Monday 8th August 2022

Invesco's Tarun Gupta explains how factor investing helps generate consistent alpha

How a star quant analyst used his poker skills to take on calculated risks and deliver outstanding returns

His credentials and pedigree as a practitioner and an academic are well-known among the quant investing community, but perhaps less well-known is quantitative analyst Tarun Gupta’s ability to play a course handicap of zero on any rated golf course as a scratch golfer, or the mathematical competencies that have allowed him to become a keen poker player among his hedge fund colleagues. These are all the hallmarks of a star quant analyst taking on calculated risks to deliver superior returns.

Speaking at an Invesco luncheon, Gupta explained how he took the academic path and focused his skills on creating innovative research on quantitative investment strategies for several well-known Wall Street banks. He now heads up Invesco’s IT for Invesco Quantitative Strategies and is also the managing director of Research.

Quants – better known as the “rocket scientists of Wall Street” – are the brains behind every bank and hedge fund. Quants identify ‘factors’ and construct strategies that best extract them. For that reason, this strategy is also called factor investing and utilises computers to formulate, test and implement these strategies. Mathematical equations aside, the end goal is one of risk management i.e., to deliver superior risk-adjusted performance.

Quants love to let the numbers do the talking, and Gupta has the numbers to back up consistent outperformance. On a five-year rolling basis, the Invesco Australian Core Equity Strategy has outperformed the Mercer Median Manager 91 per cent of the time and outperformed the S&P/ASX 300 Index, 100 per cent of the time.

“The approach we take is a rigorous systematic approach. Perform research and look at long historical back-testing. Test these rigorously and deploy them into live investment management,” Gupta said.

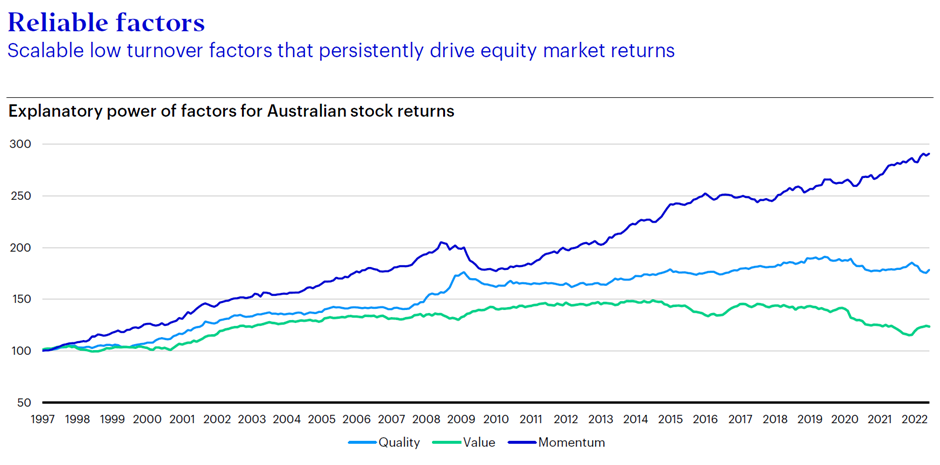

But it’s the investment factors that really distinguish his philosophy. “Broad concepts that have been around for a long time such as valuation is when cheap securities tend to outperform expensive securities,” Gupta said. “Momentum is when securities that tend to go up, go up and quality companies outperform low-quality companies,” Gupta added.

Gupta’s goal is to come up with new ways of measuring these concepts, called signal research, while implementing them into portfolios effectively without taking on uncompensated risks. So, in other words, quants leave nothing to the macro. They don’t take big bets on currencies, inflation, supply-chain disruptions or geopolitical outcomes. These are all macro bets, where human judgement has been in the driving seat. Quants, by contrast, come up with ideas they test rigorously so that they can implement them into portfolios.

“In Australia, momentum tends to be the biggest driver of returns. Along with quality and value. We aren’t trying to predict when one of these is going to underperform or outperform. We put all of these together in an unemotional way, to deliver a good risk-adjusted outcome based on combining them and the power of diversification.”

Gupta explained why he wouldn’t construct a momentum portfolio. He said, “It’s susceptible to drawdowns. Momentum rolls-over and when it does, it tends to be sharp.” As Andre Roberts, senior portfolio manager at Invesco, puts it, “even though momentum might be a good standalone idea, in a risk-adjusted context instead of buying pure momentum, we try to find quality companies that have good earnings growth so you get a more complemented sustainable earnings idea.”

Value has had a tough time. As a single strategy it wouldn’t pay, Gupta says, but it complements momentum and quality. They all have their role to play. Looking at the chart above, the value (green line) investor has underperformed. Essentially, the strategy is based on fundamentals just applied in a systematic way.

“It’s really again, the idea that companies that are improving either based on prices or fundamentals will continue to improve or outperform companies that are deteriorating, that’s the idea of momentum,” Gupta said.

Consistent outperformance, that is the 2.4 percentage points of alpha, doesn’t come from taking big bets in any given security, but rather from generating alpha from the 227 (63 per cent win) positive contributors and 131 detractors.

“It’s much like the poker analogy,” Gupta said. “In any given hand you don’t have much of an edge, but if you play the same game over and over again, you generate a pretty good outcome. That’s really what this portfolio is trying to show. Contrasting this with a fundamental process which will take much more concentrated bets with fewer positions, we are seeking to take many small bets and risk control is at the heart of this. The upside to this is that you won’t have any one position blow up your portfolio. It’s going to be very risk-controlled”.

Gupta’s portfolio captures fundamental insights with built-in risk control that can generate consistent and steady alpha. Or as Gupta put it, “our goal is for each of those to score ones and twos rather than hitting it out of the park for a home run.”

Ishan is an experienced journalist covering The Insider Adviser publication.