Thursday 15th July 2021

Goodbye Mr. Bond

Multi-asset manager Ruffer LLP’s Rory McIvor tells the story of when he sat at Ruffer’s Victoria Street office in London, five years ago, across the table from two portfolio managers, when they asked him, “What is a bond?”

He ummed and ahh’d.

The interviewers gave him the textbook definition which he had failed to provide. Perhaps there is something to learn from this failure. Throughout history he says, bonds have been used for different purposes for different people in different environments. For the past half-century, they have been the cornerstone of balanced portfolios, offsetting more-volatile equities and were an appreciating asset as bond rates fell. But that hasn’t always been the case. And may not be the case for decades to come.

Ruffer’s Alex Lennard and Kate Forsyth recently presented a session titled, “Goodbye MR BOND” via Zoom conference; a thought-provoking title if nothing else.

Alex began by familiarising listeners with James Bond films. He says “007 finds himself in increasingly precarious situations while the villain says things like ‘Goodbye, Mr.Bond.’ The bad guy then leaves the room while James executes a miraculous escape.” The bond market is no different, he says.

Many have suggested that this long bull run in bonds and equities is coming to an end and have positioned their portfolios to this certainty. They’ve been proven wrong time and again as any correction has proved to be short-lived.

With that in mind, Ruffer isn’t calling an end to this bull market. What it is really looking to understand are the circumstances that have reinforced the bull market, the dynamics that could bring it to an end, and the consequences.

Alex says, “When yields are falling, prices are rising, everyone’s happy, but when yields rise everyone watches in fear.”

The US Federal Reserve has engineered a world in which US$16 trillion ($21.3 trillion) of bonds are on offer with negative yields. Investors are happy now to receive a lower return for taking more duration risk. There are four main villains that have the potential to bring bond bull markets to an end:

What has caused the end of previous bull bond markets?

- In 1994, Federal Reserve chief Allan Greenspan proved to be a double agent when his intra-meeting rate hikes shocked the market and volatility spiked as bond market participants just assumed there would be more to come. Yields spiked by 200 basis-points, taking down equity markets and hedge funds, too.

- In 2003 – The Bank of Japan tried to inject life into bond markets by threatening to taper bond buying.

- In 2020 – The Covid-19 crisis brought about a huge fiscal response.

Ruffer suggests that current Fed boss Jerome Powell must now convince bond market participants that the inflation is transitory, otherwise we could see a revolt. In short – ‘Don’t fight the Fed,’ remains the strategy.

If the sky is soon to fall, what do we do about it? And what are the consequences? Alex says “waiting for crisis to hit rather than dealing with asset allocation now, is akin to being hit by Mike Tyson.”

Face the spectre upfront.

Bond market selloffs can cause a rather painful loss and significant harm. Low bond yields have driven equity valuations sky high. And it’s of no surprise. Equities can continue to levitate provided rates and inflation remain low. So far inflation has risen a little and has shaken investors.

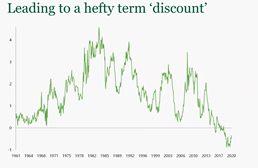

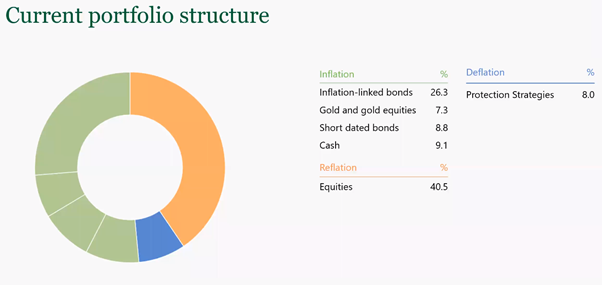

When inflation gets above 2.5%, equities and bonds increasingly move together as one. What it means for the 60/40 portfolio, which relies on negative correlation between these assets, is that it becomes unbalanced. Ruffer is seeing greater opportunities in a number of areas:

- Should the cost of borrowing rise with rates, banks are likely to become more profitable.

- Europe – Positioning becomes less extreme, markets become less prone to a sell-off as vaccine program starts to accelerate, and consumers open wallets to more stimulus.

- Real assets – Inflation linked assets will rise. Gold, oil, wheat.

Ishan is an experienced journalist covering The Insider Adviser publication.