Nick Dignam from Fortitude Investment Partners shares insights with Lachlan Maddock from Fortitude Investment Partners on how a diversified portfolio in mid-market private equity is structured. The Inside Adviser

The world of alternative investments is at a crossroads. As markets defy expectations and liquidity concerns take centre stage, investors find themselves forced to rethink how they deploy capital in an increasingly complex environment.

Three business ‘upgrades’ for advisers in 2021

Despite hope that the vaccines would see a return to normal life in 2021, it appears we will live through at least another 12 months of uncertainty. Few people, outside of the obvious, have felt the emotional and operational brunt of the pandemic more than financial advisers.

Most advisers I speak to were inundated with stressed phone calls during the pandemic from clients and friends alike. The period of March through October, in Melbourne at least, was one of near-exhaustion, both physically and mentally for financial advisers. Self-owned practices were dealing with the most volatile markets in history, while ensuring their staff and families were safe, and businesses able to run in a locked-down environment.

This period reiterated to me that few participants in financial markets, whether journalists, fund managers or industry super funds, are at the coal face of client discussions like financial advisers are. They are the first port of call when markets fall, requiring swift decision-making and in many cases acting as a psychologist to overcome biases we only read about. Very few resources, whether in the form of emotional or business support were on offer, in fact most regulatory requirements continued but with some leniency at times.

It was during the sleepless nights of this period that I’m sure many of us came to the conclusion that there must be an easier way to run our businesses, while continuing to deliver for our clients. I felt it appropriate to offer four insights from my experience during the period, that have simplified my business as we move forward.

The first is to fully embrace the fixed-fee phenomenon. For those studying or having completed the FASEA exam, the concept of asset-based fees has been raised as not accurately reflecting the work involved in managing client portfolios of different sizes. For instance, does it cost $90,000 more to manage a portfolio worth $10 million compared to one worth $1 million? Obviously, there is insurance, implementation and other risks to consider, but the one-size-fits-all approach appears to be coming to an end.

The solution, it seems, is for advisers to truly understand those people they have the most skill and resources to assist, and construct an offering that is suited to them, rather than to the masses. Whether this is tiered levels of service, fees adjusted to the age of each client, number of entities, or even the type of investments they prefer. It’s time to make a decision, be clear and implement it, the results will show in your confidence in client discussions.

The second is to overcome the willingness to maintain the status quo and review any third-party service providers; in particular, platforms. The big-name platforms have come to the table in 2021, announcing huge fee reductions as they seek to slow outflows to the independent challengers, at the same time that their predominantly bank owners were seeking to sell them to the highest bidder.

In many cases, the reasons behind our preferences for individual platforms, whether in the form of fee discounts or accessibility of certain investments, may have been overcome. It is likely with all this competition that the platform market is a “race to zero” not unlike the free trading app Robinhood, so as usual we must ensure our clients are getting the best out of it.

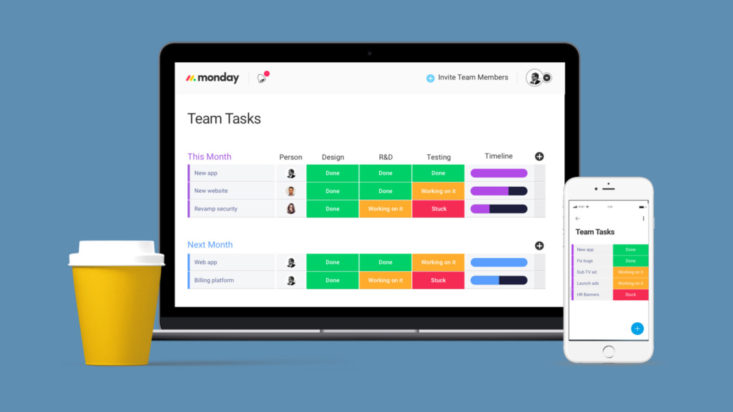

The third insight centres on the importance of transparency. With staff members having become accustomed to working from home, or at least enjoying the flexibility, transparency, record-keeping and workflow management has never been more important. The issue facing financial advisers, however, is that despite the incredible influx of technology options being made available, very few actually work together, or when they do, aren’t of sufficient quality to actually help your business.

One tool worth considering is Monday.com. Despite looking a lot like a traditional Microsoft Excel spreadsheet, the platform is entirely customisable and able to automate an extensive number of tasks that occur in the typical financial advice business. Whether it is onboarding new clients, preparing or implementing advice, the tool can become central to the efficient operation of most businesses.