Thursday 18th January 2024

Australia's best value hunters: Top 5 large value equity funds unveiled

Each of these five fund managers focus on finding undervalued stocks that have significant potential for growth. And in Australia – on a performance level, over a 3 year term – they're currently the best at what they do.

Value investing is a cornerstone of Warren Buffett’s investment strategy and hinges on identifying market inefficiencies whereby the underlying stocks are priced below their intrinsic value.

The Australia Large Value Equity category consists of funds that predominantly invest in affordable, slower-growing large cap Australian companies. These companies are generally marked by their lower valuations, reduced price ratios and higher dividends, alongside modest growth in earnings and sales.

Historically, value fund managers tend to outperform their growth-oriented counterparts during times of down markets or stagnant market conditions.

Specific characteristics of value stocks are listed below:

- Typically priced lower than peers based on ratios such as price-to-earnings (P/E), price-to-book (P/B) and dividend yield

- Often have strong fundamentals – solid earnings, dividends and cash flow

- Usually exhibit less volatility compared to growth stocks

- Commonly are consistent dividend payers

- Companies that are currently out of favour in the market but have strong potential for a turnaround

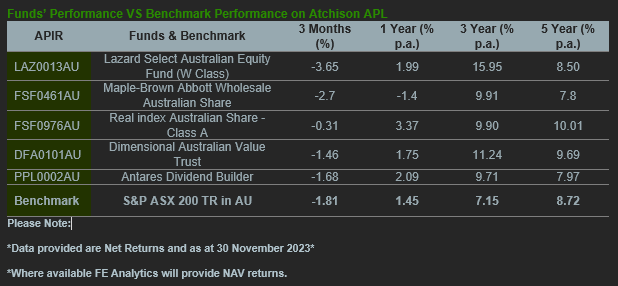

As at November 30, 2023, the top five performers were derived from eighty-six Australian large value equity funds listed on the Atchison Consultants Approved Product List.

These eighty-six funds have returned an average of seven per cent over the past three years.

Over a three-year time frame, the Lazard Select Australian Equity Fund (W Class) was the clear top performer, returning 15.95 per cent and outperforming the S&P ASX200 benchmark by 8.8 per cent.

Fund insights

Lazard Select Australian Equity Fund (W Class)

With a dynamic portfolio of 12 to 30 stocks, Lazard’s Select Australian Equity Fund actively selects ASX-listed companies believed to be trading below intrinsic value.

The stated goal of the fund is to outperform the S&P/ASX 200 Accumulation Index by 5 per cent annually over five-year periods, even investing in IPOs slated for listing within three months, without generally hedging against currency fluctuations.

Some of Lazard’s top holdings consists of QBE at 9.9 per cent, Rio Tinto at 8.4 per cent and Woodside Energy with 6.9 per cent.

Recent contributors to the fund’s outsized returns include Mayne Pharma and Collins Foods, with poorly performing holdings in AMP and South 32 pulling it back somewhat.

Maple-Brown Abbott Wholesale Australian Share

Maple-Brown Abbott, as a bottom-up stock picker, concentrating on in-depth fundamental analysis to identify undervalued stocks. The research process aims to pinpoint stocks trading below their true value, focusing on high-conviction picks.

Cash allocation is strategically used to mitigate return volatility.

The primary objective of the fund is to outperform the S&P/ASX 200 Accumulation Index’s performance, before fees and taxes, over rolling four-year periods.

Some of the fund’s top holdings includes, Aristocrat Leisure Limited at 17 per cent, National Australia Bank Limited at 6.17 per cent and Rio Tinto with 5.8 per cent of the portfolio.

Ansell and Link Administration Holdings have done well for the fund, while Woodside Energy Group and Santos have underperformed.

Realindex Australian Share – Class A

The Realindex fund crafts a value-tilted Australian company portfolio using accounting measures and factors like quality, value, and momentum.

It offers lower costs, reduced turnover, and greater diversification. This approach aims to payoff with long-term returns exceeding the benchmark, emphasising accounting-based weighting in its portfolio construction.

The largest stock active positions are Fortescue at 4.7 per cent, BlueScope Steel at 1.7 per cent and Woolworths Group with 3.1 per cent.

Fortescue has performed well for the fund, while AGL Energy Limited and CSL were recent detractors.

Dimensional Australian Value Trust

The Trust aims for long term capital growth by investing in a diversified mix of Australian Value Companies. It doesn’t target specific returns against a benchmark but uses the S&P/ASX 300 Index for performance comparison only.

This index is not a reflection of the Trust’s actual or intended asset allocation, and the Trust’s performance may significantly vary from the index.

Antares Dividend Builder

Antares focuses on a portfolio of high-yielding Australian equities, emphasising dividend growth and franked income while maintaining low turnover for reduced capital gains tax.

The strategy targets share in the top quartile for dividend yield relative to the Benchmark, while seeking undervalued companies with potential for capital growth.

It aims for regular, tax-effective dividend income surpassing the Benchmark and moderate capital appreciation over five-year periods.

Top holdings include:

- ANZ Group Holdings Limited

- BHP Group Ltd

- National Australia Bank Limited

Summary of Performances

Each value fund manager has adopted distinct strategies in the pursuit of outperforming the benchmark.

Lazard focuses on undervalued ASX-listed companies, targeting a 5 per cent annual outperformance over the S&P/ASX 200 Accumulation Index, including investments in near-term IPOs. This strategy has clearly served them well over the 3 year term.

Maple-Brown Abbott emphasizes in-depth analysis to select undervalued stocks, using cash allocation to reduce volatility, while Antares aims for high-yield equities with dividend growth, seeking tax-efficient income and moderate capital appreciation.

Real index applies accounting measures and factors like quality and momentum for a value-oriented, diversified portfolio, aiming to surpass the S&P/ASX 200 Accumulation Index over five years.