Since the banking and financial services royal commission, smaller, independent, specialist wealth platforms have been able to grow their market share at the expense of their much larger ‘legacy’ rivals — and share investors have jumped on for the ride.

The first quarter of 2025 was a challenging one for US equities, but Francis Gannon from Royce Investment Partners, part of Franklin Templeton group of companies, says the conditions for small-caps to flourish may be forming.

Ex-20 option shines as banks and miners face growth headwinds in 2025 and beyond

At this point in the Australia’s market history, it’s a truism that banks and miners anchor the top end of the stock exchange, with their combined market capitalisation taking up 35 per cent of the ASX 200. But the flip side of this stranglehold is that the growth potential of large, behemoth companies like Westpac, ANZ, BHP and Rio Tinto is relatively limited.

These “low growth dinosaurs” can create a barrier to outperformance according to a recent whitepaper to Yarra Capital, and stifle the ability of investors to increase both earnings and capital value.

The case for cutting the top 20 companies out of a ASX 200 holding is a strong one based on the simple premise that these companies present little growth potential. But as Yarra’s Go beyond the point of low returns paper points out, there are further factors, both cyclical and topical, that strengthen the argument.

Bank malaise

The banks, for their part, are faced with a plethora of headwinds that should make a tricky path to growth even more difficult.

“Bank earnings per share peaked in 2017 and EPS is expected to be flat at best in FY25 due to stagnant revenue, rising costs and normalising bad debt expenses,” the paper states. “Share prices typically follow earnings, so it’s unsurprising that, with the exception of Commonwealth Bank, major bank share prices remain below their 2015 highs.”

“Over the last decade, the market structure of Australia’s banking system has deteriorated significantly,” Yarra adds, noting that consumer preferences have shifted from banks towards brokers for property loans, while digitally native competitors have taken market share in areas like consumer finance and foreign exchange.

The golden goose for Australian banks – home loan mortgages – is under siege due to the incursion of Macquarie and lower-tier providers who have brought more competition and compressed overall return-on-equity. Instead of 20 per cent credit growth on mortgages, the big banks are “struggling to achieve mortgage returns above their cost of capital”.

Undermined

For the miners, a long and sustained of growth is now on the cusp of being stifled by a confluence of factors, many of which relate to its biggest market, China.

Despite the sector’s poor track record in mergers and acquisitions, investing in Australia’s large iron ore miners was a highly profitable trade during the first two decades of the 21st century,” the paper states. “Today, the conditions that drove that success are fading. In China, which accounts for 71 per cent of the global seaborne market, demand for iron ore is stagnating due to a housing sector downturn and a maturing economy.”

The crux of China’s issue is the housing market, with consumption stagnating in the wake of the pandemic and the demand for steel weakening in the face of material oversupply. This reflects not just overbuild, the paper explains, but problematic demographics and linked maturing urbanisation trends. New housing builds, for example, have fallen 45 per cent below the 10-year average and 55 per cent below peak levels.

“While infrastructure and auto manufacturing have grown in line with the broader Chinese economy, they have not offset the decline in housing-related steel demand,” Yarra notes. “Even if Chinese housing starts to recover, the rapid growth seen in the early 2000s will not return.”

A recent AU$2 trillion stimulus package from the Chinese government prompted a rally in Australian mining shares, but there are questions over the medium term sustainability of these measures and whether they’re enough to arrest the commodity’s decline.

Smarter path

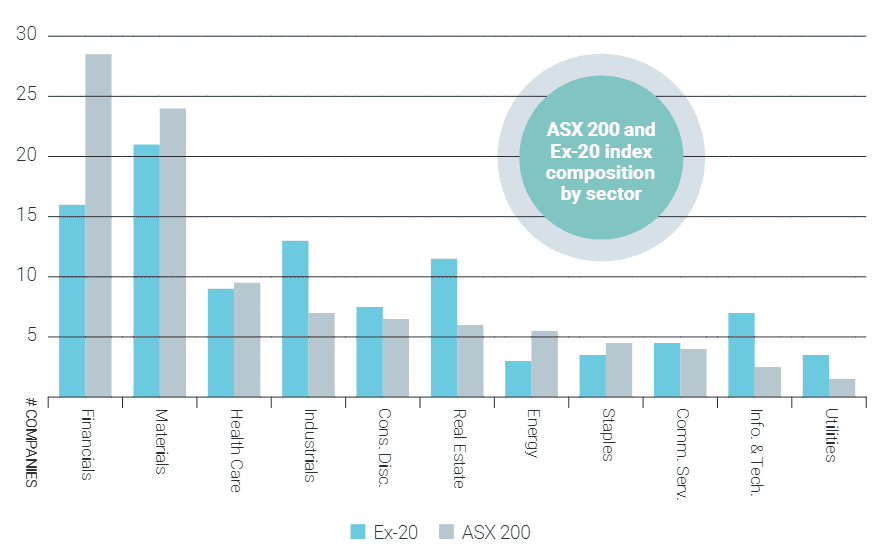

For investors looking at an ASX 200 holding, the grim growth prospects of the banks and miners may provide a reason to look at any exclusionary position, one that encompasses all the growth potential that comes outside the top 20, while still harnessing the strength and stability of well-capitalised and proven companies.

Due to its less efficient nature, the Ex-20 top 200 provides a much more fertile ground for growth, while it also targets high growth sectors with much stronger earnings potential. Yarra notes base metals like lithium and copper – core components in the drive for decarbonisation and increasingly essential in technology products like phones – as the kind of sectors that offer attractive growth.

It follows that Ex-20 holdings also provide greater diversification, with significantly lower concentration risk than an unsophisticated top-200 holding.

“While the top20 companies dominate the ASX, representing more than 60 per cent of the total market capitalisation, they also symbolise yesterday’s heroes,” the paper states, with no stock forecast to achieve 10 per cent or more revenue growth in 2025. “In contrast, 56 companies in the Ex-20 are projected to hit that mark, spanning sectors like technology, new media and battery minerals.

“The Ex-20 provides a way around sluggish growth, offering superior returns and lower risk than small caps, while reducing the systematic risks of over-concentration in specific sectors like banking and iron ore.”