Wednesday 5th June 2024

Wealth transfer on hold: Boomers reluctant to down-size, content to wait

The data is a reminder that while this enormous shift of wealth is imminent, it won't happen before its time. According to AMP, more education about the options available might instigate the process.

The $3.5 trillion intergenerational transfer of wealth from the baby boomer generation to their millennial and Generation Z descendants will not happen before its time, with the vast majority preferring to transfer their wealth upon death rather than dole out an early inheritance according to new data from AMP.

Despite 80 per cent of over 65s believing their children face “similar or harder” financial challenges than they did growing up, and wanting to help their children, 70 cent of over 65s said they were unwilling to compromise their retirement lifestyle to provide financial assistance.

AMP also notes that 80 per cent of over 65s were not prepared to downsize their primary residence in order to release funds that may end up with their children. Worth noting, however, is that by downsizing, retirees would also convert home equity that isn’t counted as an asset for pension purposes by Centrelink, into equity that would be counted as an asset.

The data is an acute reminder that while retirees are preparing for the great intergenerational wealth transfer, and the receiving end of that transfer is largely in need of financial assistance due to cost of living pressures and soaring housing costs, the transfer will take place on their terms.

According to the Productivity Commission, 90 per cent of all intergenerational wealth transferred take place through death, when the descendants are well over 50 years of age.

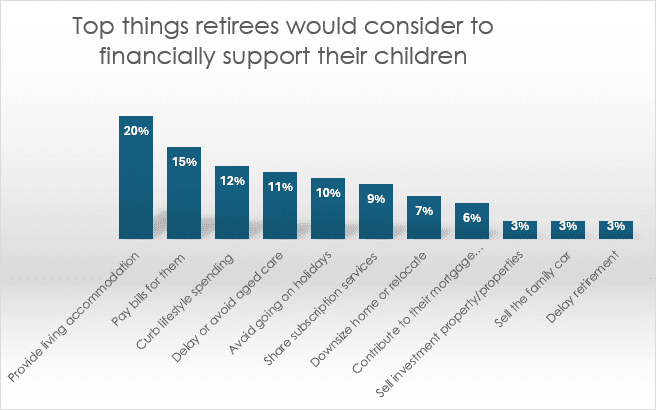

A common compromise, AMP reports, is for retirees to support their children by providing a place to live in the family home, which has given rise to the ‘never leave home’ generation term. The Melbourne Institute has conducted research showing that half of Australians aged 18 to 29 are still living at home.

Otherwise, retirees are looking to help their descendants by paying their bills, which could mean contributing to their mortgage.

Confidence and education

According to AMP’s director of retirement Ben Hiller, the key to finding ways for retirees to help their descendants while protecting their lifestyle is to give them confidence to do so while by creating pathways to unlock equity without selling the family home.

“Unlocking different options for financial support, beyond accommodation, starts with older Australians having greater comfort with their own finances. We know, for example, far too many retirees are unnecessarily fearful their savings won’t last their lifetime,” Hiller said.

“Providing retirees with the financial confidence that their savings will last, will not only help them live life to the fullest, but also give greater clarity with how they can help their kids.”

More education should be provided about the alternatives to downsizing, he suggested, including annuities and reverse mortgages.

“This confidence can be built in a number of ways, including increasing financial literacy and knowledge through education resources and financial advice, and through the use of solutions that provide greater assurance on lifetime income,” Hiller said.

“Given retirees’ attachment to the family home, it’s also clear that as an industry, we need to explore new ways to help retirees unlock capital from their home, without the need to downsize or compromise their long-term wellbeing”.

Tahn is former managing editor across The Inside Network's three publications.