Thursday 24th February 2022

CRE debt continues to perform during periods of rising rates

With our long period of near-zero interest rates seemingly at an end, every investor’s attention turns to the balance of their portfolio.

Conventional wisdom is that now is the time to rethink exposure to real estate investments because rising interest rates are a drag on property values and rising inflation benefits other asset classes.

There are certainly signs of this anxiety playing out, with the S&P 200 A-REIT index down more than 10 per cent – correction territory – in the weeks since hitting a record high on the first trading day of the year. In the same period, the broader S&P 200 is off just 3 per cent.

The fall in A-REITS is understandable. As a yield-driven investment option, the attraction of A-REITs suffers when yields on relatively risk-free bonds rise in line with inflation expectations, as they have in recent months. In addition, A-REITs’ underlying assets can be affected by monetary tightening; property valuation growth may slow or even fall, earnings and distributions are exposed to rate increases and debt funding costs rise, crimping expansion and investment opportunities.

But there is another asset class that offers exposure to real estate and that has not only proven its ability to ride out periods of rising interest rates but could actually benefit – we are talking about commercial real estate debt. A fast-growing asset class now accessible to all investors through specialist funds managed by private debt experts.

The alternative real estate financing sector grew out of the global financial crisis, after banks were forced to tighten their lending criteria and hold more capital. Non-bank lenders like Qualitas, offering more flexibility and faster turnarounds to borrowers and attractive terms to lenders, stepped in to fill the gap at a premium.

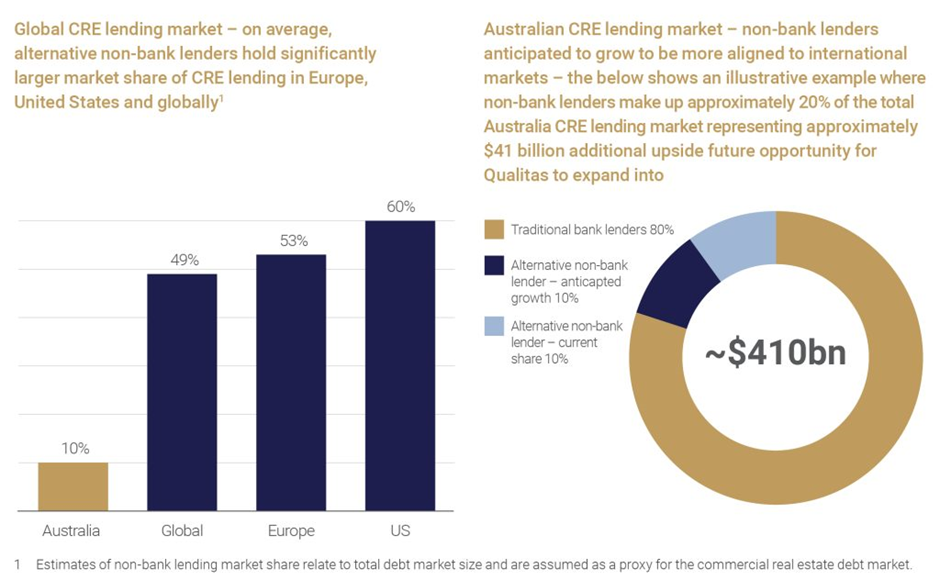

Today, these non-bank lenders have about 10 per cent of the CRE debt market but their share continues to grow and there is no reason it will not trend towards global averages closer to 49 per cent – and up to 60 per cent in the US (see chart).

Today, private CRE debt offers relatively higher yields of 5-9 per cent, often paid monthly and secured against commercial property assets. And the end of record-low interest rates is likely to accelerate its appeal.

CRE debt yields are a combination of a base rate plus a margin on the loans, so any increase in the base rate caused by increases in official rates directly results in higher returns to investors, provided margins remain stable. As a result, in a CRE debt fund, which is typically not leveraged, a rate increase corresponds directly to an increase in revenue that can be paid out to investors as distributions.

This is not the case with traditional ADIs like the major banks. A rate increase may result in additional revenue for the bank, but also leads to higher cost of funding its loans via higher rates paid to depositors. The same generally applies in respect of wholesale funding.

Any kind of lending entails some risk. In a rising interest rate environment, asset valuations come under pressure and impact loan-to-valuation ratios (LVR). An experienced alternative real estate investment manager, like Qualitas with its 13 years of experience through market cycles, is responsible for managing such risks.

A diligent manager will carefully monitor LVRs and underlying asset security values, adjusting their portfolios accordingly. In addition to offering diversification, Qualitas has found it is possible to achieve similar revenues even with lower LVRs.

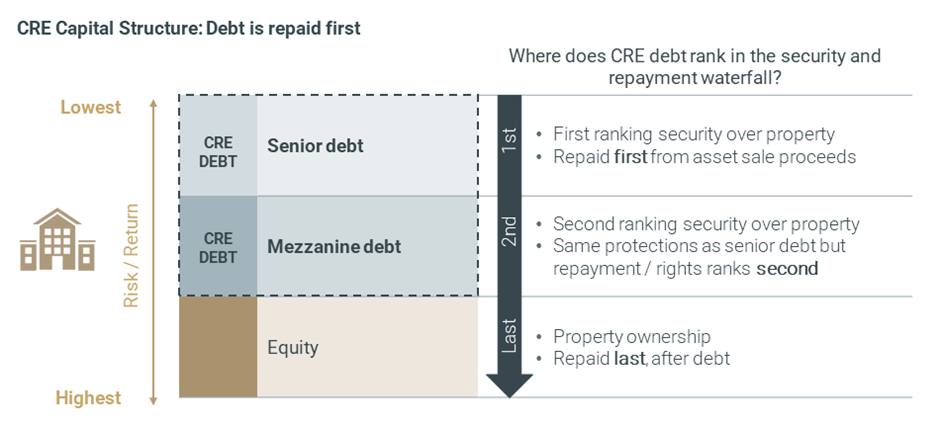

The other benefit of CRE debt over CRE equity is security. Compared to CRE equity like A-REITs, CRE debt ranks higher in the capital structure and is more secure due to the real property mortgage security. Put simply, in the event of default, equity is paid back only after debtors have first been repaid (see chart).

There aren’t many opportunities for investors to achieve equity-like returns with debt-style security, but alternative real estate investment managers offer exactly that.

For investors who are attracted to commercial property and the yield it delivers but dislike the risk of rising rates and how they might affect it, professionally managed commercial real estate debt may be an appealing alternative.

In a rising interest rate environment, CRE debt has the potential to offer similar or more attractive yields but with greater capital preservation and maintaining exposure to property. It’s an income-focused investment with a proven ability to ride out periods of rising rates.

Disclosure

Qualitas Disclosure This document has been prepared by Qualitas Securities Pty Ltd (ACN 136 451 128) (Qualitas Securities), holder of Australian Financial Services Licence number 342242. Qualitas Securities and its related bodies corporate and affiliates constitute the Qualitas group (Qualitas).

The information contained herein is for informational purposes only and does not constitute an offer to issue or arrange to issue financial products. The information contained herein is not financial product advice. This document has been prepared without taking into account the investment objectives, financial situation or particular needs of any particular person. Before making an investment decision, you should read the publicly available information carefully and consider, with or without the assistance of a financial adviser, whether an investment is appropriate in light of your particular investment needs, objectives and financial circumstances. Past performance is not an indicator of future performance.

No member of Qualitas gives any guarantee or assurance as to the performance or the repayment of capital. All data in this document has been calculated using the most accurate sources available, however any rates or totals manually calculated may differ from those shown due to rounding. Figures may also differ from those previously disclosed due to adjustments made following period end.