Thursday 26th October 2023

Inflation surprise halts Australian indices in their tracks

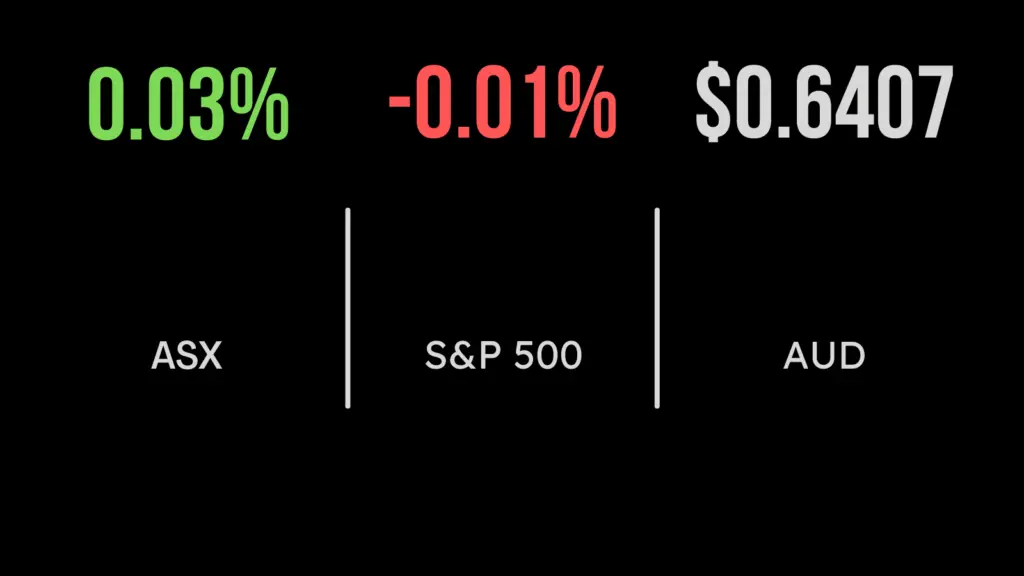

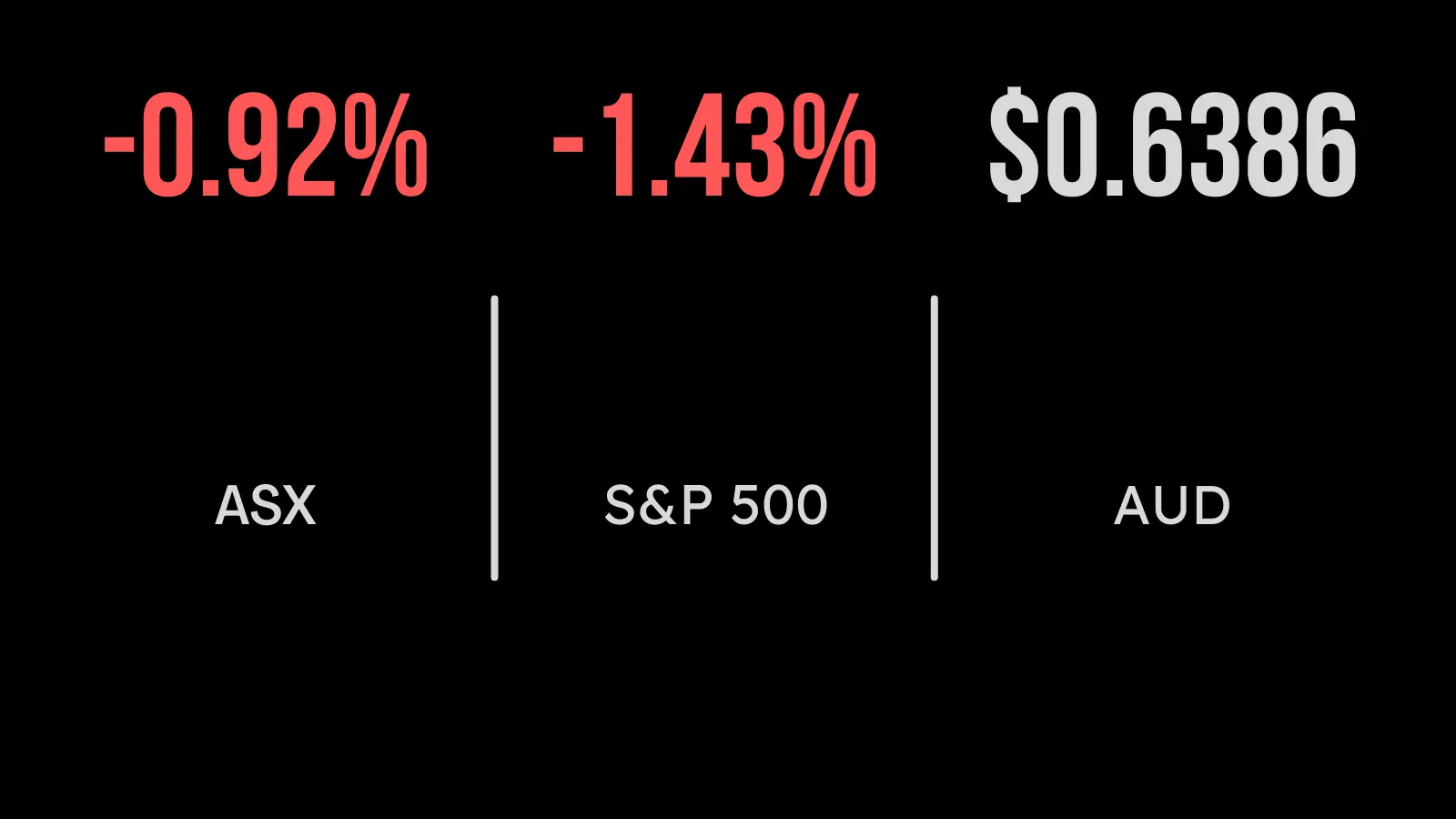

Surprisingly high inflation data stopped the Australian market from consolidating early gains on Wednesday, turning the day into a stalemate in terms of the indices. The benchmark S&P/ASX 200 closed 2.6 points lower, at 6,854, losing early gains. The broader All Ordinaries index, however, managed a 0.7-point gain, to 7,046.

Australia’s headline consumer price index (CPI) rose 1.2 per cent in the September quarter compared with April-June, the Australian Bureau of Statistics (ABS) reported. An economists’ survey had predicted a 1.1 per cent quarter-on-quarter rise, and the figure was up from 0.8 per cent. The core CPI measure also rose 1.2 per cent for the quarter, against a forecast of 1.1 per cent. In annual terms, core inflation was up 5.2 per cent, against a forecast of 5 per cent.

The strong core inflation figure was widely construed as virtually locking-in a 25-basis-point rate rise at the Reserve Bank board’s November meeting.

Firmer iron ore prices bolstered the resources sector, with BHP gaining $1.13, or 2.6 per cent, to $44.72; Fortescue Metals Group up 67 cents, or 3.1 per cent, to $22.02; and Rio Tinto advancing $2.67, or 2.4 per cent, to $116.27. Canadian-based high-grade iron ore producer Champion Iron closed 27 cents, or 4.4 per cent, higher at $6.38.

Iron ore and lithium miner Mineral Resources gained $2.66, or 4.6 per cent, to $60.09 after reaffirming its FY24 volume guidance. IGO, which produces nickel and lithium, eased 2 cents to $10.85.

Lithium producer Pilbara Minerals rose 9 cents, or 2.4 per cent, to $3.88; while fellow producer Allkem appreciated 38 cents, or 3.7 per cent, to $10.56.

Rare earths producer Lynas Rare Earths was up 30 cents, or 4.4 per cent, to $7.12. Canadian-based uranium project developer NexGen Energy Canada gained 52 cents, or 5.8 per cent, to $9.43, while Namibian-based uranium producer Paladin Energy strengthened 1.5 cents, or 1.6 per cent, to 96.5 cents, and Boss Energy, which is re-starting the Honeymoon uranium mine in South Australia, gained 15 cents, or 3.3 per cent, to $4.69.

Green splash for Kogan among the red

Online retailer Kogan spiked 39 cents, or 8.7 per cent, to $4.86 after its sales returned to quarter-on-quarter growth, despite continuing to fall in annual terms.

Property fund manager Dexus dropped 23 cents, or 3.3 per cent, to $6.70 after long-serving CEO Darren Steinberg announced that he was stepping down after 11 years with the company.

Woolworths’ first-quarter sales rose 5.3 per cent compared with a year ago – the shares dipped 72 cents, or 2 per cent, to $35.63. Wagering luminary Tabcorp lost 3.5 cents, or 4.1 per cent, to 81.5 cents after suffering a 34 per cent protest vote over executive pay at its annual general meeting.

Investment management firm Magellan dropped 19 cents, or 2.9 per cent, to $6.34 after announcing that chief executive David George was stepping down with immediate effect. Board director Andrew Formica will assume the role of executive chairman as the company searches for a replacement.

It was a red day for the big banks, with ANZ down 33 cents, or 1.3 per cent, to $24.85; National Australia Bank losing 24 cents, or 0.8 per cent, to $28.32; Westpac weakening 8 cents, or 0.4 per cent, to $20.80; and Commonwealth Bank sliding 72 cents, or 0.7 per cent, to $97.35.

Biotech heavyweight CSL eased $1.20, or 0.5 per cent, to $236.05. Telstra was up 8 cents, or 2.1 per cent, to $3.87.

Alphabet spells trouble for Wall Street

In the US, the broad S&P 500 index gave up 60.91 points, or 1.4 per cent, to 4,186.77, the blue-chip Dow Jones Industrial Average shed 105.45 points, or 0.3 per cent, to 33,035.93, and the tech-heavy Nasdaq Composite index walked back 318.65 points, or 2.4 per cent, to 12,821.22. The Nasdaq was dragged lower by a 9.5 per cent slump in Google’s parent Alphabet, which put in it worst day since March 2020, after revenue in its Google cloud unit came well below analyst estimates.

A rash of earning reports came out after the closing bell, with Facebook’s parent Meta and IBM both beating earnings and revenue estimates.

In the bond market, the US 10-year yield rose 13.5 basis points to 4.961 per cent, while the 2-year yield ended 7.8 basis points higher at 5.145 per cent.

Gold strengthened US$9.43, or 0.5 per cent, to US$1,982.11 an ounce. The global benchmark Brent crude oil grade rose US$2.06, or 2.3 per cent, to US$90.13 a barrel, while US West Texas Intermediate oil retreated 16 cents, or 0.2 per cent, to US$85.23 a barrel.

The Australian dollar is buying 62.9 US cents this morning, down from 63.77 cents at the ASX close on Wednesday.

James is an experienced senior journalist and editor of The Inside Network's publications.