Monday 6th May 2024

The rapid rise of residential mortgage funds

From residential and commercial backed mortgage securities, to whole loans and government issued bonds, there is a range of investment products that are backed by housing mortgages.

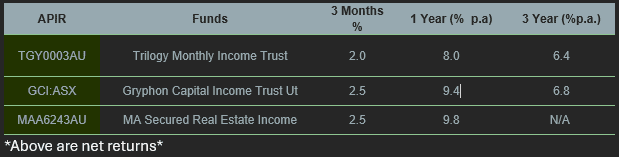

Mortgage funds have emerged as a particularly attractive investment option under current economic conditions characterised by fluctuating inflation and interest rates, which have predicated uncertain economic forecasts. As at 31 March, 2024 three mortgage fund managers have emerged due their standout performances over the one and three year periods.

Mortgage funds offer investors exposure to a range of securities, which can include:

Residential mortgage-backed securities (RMBS): These are securities backed by mortgages on residential properties. RMBS allows investors to benefit from the repayment of principal and interest from a pool of home loans, with the performance of these securities being closely tied to the health of the housing market and the credit quality of borrowers. Various government initiatives to support the housing market such as subsidies or tax incentives can further bolster the performance of these securities, thus enhancing the potential returns.

Commercial mortgage-backed securities (CMBS): Like RMBS but backed by mortgages on commercial properties such as industrials and office buildings, retail space or hotels. CMBS tend to have higher yields than residential securities but also carry a higher risk due to its sensitivity to the economic conditions that affect the commercial real estate market.

Whole loans: Mortgage funds may also invest directly in whole mortgage loans. These investments involve purchasing the original mortgage loans from lenders or originators. Investing in whole loans allows the fund to manage the asset directly, potentially offering higher returns but also requiring more active management to hedge credit risk from the borrowers.

Government-issued mortgage bonds: These securities are not as prevalent in Australia as other countries such as the U.S. These are bonds issued by government agencies or government-sponsored enterprises like the U.S. Federal National Mortgage Association and the Federal Home Loan Mortgage Corporation. These bonds are generally considered safer than private market securities because they often carry some level of government guarantee against default risks.

Generally, mortgage-backed securities have lower correlation vs other assets such as equities and commodities, enhancing diversification and therefore can reduce overall portfolio volatility. Mortgage funds can further enable investors to receive a consistent income stream through the interest payments from the underlying securities. Being linked to the real estate, mortgage funds can also offer a hedge against inflation as property values and rents tend to rise with inflation.

Deeper dive

There are also inherent risks associated with mortgage funds, with some being:

Interest rate risk: As rates rise, the value of mortgage bonds typically decreases which could lead to capital losses. Economic downturns can affect the performance of mortgage funds, especially those holding commercial or higher-risk residential mortgages.

Liquidity risk: Another issue, as some mortgage bonds may be challenging to sell quickly without a loss.

Prepayment risk: This exists when borrowers refinance their loans at lower rates, potentially reducing the expected yields from these funds.

Regulatory risk: This presents when changes in regulations affecting mortgage lending, borrowing, or housing finance can impact the value and performance of mortgage funds.

Geographic concentration risk: If a mortgage fund is heavily concentrated in a specific geographic area, it may be more susceptible to economic downturns or changes in local or regional real estate markets.

Regulatory risk: Changes in regulations affecting mortgage lending, borrowing, or housing finance can impact the value and performance of mortgage funds.

Effectively managing a portfolio of mortgage-backed securities and loans requires a deep understanding regarding the intricacies of these securities, such as their sensitivity to changes in interest rates and certain economic conditions. With the right active management approach, mortgage funds can be a valuable addition to a diversified investment portfolio providing opportunities for both income and capital growth.

From the Atchison APL there were a total 25 mortgage fund managers assessed, whereby the average 1 year return as at 31 March 2024 was 4.7 per cent, while the 3-year average return was noted at 2.9 per cent.

MA Secured Real Estate Income was the top performer over the one year period (+9.8 per cent) while Gryphon Capital Income Trust was top of the pack over the three year returning (+6.8 per cent).

The Trilogy Monthly Income Trust

The trust is a pooled mortgage investment vehicle that offers investors the opportunity to tap into the returns generated from loans secured by registered first mortgages of Australian property. This trust has financed a wide variety property development across residential, commercial, industrial and retail sectors in Australia. For over 15 years the trust has managed and raised funds from investors which have successfully supported the completion of hundreds of projects nationwide.

The investment strategy of the trust focuses on sourcing loans that are secured by registered first mortgages, with these properties being geographically diversified across various states and territories in Australia. Additionally, the trust may hold other assets to enhance portfolio diversification and potential returns. This approach ensures a broad exposure to different market dynamics and property sectors, aligning with the trust’s objectives of robust returns and capital appreciation. As at 31 March, trust has a significant holding in short term loans, with the highest state exposure being NSW at 41 per cent.

Gryphon Capital Income Trust

The trust aims to generate consistent and sustainable monthly income, with a strong focus on capital preservation. By tapping into an asset class that was previously inaccessible to retail investors, GCI strives to achieve the highest risk adjusted returns. Its goal is to provide target income distributions at the RBA cash rate plus 3.5 per cent, per annum. GCI primarily invests in structured credit markets, with a particular emphasis on RMBS, which are considered a defensive and loss-remote asset class. This strategic approach allows GCI to offer attractive returns while prioritising the safety of investors’ capital.

MA Secured Real Estate Income

MA Secured Real Estate Income focuses on generating consistent, sustainable returns by investing in high-quality real estate assets. The fund’s primary strategy revolves around capital preservation while striving to produce dependable monthly income. Targeting a class of assets previously inaccessible to retail investors, MA Secured Real Estate Income aims to achieve superior risk-adjusted returns, promising its investors an income distribution exceeding the RBA cash rate by 3.5 per cent, per annum.

The fund principally invests in structured credit markets, with a significant emphasis on RMBS. This selective approach allows the fund to offer an attractive balance of risk and reward, ensuring stable income while prioritising the security of capital. Most recently the fund hold 43 per cent of short term loans with the maturity of less than 3 months, with the greatest exposure of state being NSW at 52 per cent.