Nick Dignam from Fortitude Investment Partners shares insights with Lachlan Maddock from Fortitude Investment Partners on how a diversified portfolio in mid-market private equity is structured. The Inside Adviser

The world of alternative investments is at a crossroads. As markets defy expectations and liquidity concerns take centre stage, investors find themselves forced to rethink how they deploy capital in an increasingly complex environment.

A structural evolution or risky business?

Following a decade-long run of low-interest rates and rising asset prices, many companies took the opportunity to load up on cheap debt. But the recent rise in inflation is forcing interest rates higher and changing the status quo.

To prevent spiralling inflation and reduce its harmful effects, the RBA is well into a tightening cycle, lifting the official cash rate by increments of 25-50 basis points over the last three months. This change in policy also brings about a change in bank lending.

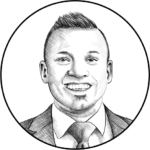

As an unlisted asset class, non-bank lending has been capturing a significant portion of the lending ecosystem, everything from corporate and leveraged loans to specialty lending and asset finance. Even in the mortgage market, non-banks are pushing up the competition by capturing half of the mortgage market, as more and more turn away from the big banks.

Managing Director of MA Financial Group, Frank Danieli, spoke at the Inside Network’s Income and Defensive Assets Symposium where he described the move to non-bank lenders as a ‘monumental’ change.

He points at two factors that have caused this transformation, “brokers now represent 70 percent of new lending origination in Australia, driven by the customer’s desire for choice and regulation. The other major change is open banking and new technology”.

These factors have created the perfect breeding ground for disruptive change. Post the Royal Banking Commission, the best interest duty was introduced to prevent mortgage brokers from being product aligned. It required mortgage brokers to understand the customer’s position, find all the products that suit and present a handful instead of just one. “Banks operate under bank capital regulations and prudential standards. Sometimes these standards diverge from real economics and that creates opportunity. So, you can look at this as a rising tide,” says Danieli.

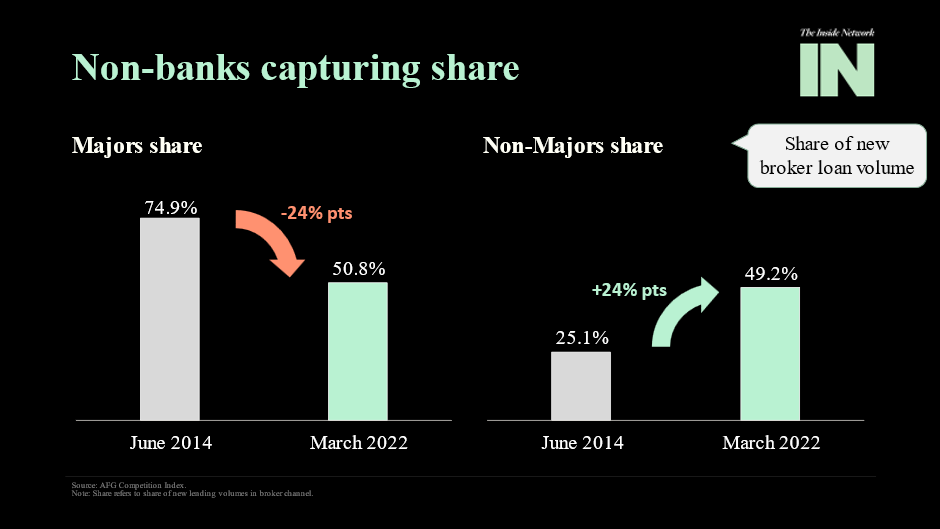

Let’s look at a unique but worthy case study – a regular home loan (80 percent LVR) versus a SMSF loan (60 percent LVR). Typically, SMSF loans are held by high-net-worth individuals with a lot lower LVR. However, the interest rate on SMSF loans carries a higher interest rate. “A SMSF loan gets treated as a non-standard mortgage. The bank is required to hold a lot more capital against it and its return is 2x worse. Banks have gravitated away, and this is what has created an opportunity for non-banks to fill the gap,” says Danieli.

“A rising tide doesn’t lift all ships. Investors must be selective in this space,” warns Danieli. While non-bank lenders are pushing this space to new heights, Danieli warns investors to be careful of fintech offering new and innovative products. Many of these fintech’s appeared just yesterday, in a puff of smoke.

In some cases, fintechs do not have any data and can’t test whether their products work. A study conducted by the Harvard Business school showed that loans originating from fintech had 2x worse delinquency rates than traditional finance companies. Is this mispriced subprime lending?

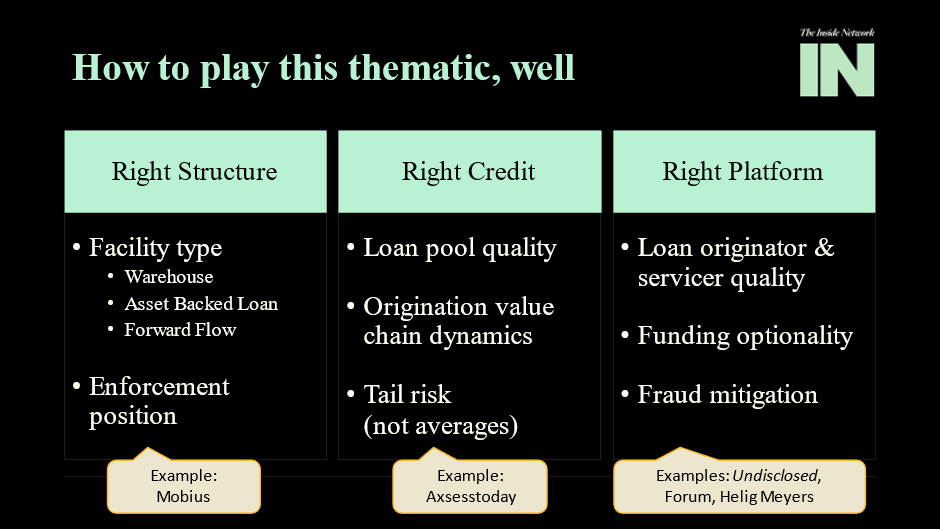

How does an investor play this thematic well?

Danieli highlights the importance of understanding credit risk, and that structure is a critical component in assessing non-bank products. In a downside event, is there a risk that the credit performs but the structure fails and there is a risk of losing money or if things get tough does it have the enforcement rights to get in quickly and stop the credit deterioration and resolve the situation early?

All this aside, Danieli concludes by saying, “The space is extremely attractive because there is a compelling relative value. Compared to traditional fixed income, on a rated basis in Australia, I am seeing premiums of up to 200bps for equivalent credit-rated securities and 300bps-plus in private unrated deals. I think this is a very exciting space, but you need to understand the right structure, right credit and the right platform.”