Nick Dignam from Fortitude Investment Partners shares insights with Lachlan Maddock from Fortitude Investment Partners on how a diversified portfolio in mid-market private equity is structured. The Inside Adviser

The world of alternative investments is at a crossroads. As markets defy expectations and liquidity concerns take centre stage, investors find themselves forced to rethink how they deploy capital in an increasingly complex environment.

The perils of yesterday’s logic

Reimagining portfolios for tomorrow’s reality

Increasing inflation volatility represents the greatest challenge to investors for a generation. A new regime and the collapse of the financial market status quo requires us to reimagine portfolios. No longer can we rely on yesterday’s logic.

“Inflation is the endgame. Just brace for inflation volatility first.”

Do we still believe inflation volatility will be the primary feature of the next few years? And, if we do, doesn’t this imply inflation falling sharply at some point in the next year?

The answers are ‘yes’ and ‘yes’.

Why do I have such conviction in inflation volatility and what does this mean for investors?

The reason the answers to these questions matter is that investing for inflation volatility is not the same as investing for inflation. Confusion in this respect will be costly to investors.

Inflation according to central banks

Our policymaking elite take it for granted that inflation is the outcome of an isolated economic mechanism and can be managed by a technocratic, independent central bank which understands the mechanism. Milton Friedman summed up this mechanistic view by saying “inflation is always and everywhere a monetary phenomenon”. Fine for economists, but social and political contexts shape the dynamics of inflation in disparate and confounding ways. Friedman’s statement is about as helpful as saying: “Flooding is always and everywhere a watery phenomenon.”

The lack of humility in the technocratic central bank view of inflation is about to be exposed by a reversal of the dynamics of the past 40 years.

Bona fide inflation

Three observations about the enduring features of inflation stand out.

First, under a paper money standard, pressures between financial markets and the state are resolved through inflation. In short, a lightly anchored paper money system is naturally biased towards inflation.

Second, inflation is associated with a decay in the status order of society. Just consider the tectonic social movements powered by the war on climate change and the Build Back Better agenda. These are powerful challenges to today’s social order and the perfect ecosystem to nurture inflation.

Third, because a capitalist system naturally tends towards inequality inflation is the safety valve against capitalism’s inherent contradictions and weaknesses.

This amounts to the idea that, under a paper money standard, inflation should perhaps be considered a natural feature of capitalism, not just a nasty bug.

Refrigeration mode

The obvious question: if a lightly anchored paper money system is biased to inflation, why has inflation gone missing in action for so long?

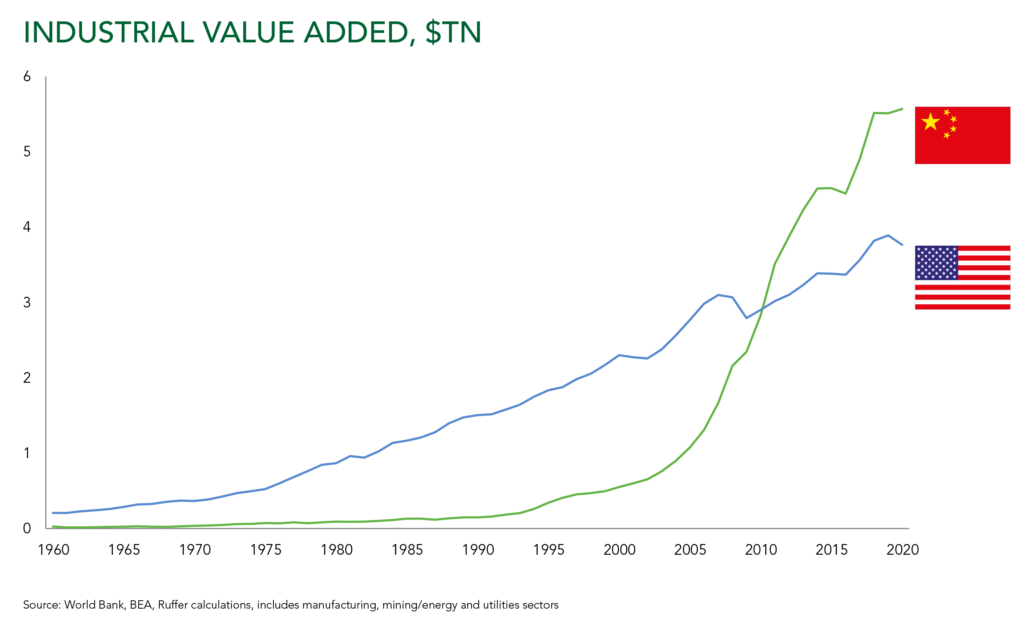

The answer, we have been in ‘refrigeration mode’ for forty years, characterised by the generation of deflationary dynamics arising from the interaction of an inflation focused monetary policy (inflation targeting) with China’s mercantile model.

It has looked a bit like this. Deflationary dynamics deliver positive supply shocks; this lowers inflation, which allows rates to fall. Consumption springs forward as individuals borrow and spend more – enter financial engineering. Inevitably, this leads to excess, which is met with tighter policy. Financial crisis ensues and central banks – fearing deflation – are forced to respond by lowering rates.

Chinese mercantilism is the second part of the equation. The Chinese discovered the magic money tree and with it, they built a manufacturing empire. Rapid industrialisation piled deflationary pressure on durable goods prices, which kept the lid on both consumer price inflation and interest rates in the West.

Monetary policy and China’s mercantile model – fed off each other, and the extraordinary monetary growth which resulted became a powerful, global deflationary mechanism – the refrigeration mode. Both China and the US got what they wanted. China got to leapfrog its industrial development. While the US got low inflation and quiescent monetary conditions – a great moderation.

Heat pump mode

But this had side effects. There is now a huge monetary overhang in China. And the US economy has been hyper-financialised. These extremes are biting back through the political economy. A shift is now underway from refrigeration mode to a new mode – the heat pump.

The system dynamic has become inflationary, and there are new supply side shocks which, crucially, aren’t deflationary. On macro policy, powerful social reactions to the extremes produced by the refrigeration dynamic are feeding into the political economy. Fiscal policy is back in the driving seat, just at the moment central banks have reintroduced an inflationary bias to their reaction functions. When fiscal and monetary policy combine, overall policy becomes more directly inflationary.

What should investors do?

It is tempting to simply invest for the inflationary endgame. After all, turbulence passes eventually. But inflation volatility could be with us for some time. And, when inflation is on a downswing, a portfolio positioned solely for inflation risks losing a wing.

To survive the turbulence of inflation volatility, investors will need a hedged portfolio. Portfolios will need to be intricately constructed – active, for sure, as no static portfolio will survive. And the hedges may be expensive. A portfolio positioned for resilience, rather than optimisation, will sometimes have a weighty cash balance. Cash is an uncomfortable asset to hold in an inflationary world, but it is an essential quiver – storing the portfolio arrows needed to pick off opportunities as they arise.

Hedging when speeding

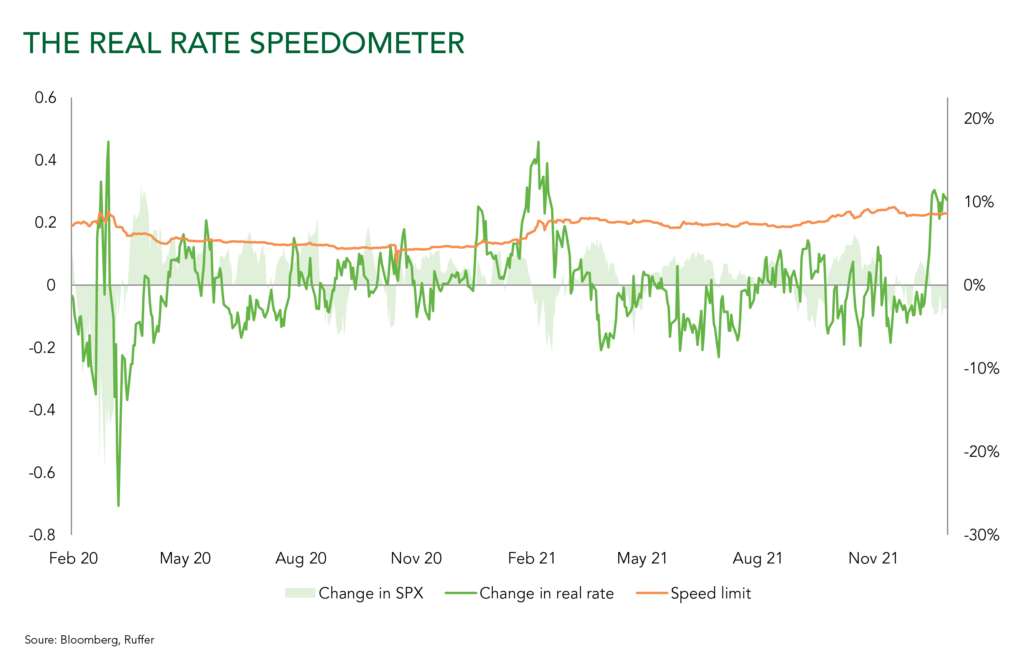

Usually the Fed is the marshal of financial conditions. It tightens monetary policy until some element of the financial system – typically the most leveraged – falls over, causing a tightening of financial conditions. So, as the Fed embarks on a tightening bias, we must look out for speed traps in markets. Real interest rates can serve as a useful speedometer.

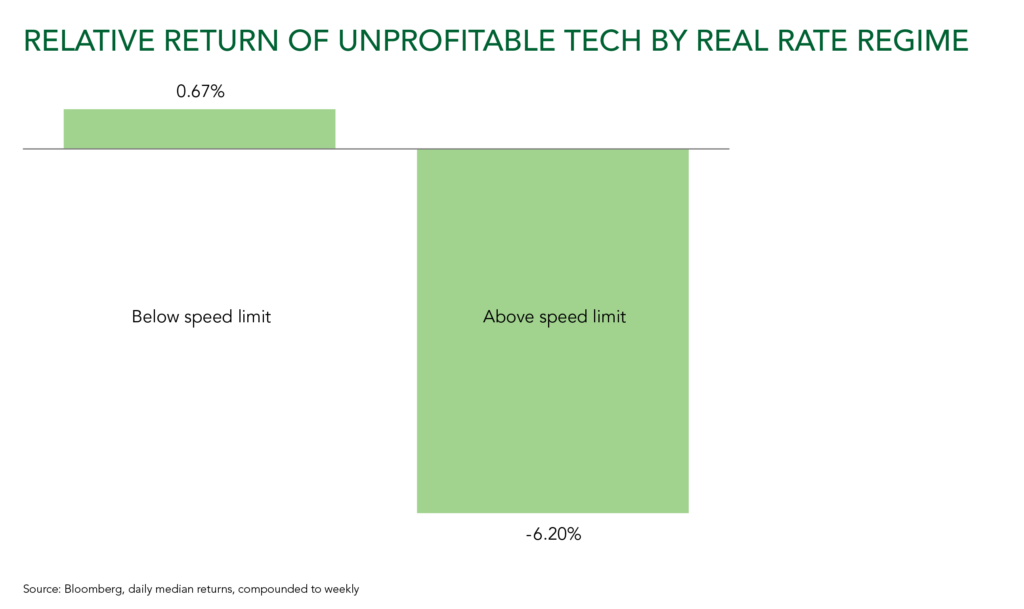

At Ruffer, we compare how fast a medium-term measure of real rates is rising relative to how fast derivatives markets expect them to move – the speed limit. We know that, once real rates speed up, there is a higher probability of equity markets selling off and rotating out of growth stocks and into value stocks. Once real rates exceed the speed limit, the chances of an accident are high.

The sector most exposed to rising real interest rates tends to be the frothy end of the tech market. The Fed is now in tightening mode to combat inflation. Liquidity conditions are going to worsen, and real rates are likely to get jumpy. In equity markets, this will hurt – and already is hurting – unprofitable tech most.

Winter is coming for liquidity, it’s coming for narcissism, it’s coming for crypto, it’s coming for retail punting, and it is definitely coming for businesses which depend on any of these things.

Switch to manual

Beyond the immediate liquidity challenges, investors will have to steer portfolios through the twists and turns of more abrupt economic cycles interacting with liquidity cycles and changing policy reaction functions.

It may take time to play out – financial conditions are still incredibly loose – but we know trip wires lie ahead. And inflation will fall sharply again when financial and economic volatility coincide.

Inflation volatility will eventually give way to inflation, but investing now solely for the inflationary endgame would be a mistake. Peter Drucker, the father of modern management thinking, said: “The greatest danger in times of turbulence is not the turbulence. It is to act with yesterday’s logic.”

Turbulence lies ahead, that’s for sure. The message to investors: portfolios will need to be steered on this journey, requiring new skills, new ways of constructing portfolios and imaginative thinking.

It is time to flick the switch off autopilot.

Written by Ruffer. To learn more visit ruffer.co.uk/en