Monday 16th January 2023

Higher rates biting into household wealth, with more pain to come

Household wealth in September recorded its third largest quarterly decline since the Australian Bureau of Statistics began keeping records in 1989. And wealth is likely to keep falling in the coming quarters, as the lagged effects of interest rate hikes flow through.

Australian household wealth has been severely dented by rising interest rates, falling by $279 billion in the September on declining property prices. While a big rise in term deposits and superannuation contributions helped to cushion the blow, wealth is likely to keep falling in 2023, with continuing weakness in property prices expected.

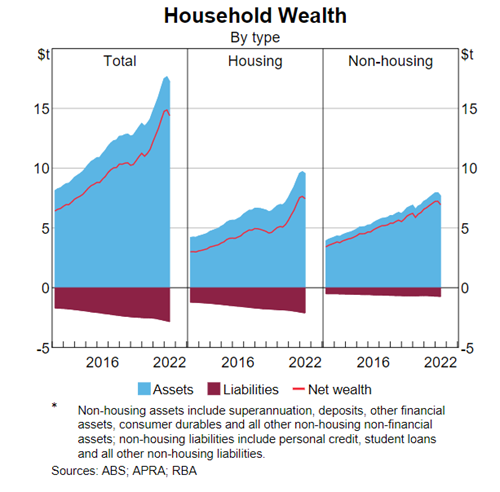

Household wealth fell for the second consecutive quarter, decreasing by 1.9 per cent or $276 billion to $14.2 trillion in the three months through September 2022, according to figures released this week by the Australian Bureau of Statistics (ABS). Wealth per capita fell 2.2 per cent or $12,050 to $545,532 per person. While property prices dropped, household liabilities rose $26 billion, driven by a $24.3 billion rise in housing loans reflecting increases in interest rates.

“This fall in household wealth was almost entirely driven by the decrease in the value of residential land and dwellings, which recorded its largest decline since December 2008,” says Katherine Keenan, ABS’ head of finance and wealth statistics.

According to Ryan Felsman, senior economist at CommSec, the drop in household wealth was also the third largest quarterly decline since records began in September 1989, and he expects further erosion in household finances in coming quarters.

“Household wealth has likely deteriorated further in the December quarter following further Reserve Bank rate hikes,” Felsman says. He notes that five-city aggregate dwelling values have fallen a further 2.8 per cent since September 30, which would wipe out another $360 billion from household wealth based on the ABS’ figures.

“That said, the Aussie [share market] benchmark S&P/ASX 200 index is up over 11 per cent since September 30, potentially offsetting some of the decline in property values,” Felsman adds. “But the Reserve Bank’s policy tightening cycle will ultimately determine the direction of household wealth in 2023.”

Residential property still dominates household wealth. A total of $10.1 trillion – around 71 per cent – of household wealth in the September quarter was stored in property, compared with $3.3 trillion in superannuation reserves. Australians also held $1.2 trillion in shares and $1.5 trillion in cash deposits, with deposits jumping by $50.5 billion during the quarter.

Diana Mousina (pictured), senior economist at AMP Australia, expects home prices to further decline about 10 per cent from current levels, which would also dent household wealth. “There could be some offset from share markets if there is a rally in equities, but it won’t be enough to offset the decline from home prices, as they are the majority of household wealth,” she says.

The softer fall in household wealth in the September quarter was due in part to an increase in household deposits, reflecting continued increases in term deposits attributable to rising interest rates and volatile share market conditions, the ABS said.

In other good news, the superannuation guarantee increased in the September quarter to 10.5 per cent from 10 per cent, which pushed up employer contributions and helped offset impacts from lower share markets.

Wealth still higher than pre-pandemic levels

Despite the decline in household wealth this year, the aggregate value of household assets was around six times larger than the aggregate value of household debt as at the end of the June quarter of 2022, compared to 5.5 times larger at the end of 2019, according to the Reserve Bank of Australia (see graph).

“Household net wealth has increased strongly over the past two years, including for the two-thirds of households that own their homes, notwithstanding recent declines in housing prices. Non-housing wealth has also increased since the start of the pandemic, reflecting increased saving; however, this will have been weighed down more recently by falling share prices,” the Reserve Bank said in its recent Financial Stability Review.

“Very low interest rates and strong growth in employment and income enabled households to continue to add to their already-large liquid saving buffers in the first half of 2022.”

The RBA earlier this month raised interest rates for the eight month in a row, to 3.1 per cent, their highest level in almost a decade. According to Commonwealth Bank economist Gareth Aird, the lagged impact of interest rate rises will hit home borrowers more fully next year, though he thinks official interest rates likely have almost peaked.

“We think we are near the end of the RBA’s tightening cycle and expect one further rate hike in the first quarter of 2023 that will take the cash rate to 3.35 per cent,” Aird said. “From there, we have the Reserve Bank of Australia on hold, as much slower growth in demand is expected to see inflation come down in 2023.”

Nicki is an experienced journalist writing across three publications.