Nick Dignam from Fortitude Investment Partners shares insights with Lachlan Maddock from Fortitude Investment Partners on how a diversified portfolio in mid-market private equity is structured. The Inside Adviser

The world of alternative investments is at a crossroads. As markets defy expectations and liquidity concerns take centre stage, investors find themselves forced to rethink how they deploy capital in an increasingly complex environment.

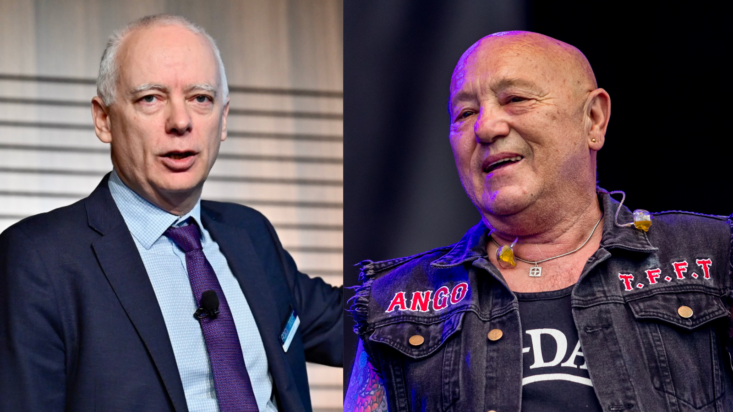

The FAAA’s ‘Angry Anderson’ sounds off on Dixon Advisory drama

For anyone who’s dealt with Phil Anderson, policy chief at the Financial Advice Association of Australia, the nickname ‘Angry Anderson’ would come across as an ironic jest. Cerebral and considered, Anderson is the type who doesn’t often raise his voice.

But these days, Anderson is furious.

It’s taken a frustrating and ultimately harmful regulatory kerfuffle to finally get Anderson’s neck vein bulging. By now, he’s used to working around regulation that doesn’t always make sense. The Dixon Advisory case, however, and the way it has been handled by the government and the corporate regulator, is something else. Not only does the mishandling of it make no sense, but it’s creating some serious collateral damage to advisers – the cohort Anderson is charged with representing.

The FAAA policy chief just spent weeks touring the country and speaking to these advisers about the Dixons case, the Compensation Scheme of Last Resort designed to repatriate consumers, and the role of the government and ASIC in botching the whole thing. Not forgotten, either, was the advice group E&P Financial, which had Dixon under its wing when 4,606 clients lost $360 million.

It was during this trip, at some point between one of his ten presentations to advisers, that someone made the connection between the two Andersons – Phil, the usually mild-mannered policy expert, and Angry, the gravel-throated Rose Tattoo singer known as one of the original bad boys of Australian rock ‘n’ roll.

“This is not the type of nickname that I would normally be embracing, however it does match how I feel about what has happened with the Dixon Advisory scandal and the CSLR,” Anderson (Phil, that is) said in a whitepaper released this week.

“Everywhere that we looked, we saw inequity and unfairness,” Anderson said. “The more we looked, the angrier we got.”

The whitepaper is the first in a 3-part FAAA analysis of the Dixon Advisory collapse. It’s far from the first effort by the FAAA to argue that the case has been mishandled and that the CSLR’s design is causing irreparable harm to an industry that can ill afford it. The FAAA has been a clear and consistent voice on the issues related to Dixons, and the whitepaper is a collation of them.

Set of grievances

The six “most significant” issues identified by Anderson are listed below.

1. E&P Financial Group walking away from its subsidiary Dixon Advisory and leaving virtually the entire mess for the rest of the advice profession to pick up.

2. The Government failing to deliver on a commitment of a prospective scheme (in which the financial advice sector would only be expected to pick up the costs of claims after the scheme started), and instead launching the scheme with a massive overhang of legacy compensation to be paid.

3. The Government committing to picking up the first 12 months of costs and claims for the CSLR, but then reducing that to less than three months and only covering one Dixon Advisory claim.

4. The Government failing to disclose anything about Dixon Advisory or the likely cost in the Explanatory Memorandum to the CSLR legislation, and failing to do a regulation impact statement for the CSLR.

5. ASIC failing to take action against Dixon Advisory in a timely manner and then only focussing on advice issues in their ultimate civil penalty action.

6. ASIC postponing the end date of Dixon Advisory’s AFCA membership which seemingly has enabled multiple hundreds of extra claims in the final months.

Infuriating the profession

In the first release, Anderson goes into detail about the role of E&P Financial Group and the apparent lack of accountability shown by Dixons Advisory parent group.

“The fact that E&P Financial Group (E&P) simply put its subsidiary Dixon Advisory into administration in full knowledge of the consequences for clients and the rest of the financial advice profession, and in the context of the expected establishment of the CSLR, is very concerning,” he said.

He makes the point that after Dixon went into administration, E&P subsequently folded many of its advisers into another subsidiary, Evans and Partners. This meant that while the rest of the industry is charged with paying for Dixon’s malfeasance (via the CSLR), its parent group, E&P, managed to benefit from bringing residual client revenue back on board.

Yet while ‘Angry Anderson’ has a bone to pick with E&P, his real ire is being reserved for the whitepaper’s next edition, when he addresses a system that punishes the good for the sins of the bad.

“Why should advisers who do the right thing be paying for the misconduct of Dixon Advisory?” he says.