Monday 27th June 2022

Supply-side remains the biggest contributor to inflation

After years of benign levels of inflation, the "beast" as it is known, reared its ugly head once again in April 2021, just as the world was emerging from the pandemic.

After years of benign levels of inflation, the “beast” as it is known, reared its ugly head once again in April 2021, just as the world was emerging from the pandemic. From lower, more acceptable rates in 2021, the rate of increases in prices in many parts of the developed world is now at or near record levels, and in some cases over 8 per cent.

Naturally, such an important input into the economy and determinant of central bank policy has seen a division of opinions. There is a growing chorus of “experts” delivering consternation on central banks for “not doing enough” or letting inflation get out of control, and plenty suggesting it is simply the result of the once-in-a hundred-years pandemic.

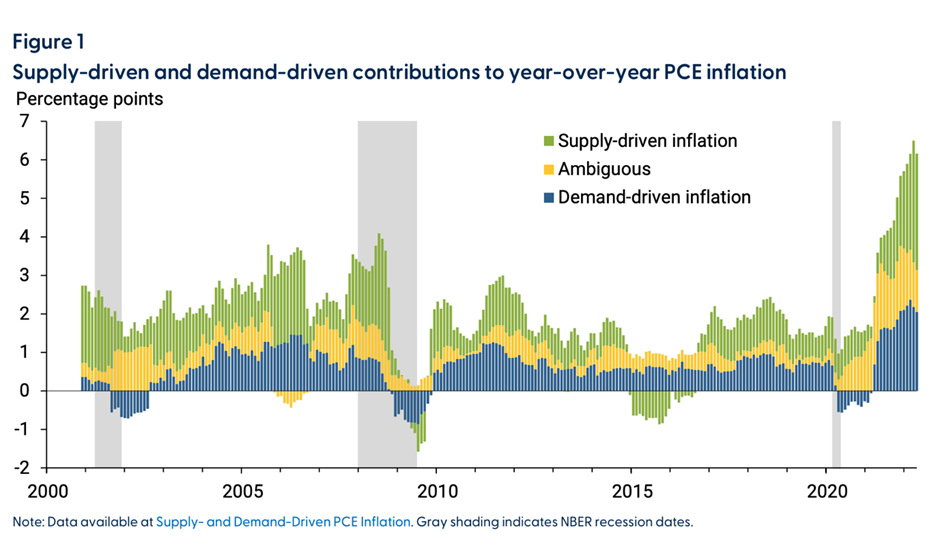

Adam Shapiro, an economic researcher at the Federal Reserve Bank of San Francisco, has been looking more deeply into the factors driving inflation, and this week released a paper titled How much do supply and demand drive inflation? The paper leveraged the growing range of data available in an attempt to answer the question that every investor and policy maker wants to know.

In his analysis, Shapiro separated every factor within the core personal consumption expenditure (PCE) and other inflation measures and sought to identify “demand-driven” versus “supply-driven” categories. Using decades of history, the analysis relied on the simple microeconomic assumptions that demand-driven inflation occurred when both price and quantity supply increased, and supply-driven when only price increased in a given month.

While this is an oversimplification of extensive data and analysis undertaken, it offers a rare insight into the workings of the economy. As Shapiro explained “the extent to which either supply or demand factors are responsible for higher inflation levels has important implications for monetary policy. As Fed Chair Powell stated in a recent interview, “What [the Fed] can control is demand, we can’t really affect supply with our policies…so the question whether we can execute a soft landing or not, it may actually depend on factors that we don’t control.”

According to Shapiro, “the decline in inflation at the onset of the pandemic was driven by a decrease in demand, whilst the surge of inflation in March 2021 was mainly due to the increase in demand-driven factors.” This was a result of the end of public health policies, and massive stimulus being delivered into American’s pockets. Put simply, most of these issues likely wouldn’t be here if not for the pandemic.

“Inflation has remained at levels well above the Federal Reserve’s inflation goal for over a year,” explained Shapiro, with his analysis suggesting that only about one-third of the current rate of inflation in the Personal Consumption Index (or PCE) is due clearly to demand-driven factors. That is, more than two-thirds of the current inflation rate is due to supply-side factors or other “ambiguous” influences.

More specifically, supply-side factors, which include labour shortages, the mass retirement of Americans, low inventories and transport costs have contributed to at least half of the current inflation rate. Important to note is that these “have been rising more recently” with demand factors one-third and falling. The data supporting these trends is shown in the table below.

Concluding the paper, Shapiro warns that “because supply shocks raise prices and suppress economic activity, the prevalence of supply-related factors raises the risk of entering a period of low growth and elevated inflation levels.

“This risk depends crucially on how long labor shortages and global supply disruptions persist. While supply disruptions are widely expected to ease this year, this outcome is highly uncertain,” he contends.

Drew is editor of The Inside Network's publications and a principal adviser at Wattle Partners.