The alternatives sector is unique in that it’s largely defined by what it’s not. Accordingly, how you fit alternatives within your existing asset class structure will depend on relativity, and how the investments interact with the other asset classes according to Atchison’s Kev Toohey.

The private markets juggernaut is one that has also thrown up a wealth of data that other players can use to sharpen up due diligence when making their own investment decisions – especially in the growing secondaries market.

Investors ‘selling the future to buy the past’: Hyperion

It’s been a torrid start to the year for 2021’s Fund Manager of the Year, Hyperion. The group is clearly feeling the “tech selloff” pinch after both its flagship funds posted negative returns and missed their benchmark expectations in January, also dragging down one-year numbers as a result.

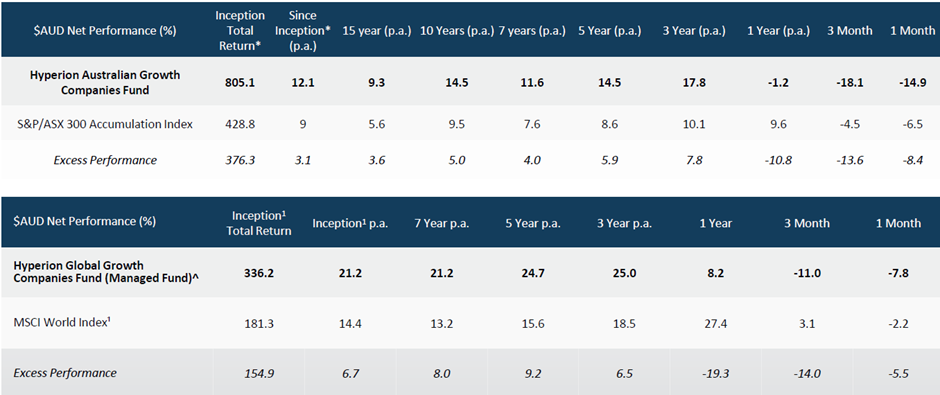

The Hyperion Australian Growth Companies Fund posted a 1.2 per cent loss for the year versus the S&P/ASX 300 Index’s 9.6 per cent gain. That’s a 10.8 per cent miss. The Hyperion Global Growth Companies Fund posted a painful 11 per cent loss versus the MSCI World Index return of 3.1 per cent, a 19.3 per cent underperformance, but as the table and portfolio managers highlight, when investing in growth companies this comes with the territory, and investors must focus on the long-term compounding returns.

With all the uncertainty from Covid-19 and geopolitical tensions currently at play, equity markets have played havoc with Hyperion’s funds. But the team is taking a long-term view and sees its current portfolio as quality picks, reiterating its message that “quality stocks outperform over longer periods.”

Jason Orthman, deputy chief investment officer, says: “This rotation is short-term, and the capital has to flow back. We call it ‘selling the future to buy the past.’ And there has to be a point in time when the funds all flow back.”

Mark Arnold, chief investment officer and managing director, says the war in Ukraine shouldn’t be an issue for markets and the firm’s portfolio. “The war in Ukraine does not change our investment strategy. Higher oil prices detract from future economic growth, which in turn is disinflationary and will help weaken demand. Our portfolio is not sensitive to low economic growth. Effectively Putin is, by invading Ukraine, accelerating the move to sustainable energy and renewable power.”

However, focusing on quality hasn’t paid off for four tech stocks that had very high expectations built into their share price. Great operating results don’t guarantee positive share price moves because expectations can get so high, and results fell below benchmark.

Orthman says, “It’s unusual the fundamentals don’t get focused on. Tesla’s metrics have never been stronger. Its order book is full, and demand is rising. Some of these businesses are cheap. If you annualise its results, it’s trading on a price/earnings (P/E) of 40x. We haven’t seen it trade on these levels in some time.”

PayPal and Meta (the former Facebook) were both negative surprises for Hyperion after results in the 4Q were weaker than expected. Arnold says “The market didn’t take to their results. But there are always a few that don’t surprise and that’s why you have a portfolio approach. PayPal should be able to grow its share price with earnings. There is nothing fundamentally wrong with PayPal. You’ve seen the reset after the result, a really strong network effect. Its digital wallet is all over the world above Google’s. Unfortunately, there might have been high expectations that it was unable to beat.

“Meta is a similar narrative. We need to focus on its long-term vision. They’ve got structural issues with Tik Tok and that is a credible threat. We’re a little more worried about Meta than PayPal and as a consequence, we’ve reduced our position from 5 per cent to 2.5 per cent and that’s the risk about risk adjustments. Overall, both companies had outstanding results.”

Overall, the portfolio is fully invested and the firm’s IRR-based system has been allocating capital to stocks that have fallen the most. Valuations in most companies have been stable. The forecast portfolio IRR is currently almost two standard deviations above the historical average.