Monday 2nd November 2020

Shining brightly - The true value of gold and how to use it

Gold has an almost mythical quality to it but assessing its true investment value doesn’t need to be shrouded in mystery. Some investors may still shy away from an asset viewed as difficult to accurately price or predict, but perhaps they are focused on the wrong metrics. Understanding the true value of gold is more than just its spot price, but also how it works in a portfolio.

The drivers of gold prices

Gold is both consumption and investment-driven, so where the prices of some assets can be easily linked to physical supply and demand, with gold, there are more variables. According to the World Gold Council, there are four broad sets of drivers to indicate gold’s performance[1].

- Economic expansion: gold is used in jewellery, technology, and long-term savings. These are areas that experience a boost in times of economic growth. These are also periods where inflation and interest rates may rise, and gold is traditionally viewed as a hedge against inflation.

- Risk and uncertainty: gold has traditionally acted as a store of value in uncertain times and its demand can go up in market downturns, for example, demand increased in the early months of the global COVID-19 pandemic.

- Opportunity costs: the costs and returns of other assets, such as bonds and currencies, can increase or decrease investor interest in gold.

- Momentum: price trends, the use of riskier investments, and general investment flows can direct demand for and therefore the price of gold.

That is not to say that all these drivers contribute equally to gold prices at all points in time. One or a combination of the drivers can be responsible for short-term spikes or falls, though prices typically even out over the longer term.

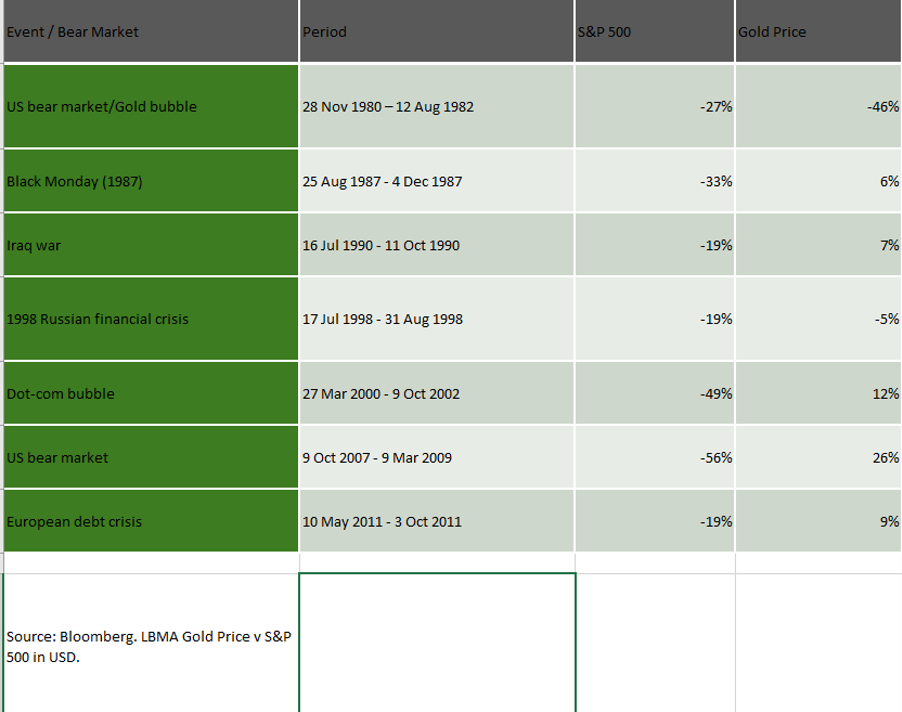

For example, just as unexpected geopolitical events (the risk and uncertainty driver) can have a dramatic short-term influence on equity markets, they can also affect gold prices – usually in the opposite direction to equities, as investors seek safe havens.

You can see this in the below table, which shows the one-year price change of gold and global equity markets following major events, over the past 50 years.

Gold returns in extreme conditions compared to equities

Calculating gold prices

These four key drivers all influence the resulting gold price. Gold prices are set by the London Bullion Market Association (LBMA), which also incorporates specific global standards for gold sales and receipt. It uses a process of electronic financial review of online auctions to update gold prices in real-time, along with twice-daily meetings, a panel, oversight committee, and the involvement of multiple banks and ICE Benchmark Administration[2].

Gold’s investment value

For investors used to calculating the value of investments using metrics related to coupon or dividend value (i.e for bonds or equities), an asset like gold can pose more challenges.

Some institutions create their own models to estimate gold’s value now and into the future, which can be helpful for investors.

For example, the World Gold Council, in conjunction with Oxford Economics, has created a customisable free tool known as Qaurum, that is designed to estimate how gold may perform in different environments, by creating estimates of expected price, volatility and opportunity costs.

WisdomTree also has a proprietary model which uses changes in the value of the US dollar, consumer price index (CPI) inflation, changes in the nominal yields on ten-year US Treasuries and investment sentiment to forecast the value of gold[3].

Investors may like to take an alternative approach by considering gold’s value in relation to its interaction within a portfolio and with other assets held in that portfolio.

Safe-haven fact or fiction?

Gold is included in portfolios for a myriad of reasons – diversification, growth, as a hedge against inflation, and for a volatility safe-haven. These reasons are backed by the data.

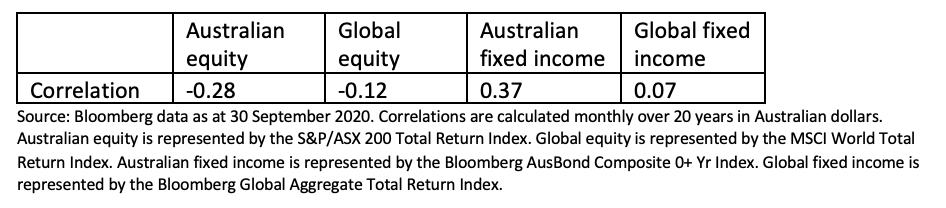

For a start, gold has a low (and at times negative) correlation to other asset classes. This means it has the ability to perform differently in a portfolio, with the potential to offer positive performance in volatile periods. As such, it can offer diversification in a portfolio and a volatility safe-haven.

The correlation between gold and major asset classes over 20 years

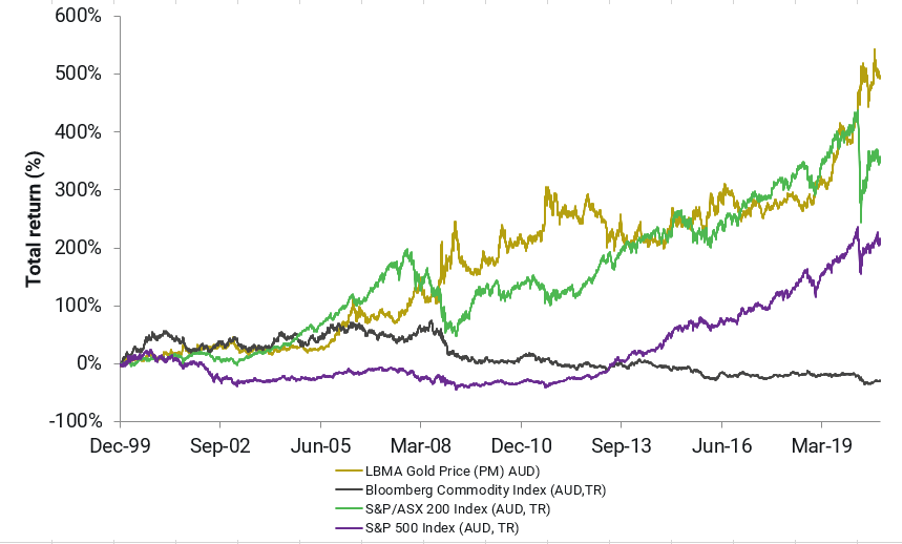

From a growth perspective, gold has also offered positive performance over the longer-term, as shown in the chart below, compared to other asset classes, including equities.

Gold 20 year performance against other asset classes

Finally, research has indicated that including gold in a portfolio may improve overall performance and risk.

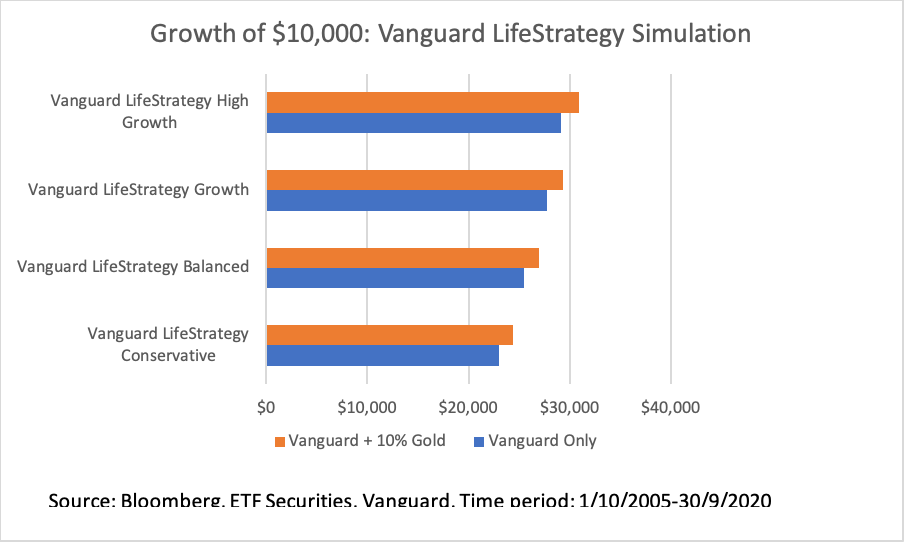

Analysis completed by the World Gold Council simulated a hypothetical pension portfolio with and without commodities or gold, finding that risk-adjusted returns improved with gold more than with commodities[4].

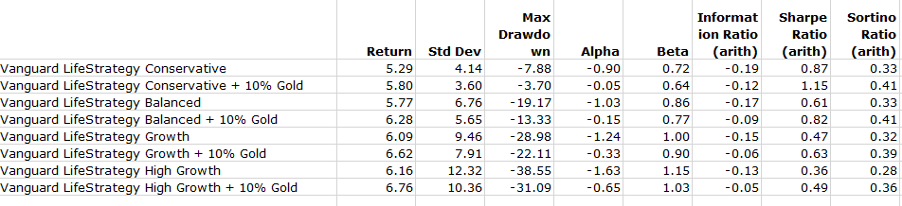

ETF Securities conducted similar analysis using the diversified Vanguard “LifeStrategy” Funds, with and without a 10% allocation to gold from a starting base of $10,000, over a 15 year period, and found similar results.

Having evaluated gold for a portfolio and decided to include it, the next question for many investors is one of allocation.

What portion of a portfolio should be in gold?

Answers to this question range but have traditionally spread from 2%-10% of a portfolio depending on the risk tolerance and market conditions. For many investors, taking a flexible approach may be the answer, dialling up or down allocations based on your portfolio needs and market activity.

For example, Stockspot increased its gold allocation to 12% a few years ago based on its market views[5].

In explaining this approach more recently, Chris Brycki, CEO and Founder of Stockspot, said, “we saw that the correlation between bonds and shares was moving from being more negative to being more positive, which meant that, in theory, bonds weren’t going to provide the same level of protection in a share market fall. And that indeed happened earlier this year when the share markets fell. Actually, for a period of that fall, bonds fell as well, until central banks got up and decided to stand behind the fixed income markets. And as a result, gold really did protect portfolios in a way that was advantageous, and something that bonds weren’t able to do.”

The Harvard Gold and Economy Observer also holds a flexible view based on risk tolerance to drive gold allocation, but positions gold as a form of portfolio insurance, with the level allocated dependent on the investor’s need to offset potential losses from market activity.

At the end of the day, how much to allocate depends on the overall portfolio – but as with anything in life, both too much and too little of a good thing can have similar consequences.

Investing in gold

Investors have a range of options when it comes to gold investment. Some examples include:

- Gold bullion

- Shares in gold mining companies

- Exchange traded funds (ETFs)

- Synthetic options, such as gold futures

Each option has different associated risks and the actual exposure to gold can vary.

Gold-backed ETFs can be a suitable option for many portfolios as they offer a low-cost exposure, without the need for physical storage. They also tend to be liquid and easy to use, simply requiring a share trading account to access. Gold-backed ETFs are literally as described, where physical gold is purchased and stored by a fund manager as part of a trust and investors buy units in the trust for exposure to the market movements of gold.

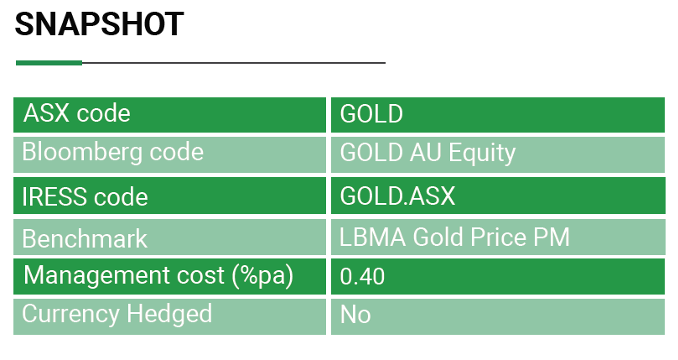

An example of this is ETFS Physical Gold (ASX Code: GOLD), the first gold-backed ETF in the world, which uses allocated gold, that investors can choose to redeem their units for.

Investors should be aware of the risks of investing in gold, as well as specific risks related to how they choose their exposure before investing.

For example, investing in gold and ETFs carries market risk. This is the loss of value due to movements in price. Changes in the price of gold relative to an investors purchase price create gains or losses. Or alternatively, an investment may be subject to liquidity risk, that is, the risk that the physical holding can’t be sold quickly or at a fair price in the market.

True value

While gold’s value may not be as simple as calculating coupons, its value in an investment portfolio is hard to question. Gold has little in the way of competition in the form of other assets offering its level of diversification, ability to hedge against inflation and potential for improved risk metrics and performance. The age-old investment is still a timeless portfolio addition.

ETFS Metal Securities Australia Limited (ACN 101 465 383) (CAR: 001274650) is the issuer of shares in ETFS Physical Gold (ASX Code: GOLD) (“the Fund”). The prospectus contains all of the details of the offer of shares in the Company. Any investment decision should only be considered after reading the relevant offer document in full.

Written by Evan Metcalf, Head of Product, ETF Securities

Disclaimer:

This document is communicated by ETFS Management (AUS) Limited (Australian Financial Services Licence Number 466778) (“ETFS”). This document may not be reproduced, distributed or published by any recipient for any purpose. Under no circumstances is this document to be used or considered as an offer to sell, or a solicitation of an offer to buy, any securities, investments or other financial instruments and any investments should only be made on the basis of the relevant product disclosure statement which should be considered by any potential investor including any risks identified therein.

This document does not take into account your personal needs and financial circumstances. You should seek independent financial, legal, tax and other relevant advice having regard to your particular circumstances. Although we use reasonable efforts to obtain reliable, comprehensive information, we make no representation and give no warranty that it is accurate or complete.

Investments in any product issued by ETFS are subject to investment risk, including possible delays in repayment and loss of income and principal invested. Neither ETFS, ETFS Capital Limited nor any other member of the ETFS Capital Group guarantees the performance of any products issued by ETFS or the repayment of capital or any particular rate of return therefrom.

The value or return of an investment will fluctuate and investor may lose some or all of their investment. Past performance is not an indication of future performance.

Information current as at 30 September 2020.

[1] https://www.gold.org/goldhub/research/relevance-of-gold-as-a-strategic-asset-2020-individual

[2]https://www.sbcgold.com/blog/how-gold-prices-are-determined/

[3]https://www.etfstrategy.com/gold-how-we-value-the-precious-metal-94857/

[4]https://www.gold.org/download/file/14226/Gold-versus-commodities.pdf