Thursday 9th June 2022

Markets still 'vulnerable' to weaker earnings

Head of Australian Equities at T. Rowe Price, Randal Jenneke, has released a note to clients that conveys a somewhat cautious tone towards the Australian equity market.

Head of Australian Equities at T. Rowe Price, Randal Jenneke, has released a note to clients that conveys a somewhat cautious tone towards the Australian equity market. His concern stems from a lack of recognition in the local equity market of the aggressive monetary tightening cycle expected to play-out.

With interest rates on the rise, the cost of waiting for future growth to materialise isn’t so small anymore. And so, it means the days of high-P/E growth stocks are long gone. In its place is value built on earnings and fundamentals.

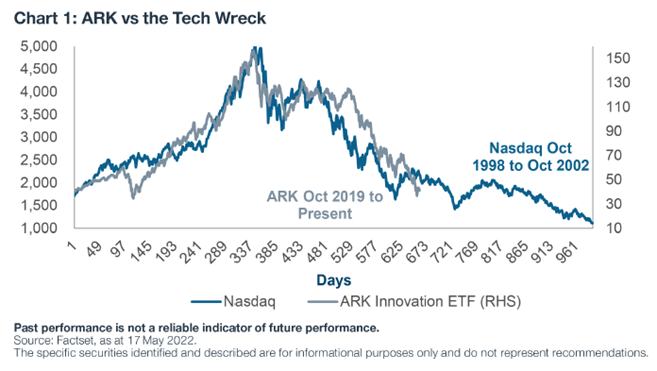

Jenneke says earnings will become the market’s main focus as economic momentum slows. “In this unforgiving climate it is yesterday’s high-flying heroes that have become today’s villains – just try mentioning ‘profitless tech’ at a dinner table. Take ARK, the poster child of the category, as an example. Its precipitous fall from grace closely mirrors the Tech Wreck of the 2000s (Chart 1),” says Jenneke.

Much of the volatility and selling has been driven by valuation de-ratings, especially in the tech sector. When the markets capitulate, assets priced on extreme valuations are the first to be offloaded as the risk-on sell-off begins to correct expensive premiums on assets. This usually occurs towards the latter stage. In earlier stages, the cost of waiting is minimal with falling interest rates, and so the idea of achieving sales growth in the future along with a good story is all that is needed to send valuations higher.

This is where Jenneke becomes a little worried.

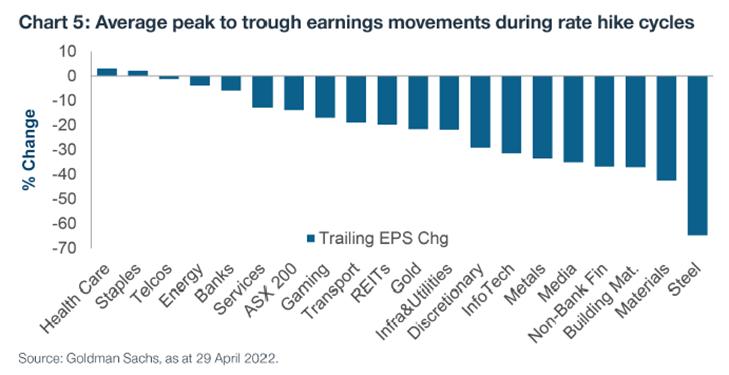

“Earnings expectations have held up well globally, however, we believe they are not pricing the full extent of the cyclical risk ahead. Despite a notable de-rating year-to-date, markets remain vulnerable to weaker earnings. Higher costs and weaker demand are not a good cocktail for valuations in the near term,” says Jenneke.

And this doesn’t even take into account the aggressive interest rate environment that lays ahead.

But things aren’t all that bad. Jenneke is confident Australia can weather this storm better than its overseas counterparts. And on the positive side, the recent share market sell-off has uncovered some great buying opportunities in stocks that are attractively valued.

Jenneke concludes by saying, “We believe quality names (those higher profitability companies with lower earnings volatility and strong balance sheets) will also likely perform well amid rising cost pressures and weaker margins. We don’t believe there will be a clear winner in the growth vs value battle in this environment. The periods of decade long rotations are likely behind us. As are the days where overoptimistic stories alone could drive extreme valuation re-ratings – earnings and fundamentals will be the focus in the bear market arena.”

Ishan is an experienced journalist covering The Insider Adviser publication.