Monday 24th July 2023

'Opaque' private credit purveyors add value, but quality is key: Mason Stevens

The proliferation of private credit providers in recent years is a boon for investors, explains Andrew Ash from Mason Stevens. But the attraction of diversification and returns comes with several caveats that investors should consider.

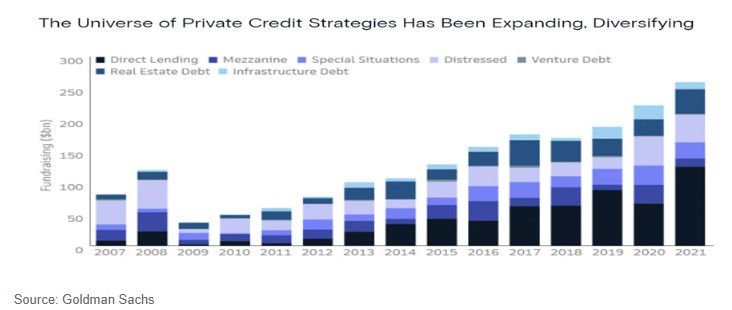

The provision of private credit investments has exploded in the last decade, driven forward by the reticence of banks and, until 2022 at least, ultra-low interest rate that sent investors scurrying for alternative and relatively non-correlated sources of return. The market is well entrenched, according to Mason Stevens head of manager research Andrew Ash, but investors need to remain vigilant about their allocation to private credit and the quality of providers they add to their portfolio.

By its very nature, Ash (pictured) described in a recent ‘Macro & Markets’ note, private credit is an “opaque” investment sector with less surety and liquidity than most others.

There has been a “mini gold rush” in private credit, he explained, which has attracted a broad spectrum of providers that haven’t had the chance to prove their mettle.

“There are numerous managers that have been running for only a few years and have limited heritage as a private credit manager. That’s not to say that a number of these newer providers can’t ultimately be successful through time, but that as of yet they haven’t been tested through a cycle.”

For investors, private credit’s attraction should come with a degree of caution, he warns. The first thing to look out for is to what degree these providers, especially the adolescent ones, invite concentration risk.

“Either by design or because they are still in the early stages of FUM growth, many private credit strategies look particularly concentrated,” he said. “This might be concentration in terms of holdings e.g. only having single digit or low double digit number of portfolio holdings. It is also often sector concentration, for example a strategy that just invests in the property sector.”

Managers can take approaches that mitigate this risk, he continued, by being senior secured or having strong covenants include in their loans. “However, it’s important to understand that this only reduces a degree of risk. Many of these strategies are highly concentrated, and it requires an appropriate assessment of whether the returns on offer are commensurate with this risk.”

“Virtually all Private Credit managers have done well from a relative performance perspective in recent years.”

As private credit is based on lending, liquidity (or lack thereof) will also be a constant consideration. But understanding the liquidity trade-off means appreciating that things aren’t always black and white.

“This is an illiquid investment class and the majority of holdings in most managers’ portfolios are not investments that could be readily sold ahead of maturity,” he said. “This is not a problem in and of itself, but understanding this profile and ensuring a fund is structured accordingly in terms of any potential redemptions is important. A notionally more liquid offering may not actually be a positive because of the mismatch this creates in environment where a weight of clients look to liquidate holdings.”

Cast your eye

Further consideration of private credit extends to bifurcations within valuations and inherent volatility, Ash explained.

The value of private credit investments are determined by the fund manager, which is often given as being steady and stable.

“While this approach has a certain logic given these holdings are illiquid and there isn’t explicit public market pricing, it also has the potential to create a false sense of security around the risks in a sub-investment grade portfolio, and an adverse reaction to a change in the unit price if and when a meaningful impairment occurs,” Ash said, adding that some other managers use separate valuations or “public and private reference points” to mark the market at intervals, proving what Mason Stevens sees as a better sense of portfolio valuation.

As ever, Ash explained, advisers and investors also need to cast an eye over the experience and alignment of the private credit provider. What is the breadth of experience across their team, and is their any significant key person risk?

Of course, he pointed out, the credit quality of the underlying investments should be a major consideration, as well as the fees charged by the provider to research them and structure deals.

‘Worth spending time’

None of these considerations, should, in isolation, preclude private credit investment, Ash explained. But they should remain considerations for any investor.

“A high-quality private credit manager can be an important source of additional returns and diversification within an overall portfolio. However, in a space that is by definition more opaque, it is important to do your due diligence,” he said.

“Virtually all private credit managers have done well from a relative performance perspective in recent years. As we approach a point in the economic cycle, however, where risks of a recession have become more elevated, it’s worth spending the time ensuring your private credit allocations are right-sized and with high-quality managers.”

Tahn is former managing editor across The Inside Network's three publications.