Friday 7th June 2024

Examining the case for small and mid-cap funds

The potential for small and mid-cap companies to outperform the bigger players on indices is clear, with liquidity expected to increase as inflation comes off the boil and money flows into the economy. So which funds are best positioned to take advantage?

When examining the global equities market, the MSCI All Country World Index shows that large cap companies dominate the index with 70 per cent of the total, while small-cap companies represent only 15 per cent and mid-caps account for the 15-30 per cent of the index.

In terms of risk and return profiles, global small cap companies can generally outperform large caps over the longer periods, although this comes with higher risk. Listed mid-cap companies can typically outperform large caps and generally fall short of small caps but do so with significantly lower risk.

This underscores the attractiveness of funds which hold these small and mid-cap companies, especially in the current economic climate where government expenditure and liquidity are expected to increase in the latter half of 2024.

Two key points drive the case for small and mid-cap funds:

- High quality mid-cap funds can potentially hold the leading large-cap companies of tomorrow.

- The lack of coverage and research of small cap companies, in comparison to their large-cap counterparts, have left the opportunity wide open for astute small-cap fund managers to generate alpha or favourable returns for their investors, who are willing to take on the higher risk.

Small and mid-cap funds often hold companies which operate in high-growth industries or niche markets, where they can achieve higher earnings growth compared to their larger counterparts. This enhanced earnings growth usually translate into superior stock performance and attractive returns for investors.

Secondly, small and mid-cap funds can tend to hold smaller cap companies which exhibit a more innovative and entrepreneurial culture, often leading the way in technological advancements and new product developments. This innovation can drive substantial business growth and overall increase shareholder value for the investor.

These small and mid-cap companies are frequently acquisition targets for larger corporations seeking to expand their market share or enter new markets. This acquisition potential can lead to significant capital gains for investors in small and mid-cap funds.

However, investing in small and mid-cap companies carries inherent risks that directly impact funds allocating to this sub-sector. These companies are more leveraged than large-cap firms, making them highly sensitive to interest rate changes, which can increase borrowing costs and impact profitability.

Small and mid-cap companies are more volatile and sensitive to market fluctuations, economic downturns and geopolitical events, leading to potential short-term losses. Lower trading volumes also make these stocks less liquid, posing challenges for funds attempting to buy or sell large positions without significantly impacting stock prices.

Hence, professionally managing a portfolio of world small and mid-cap companies involves several key challenges. A key factor being the nature of these companies, which necessitates close monitoring of interest rate and economic trends. Fund managers must therefore navigate economic cycles, balancing growth opportunities during times of economic expansion or growth with capital preservation during downturns, in addition to ensuring adequate diversification is spread across sectors and geographies to mitigate risks.

Moreover, the wide valuation disparity vs large-cap companies add complexity, necessitating precise valuation techniques to identify undervalued companies with strong fundamentals and growth potential.

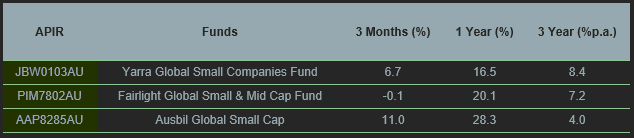

From the Atchison APL , there were a total of 45 global mid and small cap equity funds assessed as at 30 April 2024. With the average one-year return being 11 per cent, while the average three-year return was 8 per cent. Below are the top performing funds over the one and three-year periods.

Fairlight Global Small and Mid-Cap Fund

The Fairlight global small and mid-cap fund aims to deliver risk-adjusted returns through a disciplined, research-intensive approach, targeting an annual return of 8-12 per cent, while aiming to surpass the MSCI World SMID Index in AUD (net) benchmark by 3 per cent. The fund focuses on investing in 30-40 high-quality international companies with market caps between $500 million and $30 billion.

Yarra Global Small Companies

The Yarra Global Small Companies Fund aims to achieve medium-to-long-term capital growth by investing in smaller companies globally. Its target is to outperform the MSCI World small cap index by focusing on companies with market caps like those in the index. The fund uses a quantitative management approach combined with qualitative overlays, emphasizing fundamentally based stock selection, careful portfolio construction, and efficient implementation.

Ausbil Global Small-Cap Fund

The Ausbil Global SmallCap Fund aims to achieve long-term capital growth by investing in smaller companies globally, targeting returns that exceed the MSCI World Small Cap Net Total Return (TR) Index in AUD. The fund follows an active management approach that seeks to exploit inefficiencies within the small-cap asset class by investing in high-quality companies with unrecognized growth potential at attractive valuations.