Thursday 4th April 2024

Diversification unlocking the unique appeal of Asian equities

Asian market equities stand out as a beacon for growth-oriented investors, propelled by the region's rapid technological advancements, robust economic development and increasing integration into the global economy.

The Asian equity markets are currently poised for growth amidst the global economic flux, with potential gains arising from the U.S. Federal Reserve’s anticipated interest rate cuts. This policy shift is likely to weaken the dollar and redirect investments towards the Asian and emerging markets, benefitting developing regions like India and Southeast Asia due to favourable monetary conditions.

The lower correlation of Asian equities vs US, UK and Australian equities provides diversification benefits, helping investors to spread risk and potentially enhance returns in a global equities portfolio. In terms of characteristics, Asian equities are often marked by higher volatility and distinct risk factors including geopolitical tensions and policy uncertainties, which can affect market performance more significantly than in developed economies.

Due to ongoing development and growth, exposure to the Asian markets via equities can often present a compelling narrative of opportunity for investors seeking diversification and growth, with some key drivers in this region being:

Technological innovation: Asian economies, particularly China, South Korea and Taiwan, are at the forefront of technological innovation and giants in electronics, semiconductors and e-commerce. This technological prowess not only fuels domestic growth but also positions these markets as pivotal players in the global supply chains.

Demographic and urbanisation trends: The region’s significant population and ongoing urbanisation efforts continue to drive consumer demand, presenting lucrative opportunities for industries ranging from retail to financial services.

Policy reforms and economic integration: Initiatives like China’s Belt and Road and the Regional Comprehensive Economic Partnership (RCEP) enhance trade links and economic integration, fostering a conducive environment for investment.

However, the landscape is not devoid of challenges. Risks that warrant careful navigation in this environment includes:

Geopolitical tensions: Ongoing U.S.-China tensions and other regional disputes can introduce volatility, impacting trade and investment flows.

Regulatory risks: Regulatory changes, particularly in China, have recently shaken sectors like technology and private education, underscoring the importance of regulatory due diligence.

Market volatility: While offering high growth potential, Asian equities can be susceptible to periods of heightened volatility, influenced by both global economic shifts and local market sentiments.

Professionally managing a concentrated portfolio of Asian market equities requires a nuanced understanding of the above risks, ensuring that investments are not only well-placed to capture growth but are also resilient against the ebbs and flows of the unique Asian market dynamics.

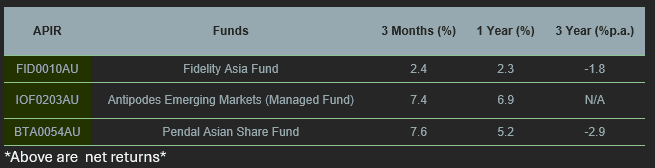

From the Atchison APL there were a total 34 fund managers assessed, whereby the average 1 year return was 0.0 per cent and average 3-year return was -5.8 per cent, as this was primarily due to the lagging Chinese economy.

Below are the top three performing managers based on the Atchison APL over one year and three years.

Antipodes Emerging Markets emerged as the top performer over the one year (+6.9 per cent) while was Fidelity Asia Fund was leader of the pack over the three-year period (-1.8 per cent).

Antipodes Emerging Markets (Managed Fund)

Antipodes aims to capitalise on the market’s propensity for overreaction, seeking out investments with significant safety margins to construct portfolios focused on high conviction and capital preservation.

While primarily targeting Asian equities, the fund has the flexibility to diversify into a broad array of assets, including cash, fixed income, various company securities (like options and convertible notes), derivatives across numerous categories, currency contracts, interests in other investment schemes, unlisted and off-market securities, and even physical assets such as bullion and real estate.

The fund’s objective is to deliver absolute returns that surpass its benchmark over a typical investment cycle of 3-5 years. As at 29th February, the fund’s top contributors were Sk Square (Korean company specialising in the fields of Information and Communications Technology, semiconductor businesses, and blockchain) and KB Financial Group (Korean financial services provider).

Fidelity Asia Fund

The Fidelity Asia Fund adopts a bottom-up strategy, focusing on strong investment prospects across the Asia Pacific excluding Japan. This strategy results in a focused portfolio of 20 to 35 stocks. The fund may allocate up to 10 per cent in any single stock, based on its appealing risk/reward ratio identified through in-depth research.

Emphasising a high conviction investment philosophy, the fund commits to companies that are well-understood and believed to have substantial return potential. It avoids adding any stock to the portfolio that doesn’t meet its criteria for adequate return potential, resulting in typically lower volatility compared to its benchmark index.

The foundation of the portfolio is built on large-cap, financially robust companies known for stable cash flows, providing a safeguard during volatile market periods. The fund’s concentrated nature is balanced by diversification and risk management practices.

The funds top overweight positions as at 29th February were Focus Media Technology (Chinese company dedicated to producing and selling computers, computer accessories, and digital communication devices) and HDFC Bank (Indian Bank).

Pendal Asian Share Fund

The Pendal Asian Share Fund, actively managed by JOHCM, invests in a diverse range of Asian equities, specifically excluding those from Japan and Australia.

Its objective is to outperform the MSCI AC Asia ex Japan (Standard) Index (Net Dividends) in AUD, aiming for superior returns over the medium to long term, prior to the deduction of fees, costs and taxes.

The fund has a higher allocation to (India 25 per cent), (Taiwan 20.2 per cent) and (China 16.4 per cent) with Taiwan Semiconductor being one of its top holdings as at 29th February.