Sunday 3rd October 2021

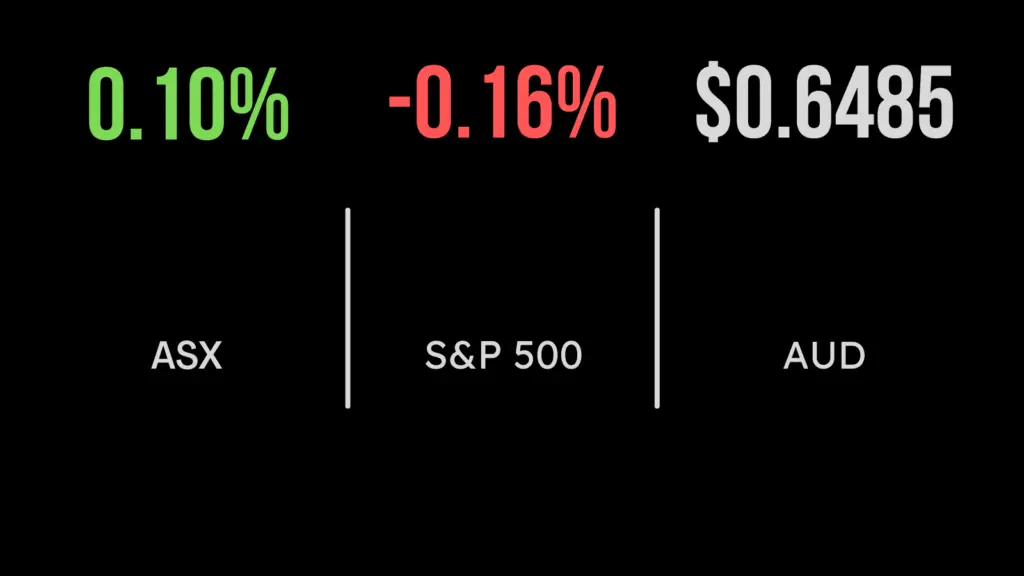

ASX drops 2 per cent as banks slide

Volatility returns, market drops 2.1%, banks lead sell off

The S&P/ASX200 (ASX: XJO) finished Friday and the week down 2.1%, after recovering most of the week’s losses on Thursday.

The selling pressure in the US flowed into the Australian session as investors remain fixated on the emerging threat to energy supplies along with the reduction in policy stimulus.

In Australia it was all about the banking sector today, selling off by 2.8%, the worst of all sectors. The weakness was driven by a 4.1% fall in Commonwealth Bank (ASX: CBA), and over 2% from ANZ, Westpac and the National Australia Bank (ASX: NAB).

Traders are clearly wary of the threat of APRA imposing borrowing limits in the coming months after residential property delivered a return of 20% over the last 12 months.

Materials also weakened another 1.8% even as the iron ore price gained 4.5% overnight, with Mineral Resources (ASX: MIN) among the hardest hit, falling 6.9%.

The positive news came from the travel and consumer sector, with Helloworld (ASX: HLO) jumping 5.4% after the Prime Minister announced that international travel will be allowed from November for the vaccinated, despite many being unable to travel within Australia.

Over the week it was the energy sector delivering the only gain, up 5% with Beach Petroleum (ASX: BPT) topping the table, up 19.8%. The tech sector was the weakest, falling 6.2%.

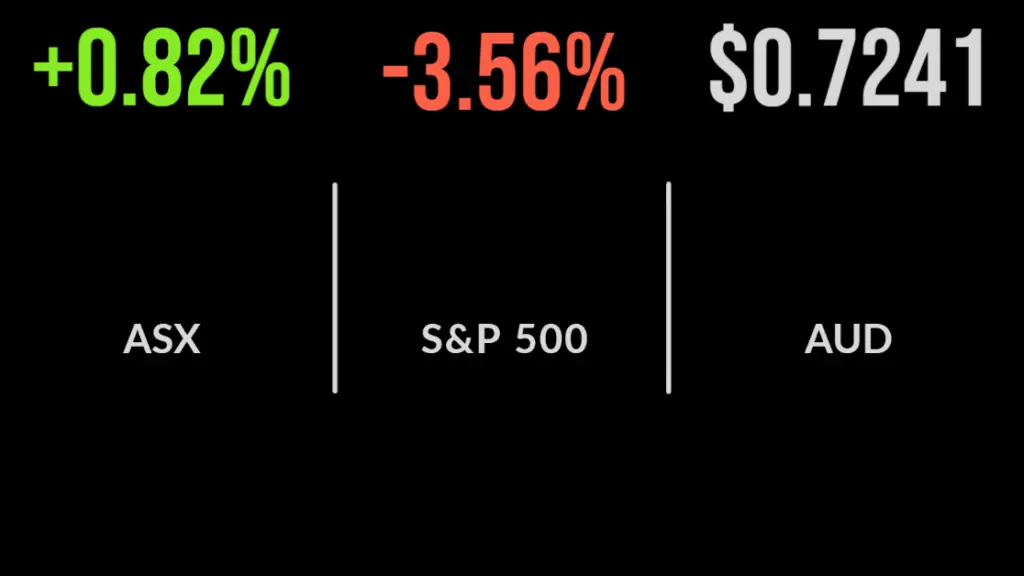

Strong Friday to send ASX higher, Merck’s COVID treatment, spending jumps

US markets overcame a turn in sentiment during the week to post another strong day, the Dow jones jumping 1.4%.

The biggest driver was drug company Merck (NYSE: MRK) announcing the results of trials of their COVID-19 treatment.

Rather than a vaccine the pill can be taken by those with the virus and was shown to reduce the risk of hospitalisation and severe illness by 50%, according to the company.

Shares rallied 8.4%, dragging the opening trade including smaller companies up another 1.7%. The S&P 500 also benefitted, adding 1.2% and the Nasdaq comparatively weaker at 0.8.

This wasn’t enough to overcome a volatile weak as traders send all three benchmarks down between 1 and 3%.

Shares in Visa (NYSE: V) jumped on hopes of higher spending, up 3.5%, with Walt Disney (NYSE: DIS) and American Express (NYSE: AXP) also following suit.

More positive news came from the US PMI which moved above 61 points showing the manufacturing sector is booming, whilst consumer spending jumped 0.8% in September. Consumers are clearly starting to grow in confidence.

Energy crisis, volatility returns, can rates really increase?

All eyes are on the Northern Hemisphere this week as energy is centre stage once again. The oil and gas sector has seen significant underinvestment in terms of both exploration and production for any number of reasons.

Whilst the future is clearly renewable, the shortages of energy that are spreading across Europe and Asia confirm there is a long way to go in the transition and it will likely be extremely bumpy.

Despite calls that fossil fuels were coming to an end; the global economy seems as reliance as ever.

October has traditionally seen the most volatility of any months, with most of the biggest crashes coming in the final quarter of the year.

Is it happening again? The month has seen a volatile start, with the threat of tapering, combined with inflationary conditions and what appears to be a tired bull market likely to see volatility here to stay.

As always, volatility offers opportunities for the patient. Economists around the world continue to predict interest rates to move higher ahead of the dates announced by central banks, but can it really happen?

It is becoming more and more evident, in my view at least, that we are facing real supply chain and supply side issues, something that rate hikes will likely exacerbate rather than solve.

If anything, we may be looking at a period of stagflation, being slowing growth and higher costs, rather than the positive inflation many are hoping for.

Perhaps this is why Australian Super feels comfortable enough to pay $1.9 billion, or a multiple of 38 times earnings, for 2,000 Optus telecommunication towers.