Nick Dignam from Fortitude Investment Partners shares insights with Lachlan Maddock from Fortitude Investment Partners on how a diversified portfolio in mid-market private equity is structured. The Inside Adviser

The world of alternative investments is at a crossroads. As markets defy expectations and liquidity concerns take centre stage, investors find themselves forced to rethink how they deploy capital in an increasingly complex environment.

In search of the ultimate inflation hedge

Whilst insurance companies are typicalled considered “technical, mundane and incredibly boring,” Ed Waller and his team at Yarra Capital Management believe there is a time, a price and a place for almost everything. And for the first time in close to a decade they believe insurance is now compelling.

Deputy Portfolio Manager of the Yarra Ex-20 Australian Equities Fund, Co-Portfolio Manager for the Yarra Real Assets Securities Fund at Yarra Capital Management, Ed Waller has put together a short research note outlining eight simple reasons for the compelling nature of the insurance sector for investors.

Here are Wallers either simple reasons for considering an insurance stock in your portfolio:

- The sector is one amongst a handful that benefits from higher interest rates, with a 1% increase in rates equating to 10-20% earnings upside

- It has potentially the best industry structure, operating as a functional oligopoly; the two major domestic insurers have a 68% market share and have successfully prioritised pricing

- Insurers are causes of inflation rather than suffering from it; Home and Car Insurance premiums are rising 5%+ p.a., and commercial insurance at 10%+ p.a.

- After a surge in natural hazards, it ‘probably can’t get much worse’; the July to October 2021 period saw natural hazard costs at 8-times normal levels

- Unlike other sectors, there will be no post-COVID earnings slump; insurers have experienced three years of trough earnings, with FY22 earnings estimates for IAG and Suncorp ~20-30% below FY19

- The sector raised billions in business interruption reserves, much of which of which we expect is surplus to requirements and will be returned to investors

- In an overheated market (yes still!), insurers remain attractively valued and trade in line with long run historic multiples

- The sentiment towards the sector and expectations probably couldn’t be worse (3-year average underperformance of 30%), meaning not a lot has to go right!

Looking at the above reasons the Yarra Australian Equities Fund’s largest sector overweights are through exposures in QBE and IAG.

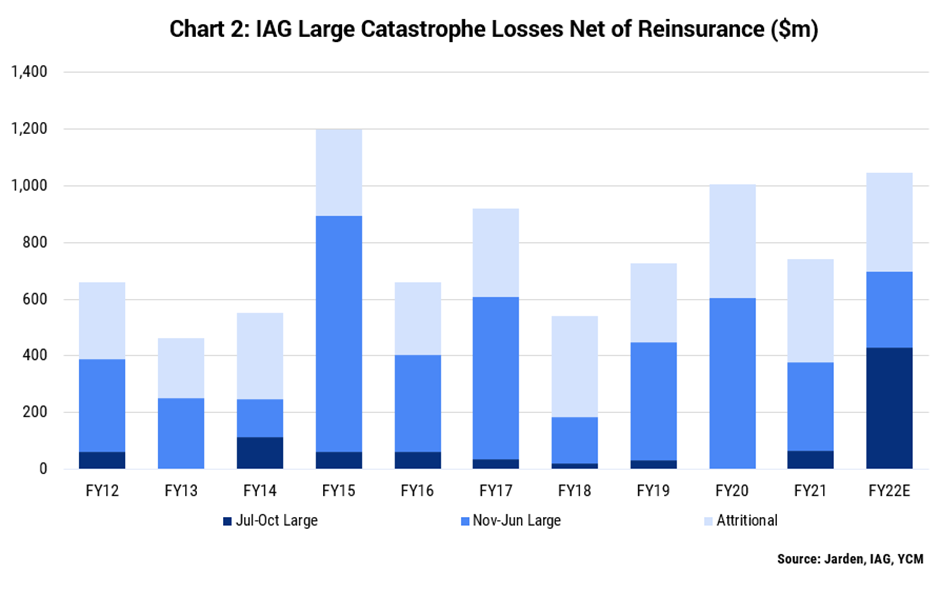

Waller says, “QBE is seeing strong topline growth through both double-digit rate increases (Refer Chart 1) and policyholder growth and has the most interest rate leverage.”

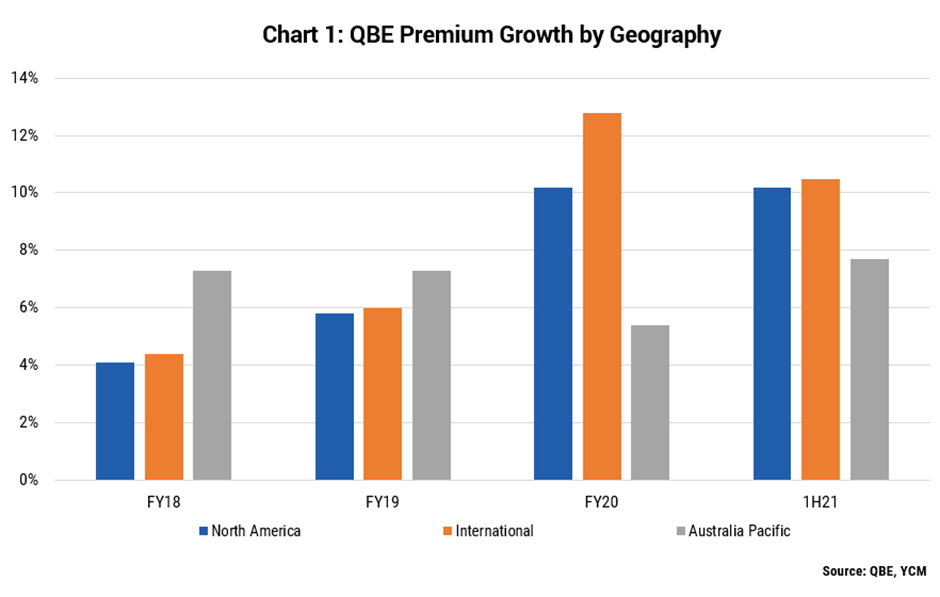

IAG on the other hand has been ‘de-rated’ after experiencing 8-times normal losses in the first 4 months of FY22 (refer Chart 2). Waller says it was a genuine once off – and its $1.15bn in largely unnecessary business interruption provisions speaks to capital flexibility.

All in all, Waller says “Both QBE and IAG represent examples of companies trading in line with their long run average valuation multiples, which are an exception in the current market where 75% of Industrials are trading above long run average multiples.”