Monday 11th December 2023

Head-to-Head: The emerging market edge

Active managers with sector-specific knowledge really flex their muscles when dealing with countries in the midst of sustainable economic development. In this data-driven comparison, Mishan Dahia from Atchison Consultants looks at two prominent emerging funds.

Put simply, emerging markets are almost anything that falls outside the definition of a developed market such as the US, Australia or Europe.

More specifically, emerging markets (EMs) are those in the process of sustainable economic development, like China and Indonesia, but that meet size and liquidity requirements in terms of their share market and meet market accessibility criteria regarding foreign ownership.

Emerging markets have historically been seen as attractive due to their potentially higher economic growth rates compared to developed economies, while also benefiting from a rising middle class, population growth, plus development of urbanisation, technology and infrastructure. The ability to gain exposure to undervalued opportunities and invest in inefficient markets where company research is limited at best, lends itself to active managers with sector specific and region-specific expertise.

Head-to-head

Below are two EM funds that have been randomly selected to go head-to-head in a comparison of their styles and approach. Note that their suitability for portfolios has not been considered.

Investment approach

- UBS has a high conviction strategy that invests in EM equities, taking meaningful positions and seeking to identify the best opportunities to add value. The fund aims to outperform (after management fees) the MSCI Emerging Markets Net Total Return Index over a rolling 3 to 5 years.

- Warakirri invests in high quality global emerging market equities, holding a high conviction portfolio of 20 to 40 companies over 3 or more years. Warakirri believe that superior investment returns rely on fundamental investment research, experience, and good judgement.

5 Year performance

The last few years have been a challenging period for emerging markets, which are dominated by China, as investors have remained close to home in US markets, while more recently Chinese growth prospects dwindled.

That said, both funds outperformed the benchmark over the last month. Warakirri was bolstered by consumer staples, Dino Polska SA and FEMSA, along with consumer discretionary via Coway Co., Ltd. For the month Chinese positions in Tencent and Alibaba weighed on the index, finishing down -3.80 per cent and -3.67 per cent in absolute terms.

Over one year, UBS outperformed Warakirri by +3.70 per cent, and the benchmark outperformed both funds. In contrast, over 3 years Warakirri outperformed UBS by +4.09 per cent, suggesting differing conditions (such as sector, region, tracking error, cyclical v growth positioning, top holding conviction) that favour cyclical versus growth equities favour either of these strategies.

Risk metrics

Volatility is the most common measure of risk, with Warakirri showing higher volatility (12.83) compared to UBS (10.82). UBS has a slightly higher beta than the market at 1.05, indicating that it’s more sensitive to market movements than the average. Conversely, Warakirri is less sensitive to market movements than the average with a beta of 0.94 over 12 months.

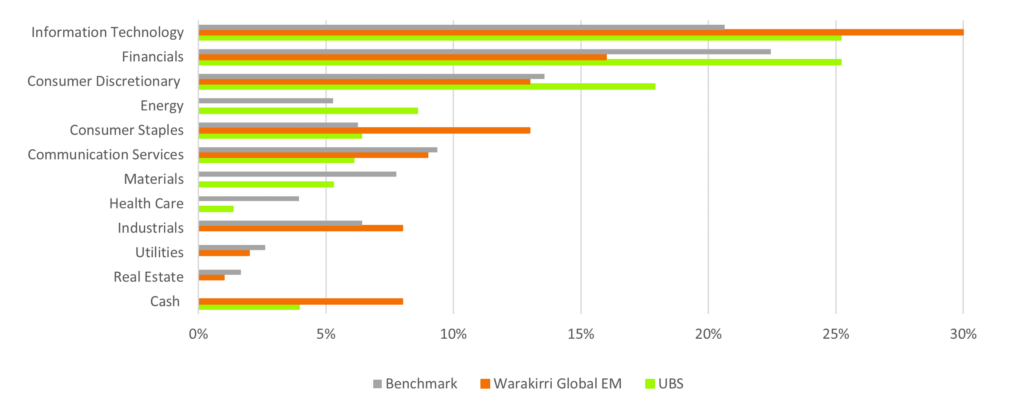

Sector exposure

Warakirri, relative to the benchmark, is overweight Information Technology (+9.36 per cent) and Consumer Staples (+6.75 per cent). Contrastingly, UBS is overweight Financials (+2.75 per cent), Consumer Discretionary (+4.33 per cent), and Energy (+3.32 per cent).

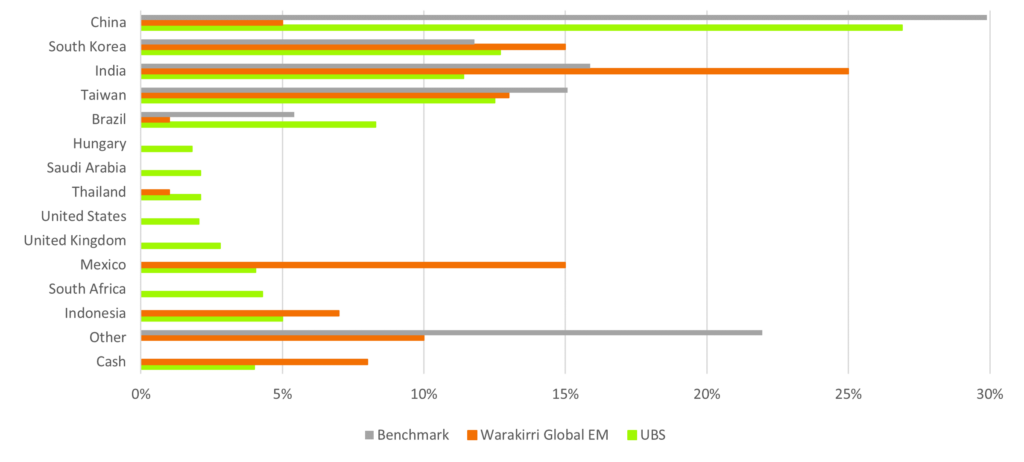

Regional exposure

From a regional perspective Warakirri is overweight India +9.12 per cent and Mexico +15 per cent and heavily underweight China -24.89 per cent, along with Brazil -4.42 per cent. UBS is more benchmark aware from a regional perspective, with major holdings in China, South Korea and Taiwan.

Holdings

The three-year correlation analysis of 0.67 produced by FE Analytics highlights that when one fund’s performance changes by a certain percentage, the other tends to move in the same direction approximately 67 per cent of the time, but not necessarily by the same magnitude.

Note, correlation does not imply causation, and does not capture the entirety of the relationship.

Summary

If you seek Emerging Market positioning with less exposure to China -24.89 per cent, and overweight to India +9.12 per cent and Mexico +15 per cent, along with reasonable 3-year performance, Warakirri may be your preference.

However, if you seek a more benchmark aware manager that takes active positions with overweights to Mexico +4.05 per cent, Consumer Discretionary +4.33 per cent and Energy +3.32 per cent, along with reasonable one year performance, UBS may be more suitable.

*Important Note

Historical performance is not a true indicator of future performance. Conduct your own due diligence regarding underlying strategies, holdings, market conditions, along with understanding your clients’ goals and risk tolerances prior to making investment decisions. Expecting a fund to maintain their top position can often leave an investor underwhelmed in future periods. Data sourced from FE Analytics and fund websites.

Mishan is a columnist for The Inside Adviser and an expert on asset allocation and fund research.