Since the banking and financial services royal commission, smaller, independent, specialist wealth platforms have been able to grow their market share at the expense of their much larger ‘legacy’ rivals — and share investors have jumped on for the ride.

The first quarter of 2025 was a challenging one for US equities, but Francis Gannon from Royce Investment Partners, part of Franklin Templeton group of companies, says the conditions for small-caps to flourish may be forming.

ASX hits 7300 as record rally rolls on

ASX finishes at record high, The Reject Shop downgrades, energy leads the week

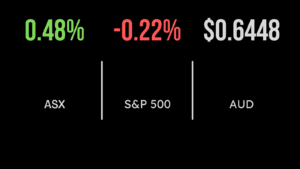

The ASX200 (ASX: XJO) broke 7,300 points for the first time, ultimately finishing up 0.5% on Friday and 1.6% for the week; three consecutive records.

On Friday it was 4X4 parts supplier ARB Corporation Limited (ASX: ARB) and Origin Energy (ASX: ORG) leading the way, jumping 6.3% and 5.4% respectively.

ARB is clearly benefitting from a lack of supply of new vehicles and closed borders, ensuring tourism stays at home.

Over the week, the IT sector was the only detractor, falling 1.1%. Both energy and utilities were up 8.5% and 5.8% each, the biggest contributors to the record finish.

The catalyst was the combination of an improving economic outlook and positive comments from OPEC+.

Energy companies led the weekly gains, with ORG up 15.7%, Worley Ltd (ASX: WOR) 15.6%, and Santos Ltd (ASX: STO) 12.2%.

Once again, recently listed data analyst Nuix Ltd (ASX: NXL) led the falls, down 23.2% in just five days.

Reject Shop Ltd (ASX: TRS) was among the biggest losers after the company flagged significant concern in its earnings outlook.

Foot traffic to CBD stores has struggled as expected, but even shopping malls have been lower than expected with management flagging a fall in like-for-like sales of 1.4% on 2019 numbers.

Earnings are now expected to be just $8 to $10 million. TRS shares fell 12%.

The US finishes higher, movement at the top, unemployment falls

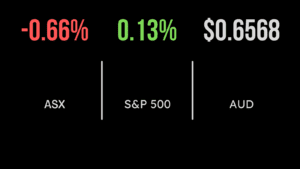

US markets finished broadly higher on Friday, with the Nasdaq leading the way to jump 1.4% whilst the S&P500 and Dow Jones added 0.9% and 0.5% respectively.

The biggest driver today and across the week was the performance of ‘big tech’, as the likes of Amazon, Alphabet, and Facebook benefitted from another fall in the US bond rate.

This came despite a fall in US unemployment to 5.8%. That said, only 559,000 jobs were gained in May, below the 650,000 expected.

Many analysts suggest this may be the ‘goldilocks’ scenario where the economy isn’t strong enough to boost inflation but is just weak enough to ensure support is maintained.

Alphabet Inc (NYSE: GOOGL) overtook Amazon (NYSE: AMZN) in the size race this week, moving beyond US$1.6 trillion in market cap but remains well behind Apple (NYSE: AAPL) at over US$2 trillion.

Across the week, it was the value-focused Dow Jones leading, up 0.7%, with the S&P500 and Nasdaq trailing at 0.6% and 0.5%.

Know what you own, follow the leader, headline data is not all it seems

The resurgence of the ‘meme stock’ rally once again brought focus on the growing use of passive investments around the world.

Unbeknownst to many, but both AMC Entertainment and GameStop, which have seen returns in the thousands of percent in a short period are actually among the largest holdings in the Russell 2000 small cap index.

Given the incredible volatility and clearly struggling business models, there is little doubt most investors would be seeking to avoid rather than hold them as their largest exposure. It always pays to look beyond the label.

This follows onto my second takeaway, which is that headline data and forecasts are not all they seem.

This week saw Australia among the world leaders as GDP increased 1.8%, yet expectations through 2020 were that our record-high savings rate would reduce, offering a perfect opportunity for Australian retail spending.

With the rate still at 11.6%, down from 12.2% last quarter, this hasn’t quite come to fruition.

Finally, after a week of presentations, and some paternity leave, there appears to be somewhat of a ‘follow the leader’ view in markets, with consensus building around everything from monetary policy to ‘transitory’ inflation and ESG.

I’m wary of anything where ‘experts’ agree and believe a more active approach than ever is warranted given the very unique conditions.