company “beats” broker forecasts, it does so in spectacular fashion. Once the herd catches onto it, it’s off to the moon. Earnings accelerate, and the share price skyrockets. The key to this is finding those companies about to experience the belly of the ‘S curve’:

“The S-curve beats the ‘macro’ every time,” Griffin says.

And he’s right. Instead of worrying about inflation, interest rates, or any other macro-economic driver, it is the ability to see structural change occurring and pick out a winner that stands to benefit most from this disruption. “It is these companies that will deliver the strongest returns over the long term, regardless of the economic backdrop or point in the cycle.”

Investing ahead of the curve is where the money is at. But how does one invest ahead of the curve?

- First, identify where and how a company aims to generate profit.

- Check and see whether there are signs that the company is on the right track. For example, let’s look at a company that makes money from selling a product to a customer. Check and see if it has identified the right target customer. Its target market must be in desperate need for this new product and must be ready to buy.

- Identify competitive advantages – such as the networking effect, disruptive cutting-edge technology, or increasing switching costs that knock-out competition.

Munro’s investment philosophy has three key factors that have proven important in generating strong long-term returns:

- Earnings growth is what drives stock prices. It’s simple. Companies that stand to make more money every year, will experience greater growth in their share price. It makes sense.

- Sustained earnings growth is worth more than cyclical growth. Consistent earnings growth that is devoid of cyclical factors, and greater than its peer group, will be valued higher than otherwise.

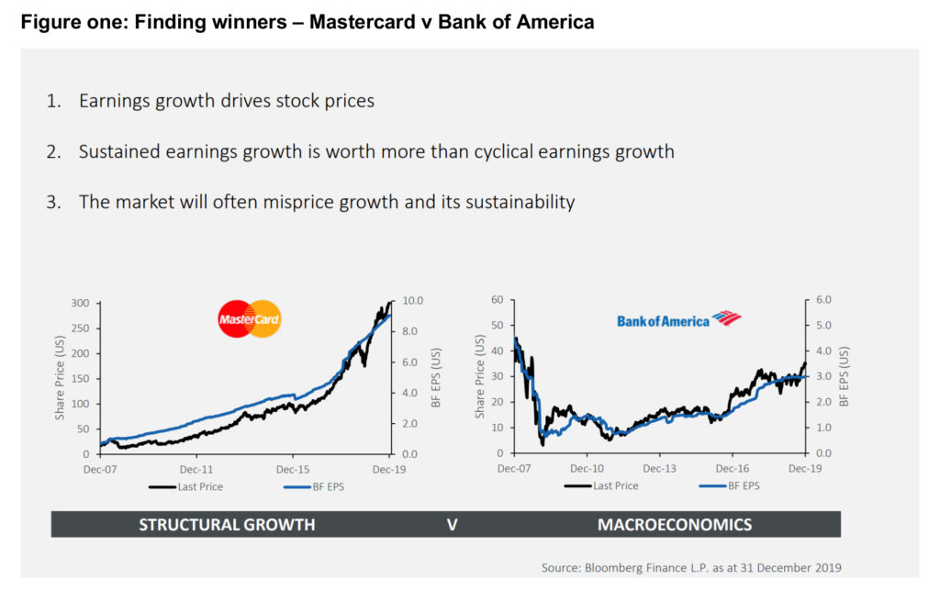

- The market often misprices growth and its sustainability. Griffin often uses his MasterCard and Bank of America example. On the left is MasterCard. What you’ll notice is that tboth share prices follow forward 12 month rolling forward EPS expectations. On the right there isn’t a lot of value to add in where the share price will track, because Bank of America relies on macro indicators such as interest rates, regulation etc. But MasterCard is benefiting from a simple shift from physical to digital cash. This is a structural shift that is creating sustained earnings over the long term.

Griffin says that people are more aware of this structural shift, but the market is incapable of pricing it in because it is accelerating. “The market always misprices growth and its sustainability” and the reason that happens is because most of the market believes in mean reversion. The key is to find a situation where mean reversion doesn’t exist.

Griffin says, “In every game there are few winners, and a lot of losers.”

The big disruptive S-curves of our lifetime have been disruption and e-commerce, which is growing at 13% per year. The winner from that shift was Amazon. In internet disruption it was Google. Griffin believes decarbonisation, cloud computing, digital payments and semiconductors are just a few areas that are in the early phases of structural shift.

“Our job is to find the structural change and pick the winner,” he says.

Ishan is an experienced journalist covering The Insider Adviser publication.