Monday 4th September 2023

Consumer discretionary strength drives upbeat reporting season

Companies were largely able to pass cost increases on to the surprisingly resilient Australian consumer, allowing them to defend profit margins, while retail continued to defy analysts' expectations of a downturn.

Company profit results were robust during reporting season, with beats – profits coming in above forecasts – outnumbering misses by a ratio of 5-to-3, as surprisingly resilient consumers underpin a strong Australian economy.

The beat rate was strongest for the materials (ex-mining) and communication services sectors, while earnings misses were greatest for consumer staples and information technology, new research from UBS reveals.

Rising costs were the biggest headache for companies this reporting season, largely stemming from higher labour expenses, as well as rising rent, energy, transport and technology expenses.

“The broad-based stickiness in cost inflation that we saw in company results [and] recent business survey data suggests that input costs pressures will likely remain elevated,” UBS equity analysts Richard Schellbach (pictured, centre) and Sparsh Polepalle (pictured, left) say in a recent earnings season analysis.

But the good news for shareholders is that companies largely passed cost increases on to customers in 2022-23, which has allowed them to defend their profit margins. “As was the case in the February results period, telcos and insurers were again able to push through price increases to their customers without damaging sales,” they say.

“The fact that most Australian companies have had little trouble passing on high input costs over the past year has actually not surprised us, and reflects an end customer that has been able (although reluctantly) to digest higher prices. Results through August show this dynamic is mostly continuing.”

Retail spending remains resilient

One of the most surprising outcomes from the August reporting season is the strong performance of consumer discretionary retailers, with the expected hit from higher interest rates and inflation not proving as bad as many analysts had feared.

“In the months leading [into the August] results, investors had piled into consumer staple companies such as supermarkets on expectations that the discretionary names would suffer as householders struggled against cost-of-living pressures and higher interest rates,” Schellbach and Polepalle say. “Instead, discretionary retailers saw that consumer spending was slowing (but not collapsing), whilst staples suffered under cost and operational challenges.”

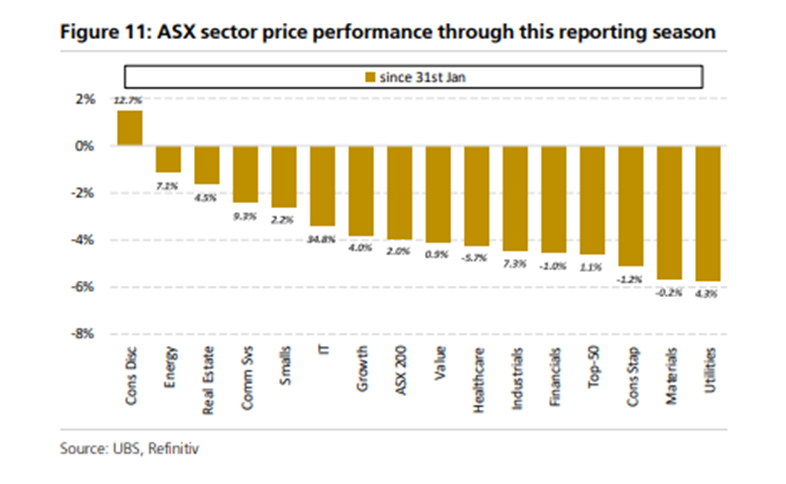

Since January 31, consumer discretionary stocks have been the best price performers (see chart).

The resilience of the retail sector is backed by August data from the Australian Bureau of Statistics. Retail sales rose by more than expected in July, up 0.5 per cent from June compared with economists’ forecasts of 0.3 per cent, with sales rising 2.1 per cent from July 2022. Department stores and clothing and footwear sales were the best performers, rebounding after relatively weak end-of-financial-year sales.

“The retail sales performance, together with recent trading updates from listed retailers, appear to be consistent with a ‘soft landing’ scenario,” says Alexander Mees (pictured, right), co-head of research at Morgans. “Low unemployment is sustaining an apparently controlled descent in retail sales in the face of relentless cost of living pressures.

“This is a positive scenario for all retailers, but especially good (relative to prior expectations) for those that operate in the more discretionary categories of clothing, footwear, electronics and homewares,” he adds.

“With only a few exceptions, most retailers have reported sales trends that are also less precipitous than may have been feared. For investors wishing to build their exposure to discretionary retail, we prefer Lovisa Holdings [ASX:LOV], Super Retail Group [ASX:SUL] and Universal Store Holdings [ASX:UNI].” Mees says Morgans has also upgraded Accent Group (ASX:AX1) and Baby Bunting Group (ASX:BBN) to ‘add’ ratings.

That said, some retail companies are doing it tougher. UBS noted that Adairs (ASX:ADH), Dominos Pizza Enterprises (ASX:DMP), JB Hi-Fi (ASX:JBH), Vicinity Centres (ASX:VCX) and Woolworths Group (ASX:WOW) were among companies whose management noted a consumer or economic slowdown.

Outside the retail sector, Morgans has an ‘add’ recommendation on Mineral Resources (ASX:MIN), which delivered a mixed profit performance but impressed the broker and shareholders with strong cash flow and a big increase in its full-year dividend. The lithium exporter delivered a fully franked dividend of 70 cents per share, yielding an overall FY23 dividend of $1.90 per share, a 90 per cent increase on FY22.

Nicki is an experienced journalist writing across three publications.