Tuesday 14th June 2022

ASX falls in worst week since 2020, Atlas bid, Douglass returns

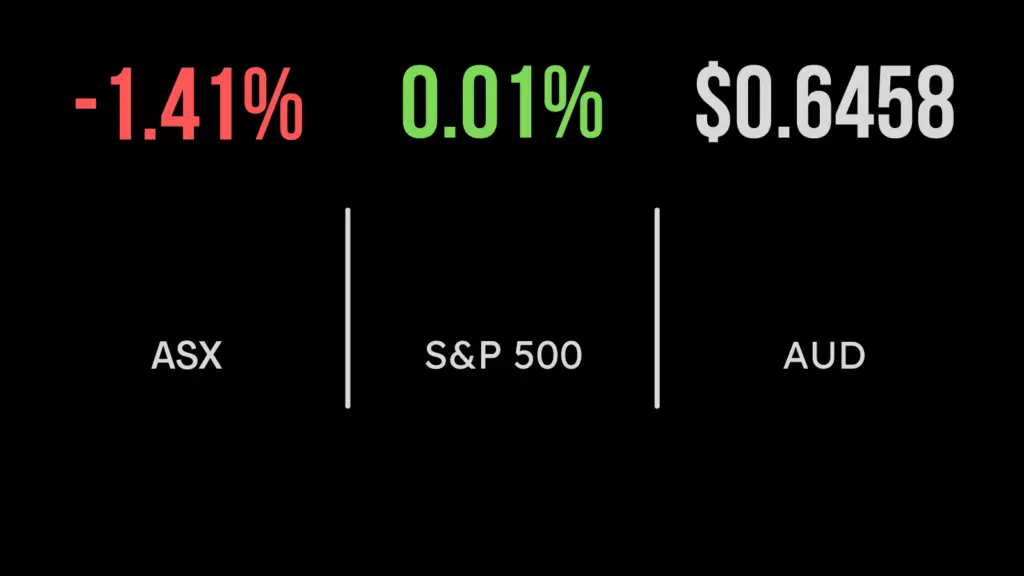

The local market was pushed lower by the global turnaround in interest rates with the S&P/ASX200 falling 1.3 per cent to finish the week.

Every sector was lower, led by property, which fell 2.9 per cent on concerns that higher interest rates will hit valuations, while another six sectors dropped more than 1 per cent, including financials and consumer groups.

Among the biggest detractors were rare earths group Lynas (ASX: LYC), down 5.7 per cent, Boral (ASX: BLD) and JB HiFi (ASX: JBH) which fell more than 4 per cent each.

The weak end on Friday resulted in the market seeing a 4.2 per cent loss for the week, the worst since 2020 after the Reserve Bank decided to hike interest rates by a more than expected 50 basis points to combat inflation.

Among the sectors worst hit was financials, despite many expecting banks to benefit from higher interest rates in the form of wider profit margins.

The sector fell more than 9 per cent with the Commonwealth Bank (ASX: CBA), Westpac (ASX: WBC) and National Australia Bank (ASX: NAB) all entering a correction, falling 10 per cent from their highs.

Atlas Arteria was a rare highlight gaining 13 per cent across the week after IFM Investors announced they had purchased around 15 per cent of the shares on issue and were considering a takeover.

US markets hit by ‘unexpected’ inflation print, Docu Sign shares tank, sentiment weakens

It was another rough week for the US and global markets after an ‘unexpected’ inflation print, the highest since 1981, disrupted what had been a strengthening recovery in recent weeks.

The inflation result for May was 8.6 per cent for the prior 12 months, with the core reading a more reasonable 6 per cent, but higher than forecast.

Once again experts were unable to predict even the most short-term economic events. The price of oil, energy and petrol remains the biggest contributor with no signs of slowing until the war in Ukraine is resolved.

Consumer sentiment has been hard hit by surging inflation expectations, with the print falling from 58 to 50 points in a week.

Technology companies remain under the most selling pressure, with Netflix and eBay falling another 5 per cent each, while DocuSign (NYSE: DOCU) tanked by 24 per cent after failing to meet sales and profit forecasts.

Drew is editor of The Inside Network's publications and a principal adviser at Wattle Partners.