Thursday 7th March 2024

Beyond bricks and mortar: 2024's best listed property fund managers unveiled

For many Australians, REITS have been a cornerstone for those looking to dip their toes into the property market without the traditional barriers of direct ownership. So, who were some top performing managers as at January 2024?

Listed property investments via Real Estate Investment Trusts, or ‘REITs’, offers a practical way for investors to trade real estate on stock exchanges like the ASX. These instruments allow for swift portfolio adjustments due to their high liquidity, with the added perks of consistent yields from property rentals, plus the potential for capital growth.

Investors can therefore enjoy a diversified and accessible entry into real estate across various geographies and sectors, often at lower costs compared to direct property ownership.

Like any asset class listed property also comes downsides, below are a few that investors may need to be aware of:

- Equity or market risks : REITS tend to move in step with the equity markets, meaning that broader stock and market sentiment volatility can also affect them.

- Concentration risks of A-REITS vs G-REITS: Australian REITS shows a high degree of concentration compared to its global counterpart. The S&P/ASX200 A-REIT (Sector) Index consists of just 18 companies, whereas Global REITS represented by FTSE EPRA NAREIT Developed Index consists of 367 companies.

- Interest rate risks: Listed properties are actively traded on stock exchanges, with investors’ valuations reflecting not only current asset worth but also projections about future economic conditions. Consequently, investor expectations regarding variables like interest rates or regulatory shifts are swiftly factored into REIT trading prices.

REITs are therefore a double-edged sword, offering accessible real estate diversification while carrying inherent market-related risks.

As at 31 January 2024, the average listed property fund manager, represented by FE AMI Listed Property (aggregated peer group) data returned 7.6 per cent over one year and 6.7 per cent over the three years.

From the Atchison APL there were a total 81 fund managers assessed, with the average one year return coming in at 8.75 per cent and average three year return at 5.75 per cent.

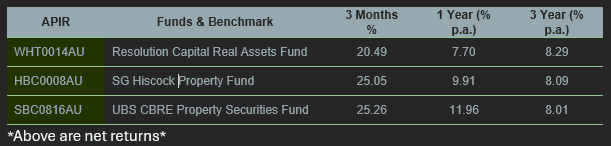

Below are the top three performing REIT managers based on the Atchison APL over the one year and three years (net returns).

UBS CBRE Property Securities Fund was top performer over the one year (+25.26 per cent), while Resolution Capital Real Assets Fund was the best over the three-year period (+8.29 per cent).

Resolution Capital Real Assets Fund

This fund provides investors with the opportunity to have a stake in a professionally managed portfolio comprising primarily of A-REITs, along with Australian listed infrastructure. The portfolio’s investments span across a variety of commercial real estate assets including office buildings, retail shopping centres, and logistics warehouses, in addition to infrastructure assets like airports, pipelines, toll roads and utilities.

Resolution Capital aims to boost returns by allocating up to 20 per cent of the fund’s assets into international real estate and infrastructure securities traded on global stock markets. The fund operates in Australian dollars and may engage in hedging to manage the risk associated with foreign currency fluctuations. During January, a top contributor was Goodman Group (GMG.ASX) a well-known name which operates as a worldwide integrated property group with a footprint in Australia, New Zealand, Asia, Europe, the United Kingdom, North America, and Brazil. It consists of stapled entities including Goodman Limited, Goodman Industrial Trust, and Goodman Logistics (HK) Limited.

SG Hiscock Property Fund

SG Hiscock employs a disciplined investment strategy, blending quantitative valuations with fundamental analysis and market sentiment analysis. This approach results in portfolios with value characteristics, moderated by fundamental insights.

Key beliefs include the convergence of prices to fair value, the importance of a property-centric valuation perspective, low turnover mirroring direct property investment, bottom-up analysis for capturing inefficiencies, and the critical role of in-depth research.

The fund invests mainly in ASX-listed securities, including REITs and property-related companies. Portfolio composition ranges from 15 to 60 stocks, adhering to guidelines that limit exposure to any single entity. Maximum allocations are 20 per cent to cash and 5 per cent to infrastructure assets. A top performing asset for the fund as at January was Charter Hall Social Infrastructure REIT (ASX:CQE), which specialises in investment in social infrastructure properties across Australia and New Zealand.

UBS CBRE Property Securities Fund

This fund actively manages a portfolio of 15-25 mainly Australian property and related equities, diversifying across locations and sectors. It employs a multi-step strategy, blending top-down sector analysis with bottom-up stock selection.

Sector allocation assesses property market trends, while stock picks are based on in-depth fundamental analysis, evaluating securities both independently and comparatively.

In terms of recent performance, a key driver was the fund’s overweight position to Scentre Group (SCG.ASX), an A-REIT manager that owns and operates Westfield in Australia and New Zealand, holding interests in 42 Westfield centres that house over 12,000 retail outlets.