Wednesday 9th December 2020

Global credit set for cyclical recovery

Global credit will see a cyclical recovery in 2021

This year has certainly been one for the record books, leaving many to speculate what 2021 may bring.

Given the expectations for a vaccine and the tremendous policy responses at work, Brian L. Kloss, Portfolio Manager at Brandywine Global, a global investment manager, believes there is a very likelihood of a cyclical recovery and further spread tightening in corporate credit due to stronger global GDP growth.

He adds: “The new administration in the U.S. could lead to increased corporate tax rates and regulations, which introduces some uncertainty. However, we believe the extensive monetary and fiscal support, including the potential for another U.S. fiscal stimulus package, would outweigh any economic constraints resulting from these potential regulatory headwinds.

“Therefore, we remain constructive on risk assets, expressing that view through corporate credit markets. A major tailwind for corporate credit markets is the continued strong demand from foreign investors, which has allowed credit markets to issue at record amounts and enabled companies to lower the cost of capital and extend their maturity profiles.

“Our focus now is on the economic cycle as basic industries, capital goods, energy, and other cyclical sectors in both developed and emerging markets are still trading at spreads wide to historical levels.

“We favour those industries that have a more cyclical tilt, like autos and mining, which should see marked improvement as the economy rebounds from the lockdowns.

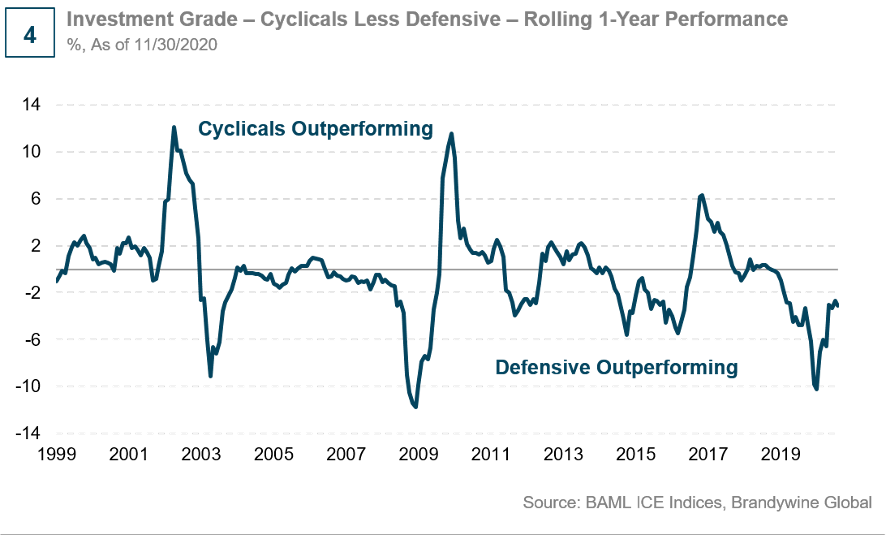

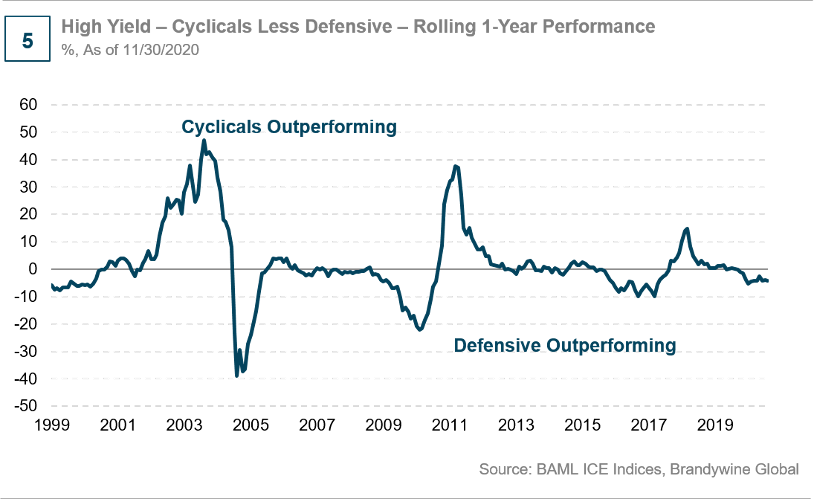

“As the global recovery progresses, demand resumes, manufacturing and exports tick higher, and the medical front draws nearer to resolving the COVID-19 pandemic, conditions are in place for a reflationary trade and substantial spread tightening in these more cyclical areas of the economy (see Charts 4 and 5).

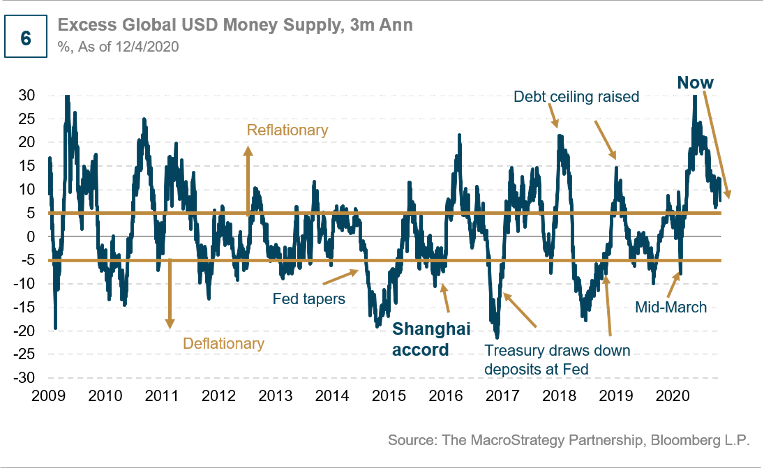

“Our team believes both the BBB and BB quality segments offer the best risk/return profile and should remain supported by monetary policy and the significant excess money supply currently in the system (see Chart 6).

“Also, we favour European high yield, which has more direct involvement from the central bank along with a lower predicted default rate in 2021 versus the U.S. market.

“Our energy exposure is split between foreign state-owned oil companies and recent fallen angels that hold some of the most sought-after assets in the U.S. Within the energy sector, we see the potential for continued supply contraction in the U.S. and a more normalized demand profile in 2021.

“We are generally avoiding both ends of the credit-quality spectrum, with high quality offering limited total return potential, and lower-quality bonds still susceptible to hiccups in the global economic recovery.

“However, if the global economy picks up steam, we would anticipate moving farther down the quality spectrum,” he notes.

“Lastly, while inflation is a risk that we continuously assess, we do not envision a significant back-up in yields in the near term. However, we likely will continue to reduce spread duration in positions that have reached or traded through fair value in favour of opportunities that include some of the following characteristics:

- a shorter maturity

- an OAS that will compensate or cushion an investor for a back-up in the risk-free rate

- cyclical exposure

- commodity exposure

- non-US assets

- lower-quality assets

-ends-

Groupthink is bad, especially at investment management firms. Brandywine Global therefore takes special care to ensure our corporate culture and investment processes support the articulation of diverse viewpoints. This blog is no different. The opinions expressed by our bloggers may sometimes challenge active positioning within one or more of our strategies. Each blogger represents one market view amongst many expressed at Brandywine Global. Although individual opinions will differ, our investment process and macro outlook will remain driven by a team approach.

For all media queries please contact Shed Connect:

Simrita Virk simrita.virk@shedconnect.com