Monday 27th June 2022

Understanding development funds

With inflation embedding itself back into the economy, the days of easy money have quickly become a thing of the past.

With inflation embedding itself back into the economy, the days of easy money have quickly become a thing of the past. Not only do central banks now need to take action on inflation, but investors must also change the way they invest to account for higher interest rates. And so, the rotation away from risk and into quality defensives and alternatives is well and truly underway if the volatility in the share market is anything to go by.

Investments that have a lower correlation to the share market and bond market are primarily what an investor will be seeking to help diversify during times of high inflation. For this article, we will be exploring development funds, how they work and what role they can play within diversified portfolios.

The retreat of the major banks from the development and property sector has opened a significant opportunity for direct lenders and non-bank lenders, but experience, skill and due diligence remain the top priority in negotiating the sector.

At its most simple, a development fund is simply a private trust that allows investors to buy equity or lend capital into major property development projects or portfolios. It pools together investor funds which are used to fund this large-scale property development through debt financing arrangements.

For the borrower, the development financing arrangements are unlike a regular home loan. Loan amounts are released in stages so that the borrower can pay the builder and others involved in the construction process. This helps the borrower maintain accountability by updating investors on the progress of construction so that they know funds are being applied correctly. The five major stages of construction generally considered for a property development loan are – The deposit, Base stage, Frame stage, Lock-up stage and Fixing stage.

By investing in this type of strategy, an investor will receive a return in the form of distributions from the fund predominantly coming from interest and capital repayments. As the properties settle or generate income, this is passed back to the investors of the pooled fund when the capital is repaid. Every loan is subject to specific terms and clauses, is traditionally shorter-term (typically, less than a few years) with interest payable regardless of the length it remains open.

The process overall is relatively straightforward. Let’s look at the Alceon Debt Income Fund, for example. The lender, in this case, Alceon, provides capital to finance the purchase of land, or for the development or redevelopment of residential or commercial property. In return, interest on the loan is paid to the Fund either monthly, quarterly, or capitalised and paid at the end of the loan term. Alceon collects the interest paid from borrowers and distributes the net income as distributions to investors on a monthly basis.

When assessing the fundamentals of a development fund, it’s important to look at the Loan to Value ratio (LVR), not unlike a bank would. Let’s say the LVR is 80 per cent. The loan amount is calculated as 80 per cent of the property’s value. This means the borrower can borrow up to 80 per cent of the property value and is required to stump up 20 per cent of the property’s value as a deposit. The LVR plays a crucial role in determining the risk and return potential. The higher the LVR, the higher the risk. As a rule of thumb, an LVR below 70 per cent is considered low.

With the current shortage in property funding, capital solutions firms such as Alceon Group have helped fill the gap by lending to mid-sized and large property developers, after the big banks reduced their lending and decided to focus on traditional home loans.

The alternative investment manager launched its Debt Income Fund back in 2017, with a yield target of between 5% to 7% per annum, to meet the growing demand by institutional investors and family offices wanting secured private debt. The majority of Alceon’s lending to developers has been senior debt typically in the range of $10 million to $50 million, secured over high-quality assets in different stages both pre and post-development. But what exactly does this mean?

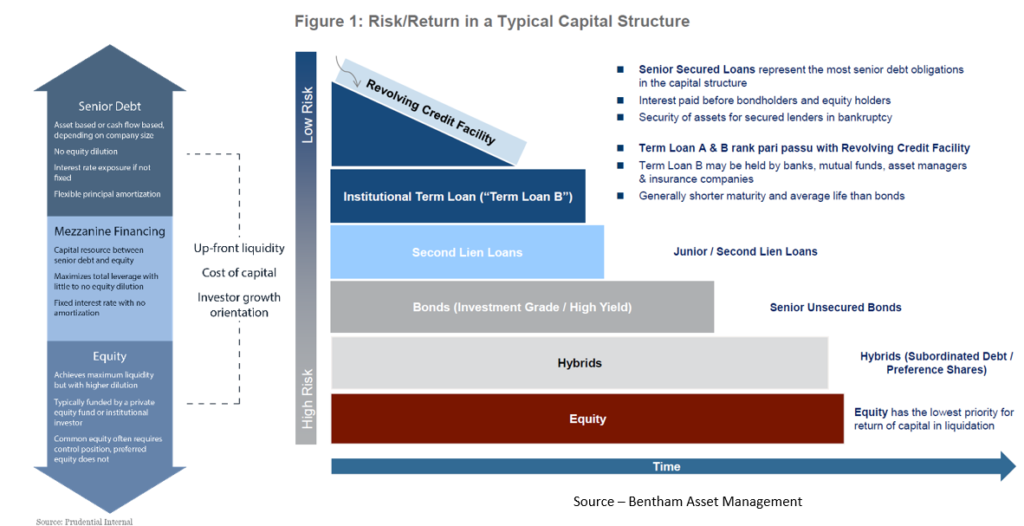

A development loan can come in the form of various debt/equity instruments which form the “capital structure” of a company. Looking at the capital structure diagram above, the various debt/equity instruments are ranked in order of priority of payment, or seniority.

Security refers to a creditor’s right to take a mortgage over a property, in case of a default. A senior secured loan will have the first ranking claim over both the cash flow and assets of a borrower. It carries the lowest risk. Senior unsecured debt means it is senior in payment but without any specific security backing the asset. Subordinated debt or Mezzanine debt is an unsecured borrowing and ranks after senior debt.

Key qualities that ensure the development debt fund is a good investment:

- Low risk – One option to manage risk is to understand and control the exposures being taken and the security provided. Alceon focuses on providing senior secured loans; second-ranking loans are used where the LVR does not exceed 65 per cent. Its allocation to second-ranking loans is capped at 20 per cent. ensuring greater protection should a developer experience any trouble.

- Security – The majority of loans are secured by registered first-ranking mortgages held over Australian property, mostly on the east coast of Australia. The loans finance a mix of real estate development, construction and ownership across multiple sectors and property usage types

- Interest rate – Alceon’s fund aims to provide investors with a total annualised return of 5-7 per cent through monthly income dividends from a diversified pool of loans. The reason this is higher is due to the experience and relative efficiencies afforded to groups like Alceon, which are able to carve-out a niche and know an entire sub-sector of the market inside out.

Ishan is an experienced journalist covering The Insider Adviser publication.