Nick Dignam from Fortitude Investment Partners shares insights with Lachlan Maddock from Fortitude Investment Partners on how a diversified portfolio in mid-market private equity is structured. The Inside Adviser

The world of alternative investments is at a crossroads. As markets defy expectations and liquidity concerns take centre stage, investors find themselves forced to rethink how they deploy capital in an increasingly complex environment.

Small cap sell-off presents ‘promising backdrop’ for market entry: Australian Ethical

With the recent underperformance of small cap stocks largely attributable to the effects of rapidly inflated interest rates rather than fundamental value change, Australian Ethical portfolio manager Andy Gracie believes could be ripe for investment.

High points in the inflationary cycle, which the economy has been building to in the last 18 months or so, typically hurt the small cap sector more than its large company counterparts as smaller companies are generally perceived to be more vulnerable to tougher economic conditions.

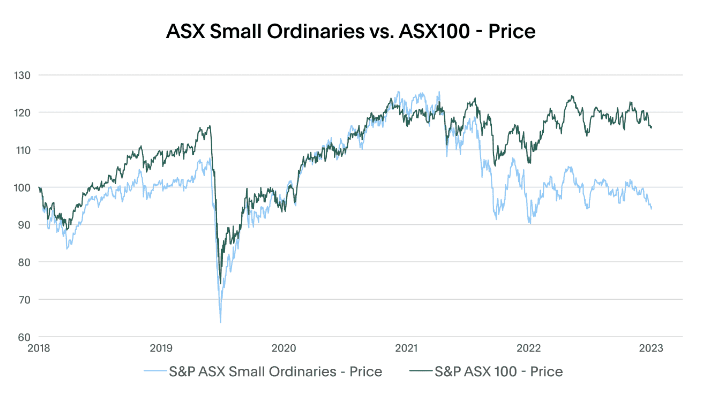

As seen below, the ASX Small Ordinaries has significantly underperformed the ASX100 since 2021.

The intrinsic value of the companies within the small-cap cohort, remains relatively robust. And with the inflationary cycle viewed to be at or near its peak (the Reserve Bank of Australia’s cash rate has increased from zero to 4.35 per cent in 18 months), Gracie thinks this period of underperformance is close to ending.

“Looking forward, the combination of two years underperformance and an interest rate cycle that looks to have nearly peaked is a promising backdrop for investing in small an micro-cap companies,” the portfolio manager described on a recent webcast.

The tide may be turning, however, with the Reserve bank holding rates two out of the last three months and showing a willingness for the economy to catch up with the effect of previous rate increases, which are starting to bite into employment rates and consumer spending.

“We expect confidence to start returning to the micro-cap and the small cap component of the market as interest rates look like they’ve peaked,” he said, noting that this should bring more liquidity back into the market, “whether that be local investors, private equity or strategic buyers”.

In a blog piece accompanying the webcast, Australian Ethic detailed some of the “quality” companies it knows well and has been watching through the sell-off.

“Companies including Aroa Biosurgery, a regenerative soft tissue repair bio tech company, Antisense, a Phase 2 drug developer in muscular dystrophy, and Prophecy, a cyber and call centre provider,” the post stated. “These are names we’ve recently added to our portfolios as we look for to capitalise on the small caps opportunity.

“We’ve been actively talking to 60 or more companies and management teams caught up in the sell off. As interest rates peak in this cycle, we believe the opportunity will continue to improve as investors return to this segment of the market.”

Investment teams will need to be judicious, Gracie believes, but a careful degree of confidence is warranted in a sector that looks undervalued if the expected tailwinds come to pass.

“We think the combination of all that gives a pretty positive backdrop for investing in smaller macros,” he said.