Monday 9th October 2023

All at once, government data finally catches up to adviser shortage

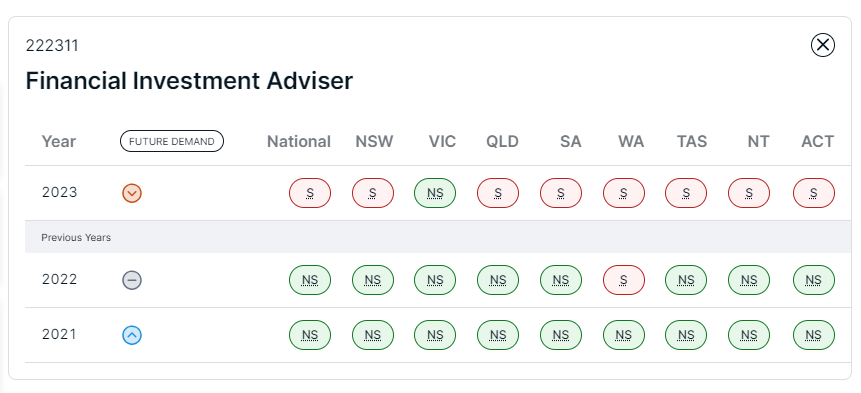

Even when thousands more advisers left the industry in 2022, bringing the cohort down from 28,000 in 2018 to a total of around 17,000, there was still no shortage according to the government's own skills commission.

Somewhat belatedly, the Australian government’s employment commission, Jobs and Skills Australia, has caught up to the fact that the country is woefully short on financial advisers.

In 2023, and for the first time, the role of financial investment adviser was recently marked as being officially in “shortage” across every state (except Victoria).

In 2022, when the Jobs and Skills commission was created, all states were inexplicably classified as “no shortage” (except Western Australia).

The classification upgrade comes well after the issue ignited. Of the 28,000 or so registered advisers in the country in 2018, most of the ones that abandoned the industry (due to regulatory pressure, tougher education standards, a skyrocketing adviser levy and lack of insurance options) did so in the two years following the 2018 Hayne Royal Commission.

By 2021 there were already less than 19,000 advisers left on ASIC’s registry.

In 2022, Wealthdata reports that 2,022 more advisers left the industry (a notable coincidence), with 649 joining for a net loss of 1,373. Yet despite the quantum of advisers falling from 28,000 to around 17,000 by that point (leaving 1 adviser for roughly every 1,117 adult-age Australians), there was still no shortage according to government’s skills commission.

*Source: Jobs and Skills Australia

Even when policymakers were using the adviser shortage as an excuse to propose watering down adviser education standards in late 2021, the government’s own national skills commission says there was no shortage.

For the skills commission to finally acknowledge the shortage in 2023 makes even less sense when you consider that so far this year, only 751 advisers have left while 610 have entered the profession, leaving a net loss of just 106.

Part of the reason those numbers have softened so much in 2023, says Wealthdata managing director Colin Williams, is that some advisers have re-entered the industry in light of the education policy change. So, while the government has had enough time to recognise the issue and pass legislation aimed at ameliorating it, its own department was blind to the underlying data.

Data catching up

According to the Financial Adviser Association of Australia’s head of policy, Phil Anderson, the anomaly is more about the data “catching up to the reality” than a disconnect between the government and it’s skills tracking department.

The FAAA has spent time recently working with the council on its definition of a financial adviser, he notes, which should result in clearer data representations in the future.

“Previously we weren’t confident that there was an adequate focus on financial advice as a specific role category, they have it down as a ‘financial investment adviser’,” he tells The Inside Adviser. “But the FAAA has done a bit of work this year with the Australian Bureau of Statistics on the classification so I believe that and the data are both improving.”

Anderson also makes the point that the commission’s data, and it’s classification system for shortages, is made from the employer side rather than the client side. The majority of advisers that left the industry came from salaried roles as larger wealth institutions, he explains, and those weren’t reporting an adviser shortage because they largely closed up shop.

This dynamic has changed markedly in the last year, Anderson says, as the industry has experienced a surge in demand.

“The shortage metric is more a measurement of vacancies base on employers going into the market place, rather than client demand,” he says. “And the demand for advisers has clearly risen substantially in the last year or so.”

An alternative pipeline

The change is part of a broader recognition of skills shortages across the country, exacerbated by restrictions to immigration during the pandemic, combined with a renewed focus to cover various industry shortfalls with overseas talent.

The Australian Chamber of Commerce and Industry recently called for a doubling of the skilled migration program to 200,000 people per year. In a 2022 paper Overcoming Australia’s labour and skills shortages, the ACCI identified our skilled migration system as “overly complex and expensive”.

“We should be planning now to restore the migration settings to an even stronger position post-crisis, ensuring Australia’s migration system meets the skill needs of Australia’s businesses and is fit-for-purpose for the long term,” it noted.

According to the FAAA’s Anderson, the skills commission’s acknowledgement of the adviser shortfall may be belated, but it should at least pave the way for more work on this skilled migrant pathway.

“One of the potential outcomes is a recognition of the adviser skills shortage so the government can start looking at what more we can do from a process perspective,” he says. “Where would appropriate candidates come from and what qualifications are recognised? What are the transition arrangements? We want to improve the process without lowering the standards.”

Tahn is former managing editor across The Inside Network's three publications.