Thursday 4th August 2022

Holes revealed in new fund disclosure regulations

Morningstar has released a research paper citing how "abysmal" Australia's portfolio holdings disclosure requirements are for superannuation funds.

At a time when the Australian Prudential Regulation Authority (APRA) is calling on Australian superannuation fund trustees to improve the frequency and methodology used in unlisted asset valuations, Morningstar has released a research paper citing how “abysmal” Australia’s portfolio holdings disclosure requirements are for superannuation funds when compared to those of other countries.

According to Morningstar’s Grant Kennaway, head of manager selection, Australia’s compulsory superannuation system operates “in a dark void for investors.” A consistent finding from Morningstar’s Global Investor Experience studies, which has analysed the retail investor experience across 26 markets, is that Australia has the feeblest investment fund disclosure requirements related to superannuation funds on the planet.

“Put simply, Australian investors have limited regulated rights to know what securities (stocks and bonds) their investment and superannuation funds hold in their portfolios,” says Kennaway.

“Australia’s current portfolio holdings regulations offer little value to Australian investors and do not exceed the lowest bar that Morningstar sees in disclosure regulations in other global markets. In Australia’s compulsory superannuation system, investors’ best interests are not being served by weak portfolio holdings disclosure regulations,” he says.

The flaws in the Australian Portfolio Holdings Disclosure Regulations released in November 2021 are many, according to Morningstar. This guide was developed after the Australian Custodial Services Association (ACSA) worked with both the Australian Prudential Regulation Authority (APRA) and the Australian Securities & Investments Commission (ASIC) to produce the regulations.

The new regulations only require a semi-annual disclosure by superannuation funds and do not cover managed funds. Unless a fund is a related party to an Australian registrable superannuation entity (RSE) and managing superannuation fund assets, there will be no portfolio disclosure obligations on fund managers. Morningstar has raised several concerns about the regulations.

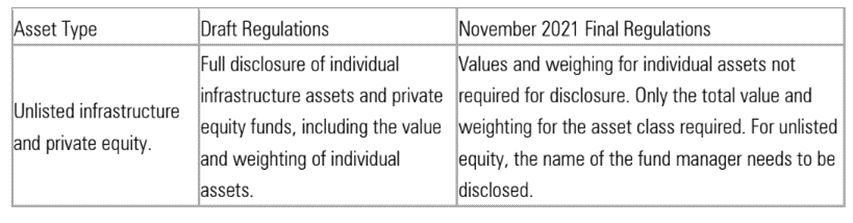

First, for unlisted infrastructure and private equity held by super funds, the values and weightings for individual assets are not required to be disclosed. Only the total value and weighting for the asset class are required. For unlisted equity, only the name of the fund manager needs to be disclosed, which leads to ambiguity about the assets actually being held by the super fund.

Second, the disclosure requirement of simple asset types like bonds without further details about credit quality leads to ambiguous reporting and makes these disclosures meaningless. “Simply listing the issuer of a bond tells investors nothing about its credit quality and interest-rate risk,” says Kennaway.

Third, if a superannuation fund were to invest in an external bond fund, “it need only disclose the name of the fund manager, obscuring whether the investment was in Australian government debt or emerging-market bonds, and so on,” says Kennaway.

“Fourth, Australians looking to invest sustainably have no regulatory enforced way to know if they are exposed to fossil fuels. For example, the external bond fund may be exposed to the debt of a company involved in fossil fuel industries or another industry segment that does not align to an investor’s values.”

More topically, the current disclosure requirements for unlisted infrastructure and private equity are “appallingly weak”, according to Kennaway. Following industry lobbying, draft regulations to require disclosure of the values and weightings of individual assets were significantly watered-down in November 2021, so that the regulated disclosures for derivatives and unlisted assets are only required on an aggregate basis. Individual attributes for derivatives and specific dollar values for individual unlisted infrastructure assets and private equity are not required.

Similarly, for unlisted property, the values and weighting for individual assets do not need to be disclosed, just the aggregate total value of holdings. This is a materially lower standard than the Australian Real Estate Investment Trust (A-REIT) sector, which must disclose net tangible assets (NTA) values based on individual property valuations every six months.

According to analysis from lawyers Philip Marquet and Geoff Sanders at Allens, the new disclosure requirements were good news for superannuation trustees and their external managers because they were much simpler than the exposure draft regulations suggested they might be.

“In a significant departure from the exposure draft, the regulations now allow for a range of assets to be disclosed on an aggregated basis. Overall, this should materially simplify the amount of disclosure required and (except perhaps in limited circumstances) should provide greater protection for commercially sensitive information,” the lawyers write.

“While the requirements still require look-through disclosure to the first non-associated entity level of a fund’s holding structure, the importance of that test has been greatly diminished by the introduction of a distinction between ‘internally managed’ or ‘externally managed’ investments. That is, for unlisted asset types (that is is, unlisted equities, property, infrastructure and alternatives) as well as fixed-income assets, the key question for trustees is now whether the relevant assets are ‘internally managed’ or ‘externally managed’, rather than whether an investment is controlled or not controlled by the trustee.”

Importantly, where such assets are ‘externally managed’, the value of those assets is only required to be disclosed on an aggregated basis, with a single line item referring to all such assets managed by the relevant fund manager: in other words, the very problem that Kennaway says leads to less important information being disclosed to investors about their superannuation funds.

“If superannuation funds do not have look-through knowledge on their underlying assets each quarter-end, the industry has material issues. It’s not credible for superannuation funds to argue they should be held to a lower disclosure and valuation standard than other global markets or the local A-REITs sector,” says Kennaway.

Nicki is an experienced journalist writing across three publications.