Nick Dignam from Fortitude Investment Partners shares insights with Lachlan Maddock from Fortitude Investment Partners on how a diversified portfolio in mid-market private equity is structured. The Inside Adviser

The world of alternative investments is at a crossroads. As markets defy expectations and liquidity concerns take centre stage, investors find themselves forced to rethink how they deploy capital in an increasingly complex environment.

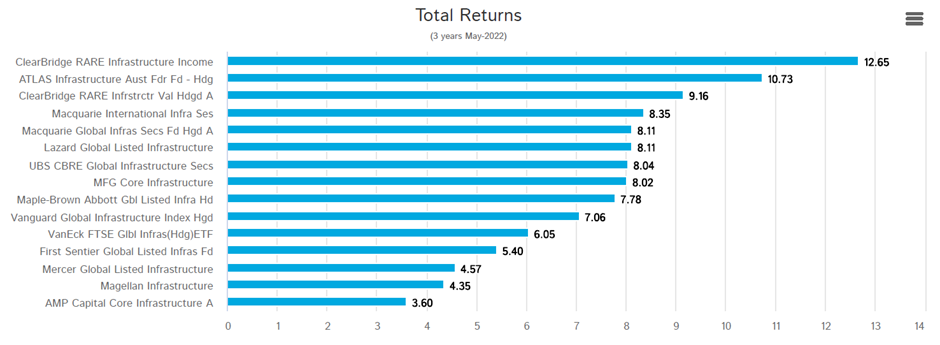

A closer look at the top inflation-linked strategies in 2022

In a year marred by rising volatility, inflation, war and supply disruptions, sharemarkets fought a battle between positives and negatives which weighed on equities as investors rotated out of growth assets and into safety. The RBA is tipping GDP to grow by 4.25 per cent over 2022, and by 2 per cent over 2023. Inflation is expected to increase by 4.5 percent by June 2023 and 3.25 percent by year’s end.

For that reason, financial advisers need to find a way to protect the value of their clients’ investments, because inflation eats away at the value of money. One asset class that acts as a hedge against inflation is infrastructure assets. As prices rise around the world, fuelled by soaring energy and supply chain constraints, specific types of infrastructure companies can act as a inflation hedge if they tick two boxes. Magellan Financial Group says: “First, the company must own or operate assets that behave like monopolies. Second, the services provided by the company must be essential for a community to function efficiently. Such companies have predictable cash flows that make them attractive defensive assets.”

Infrastructure companies can pass-through rising costs without affecting demand thereby protecting investors from the erosive pressures of inflation. Infrastructure assets offer a defensive business model, inflation protection and income. Given the COVID headwinds of the last two years are now behind us, global travel is becoming busier, which is a positive to transport organisations such as airports and toll roads. An increase in demand for income and defence against rising inflation have all created a compelling case for investment in infrastructure.

The main sectors within infrastructure are utilities, toll roads, airports, railroads, energy infrastructure, communications (mobile phone and broadcast towers). Here are our top five picks, but for the purposes of this article, I will only go through the first two:

- ClearBridge RARE Infrastructure Income

- ATLAS Infrastructure Aust Fund

- Magellan Financial Group Core Infrastructure

- Macquarie International Infrastructure Securities

- IFM Investors

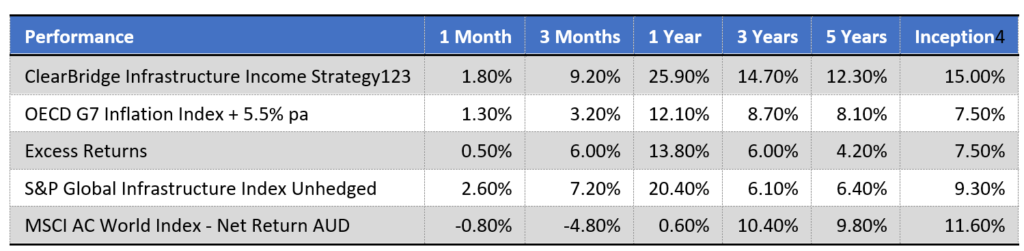

The ClearBridge RARE Infrastructure Income fund has long been a favourite among investors because of its enviable track record and inflation-linked capital growth that provides a reliable source of income. This total return is achieved via a range of listed securities spread across the globe in both developed and emerging markets. The fund outperformed global equities for the month of May, returning 1.8 per cent versus the OECD G7 Inflation Index, which returned 1.3 percent. It did however, underperform the S&P Global Infrastructure Index, which returned 2.6 percent. According to ClearBridge, it

“primarily owns and operates contracted renewable generation assets in the US. It also owns and operates conventional generation and thermal infrastructure assets… On a regional level, the strategy’s largest exposure is in the US and Canada (59%) and consists of exposure to regulated and contracted utilities (36%) and economically-sensitive ‘user-pays’ infrastructure (23%).”

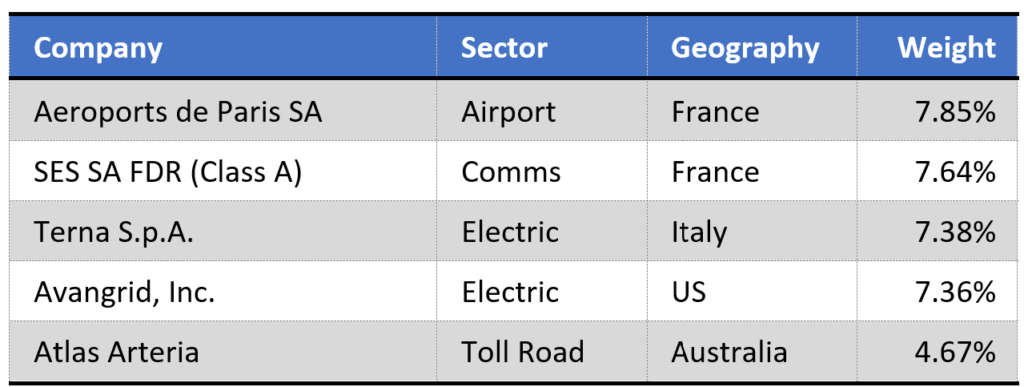

The ATLAS Infrastructure Australia Fund gives exposure to high-quality infrastructure equities in OECD countries only and is a high-conviction strategy that also monitors and manage carbon and climate change risk exposures within set tolerances. The fund returned 1.9 per cent for May and 22.3 per cent for the year.

The fund posted a 1.87% (net of fees) return, which beat the benchmark return of 1.25%. The main contributors in the period were holdings in Avangrid, Consolidated Edison and SES. The main detractors were Norfolk Southern Corporation, Enel SpA and PG&E Corporation. ATLAS says, “Enel SpA is one of Europe’s largest integrated utilities that engages in electricity distribution, generation and supply across the EU, Latin America and the US, and is a monopoly operator of Italy’s electricity distribution grid. Because of the Russian invasion of Ukraine, Enel is well-positioned to benefit from an expected acceleration of climate transition policy in Europe over the coming years.’

Real estate and infrastructure outperform other asset classes during previous inflationary periods, and this is primarily due to their revenue streams being linked to inflation and therefore being an expense pass-through. For example, Transurban receives concessions that allow it to increase prices on many of its roads by the greater of inflation or 4 per cent a year. So, it makes sense for advisers to have their clients in an infrastructure fund because real assets perform well in periods of higher inflation.