Thursday 30th May 2024

The risks and rewards of diversified credit funds

They may be the flavour of the month, and probably for good reason, but are diversified credit funds all that they're cracked up to be? Will Arnost takes a look at the top performing funds on the Atchison APL.

In today’s environment of interest rate and inflation uncertainty, diversified credit funds can serve as a valuable hedge against equity market volatility. Recent rises in global bond yields have pushed credit portfolio yields to near 15-year highs and many expect that these elevated yields are likely to persist, making them appealing to income-focused investors.

The International Monetary Fund predicts that major developed economies will remain resilient despite higher interest rates, with any chances of recessions likely to be brief and shallow. This resilience supports the profitability of companies and thus reassuring credit investors.

Diversified credit funds have been the recent ‘flavour of the month’ for many investors, because they can enhance a multi-asset portfolio by providing diversification, while providing consistent income via yields and higher expected returns compared to traditional fixed-income securities. These funds typically invest across an array of debt instruments, including corporate bonds, sovereign debt, structured products, mortgage-backed securities, asset-backed securities, derivatives and loans.

During times of rising and elevated rates, credit instruments like floating rate notes can be particularly attractive as they adjust their payments in line with interest rate changes, providing an effective hedge against rising rate risks. These periods can also widen credit spreads, offering higher returns for taking those investors willing to take on the additional risk.

Like any other single sector funds, diversified credit funds are associated with various risks including credit risk (issuer default), interest rate risk (value fluctuations due to rate changes), liquidity risk (difficulty in selling certain credit instruments), market risk (impact of overall market conditions on performance) and management risk (reliance on fund managers’ expertise and strategies).

Managing a diversified credit portfolio also involves several distinct challenges. Portfolio managers must navigate overall market volatility to protect capital while ensuring consistent returns. Secondly, conducting thorough credit analysis of underlying debt instruments to evaluate issuers’ creditworthiness is both resource intensive and complex, while balancing liquidity requirements to meet redemption requests adds another layer of complexity for the manager.

Moreover, effective portfolio management of this asset class requires deep understanding and responsiveness to macroeconomic trends such as inflation, geopolitical events and global economic cycles.

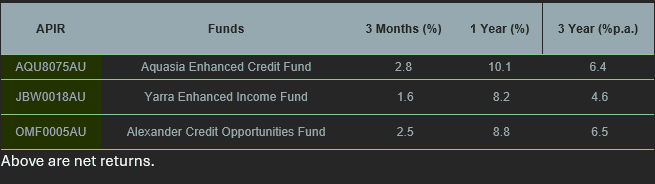

From the Atchison APL there were a total 84 diversified credit funds assessed, whereby the average 1-year return as at 30 April 2024, was 7.0 per cent, while the 3-year average return was noted at 3.8 per cent. Below are the top three performing funds over the one- and three-year periods.

Aquasia Enhanced Credit Fund

The Aquasia Enhanced Credit Fund aims to preserve capital and generate returns exceeding the Bloomberg Aus Bond Bank Bill Index plus 3 per cent over a two to five-year horizon. It invests in a diversified portfolio of credit, fixed-income, cash, and cash-equivalent assets.

At least 40 per cent of the portfolio is allocated to investment grade assets and the fund aims to maintain a mix of liquid and illiquid investments, predominantly in floating rate assets. The fund leverages Aquasia’s extensive network to acquire attractively priced assets, targeting regular income distributions with potential capital gains while actively managing risk and optimising returns. Its specific investments include residential mortgage-backed securities (RMBS), asset-backed securities (ABS), subordinated debt, structured credit, corporate loans and bonds, and hybrid securities. This strategy ensures a robust and diversified asset base aimed at achieving consistent performance.

Most recently the key drivers of performance were the tightening of credit spreads, particularly for structured and securitised assets. This tightening, coupled with the income generated by the underlying investments have resulted in the fund’s outperformance.

Alexander Credit Opportunities Fund

The Alexander Credit Opportunities fund aims to achieve positive returns in both rising and falling markets, targeting a rate of return above the Bloomberg Aus Bond Bank Bill index plus 2 per cent per annum. The fund employs an active management approach, focusing on identifying opportunities in the Australian and global credit markets that offer attractive risk-adjusted returns. It invests in a broad spectrum of fixed income instruments, including corporate bonds, corporate debt, bank bills, commercial paper, loans, hybrid securities, unit trusts, mortgage-backed securities, asset-backed securities, structured credit securities, credit derivatives, and convertible, preference, and ordinary shares.

As at 30 April the fund’s top holdings includes, private asset backed securities (38.4 per cent), public asset backed securities (9.3 per cent), public residential mortgage-backed securities (10 per cent) and cash (10.8) per cent.

Yarra Enhanced Income Fund

The Yarra Enhanced Income Fund aims to achieve higher returns than traditional cash management and fixed income investments over the medium to long term by investing in a diversified portfolio of hybrid (debt/equity) and fixed income securities.

The fund seeks to provide fewer volatile returns compared to equity markets, offering modest capital growth and some franking credits. The investment approach is research-driven, utilising a comprehensive analysis of the broad economic and market environment as well as specific investment details. During April, the primary contributor to performance was the robust income and yield from its underlying assets.