Nick Dignam from Fortitude Investment Partners shares insights with Lachlan Maddock from Fortitude Investment Partners on how a diversified portfolio in mid-market private equity is structured. The Inside Adviser

The world of alternative investments is at a crossroads. As markets defy expectations and liquidity concerns take centre stage, investors find themselves forced to rethink how they deploy capital in an increasingly complex environment.

‘No short-term phenomenon’: Why private capital will not only survive but thrive beyond 2025

The remarkable growth of private markets over the last decade has prompted some pundits to liken it to a bubble, fashioning it as some kind of overinflated hype-machine with vast tranches of capital placed in perilous investment vehicles peddled by inexperienced mavericks.

Yet the reality is far from the truth, with a report from consultants EY reinforcing just how embedded private capital has become in the financial services ecosystem, and how much growth potential remains in the sector.

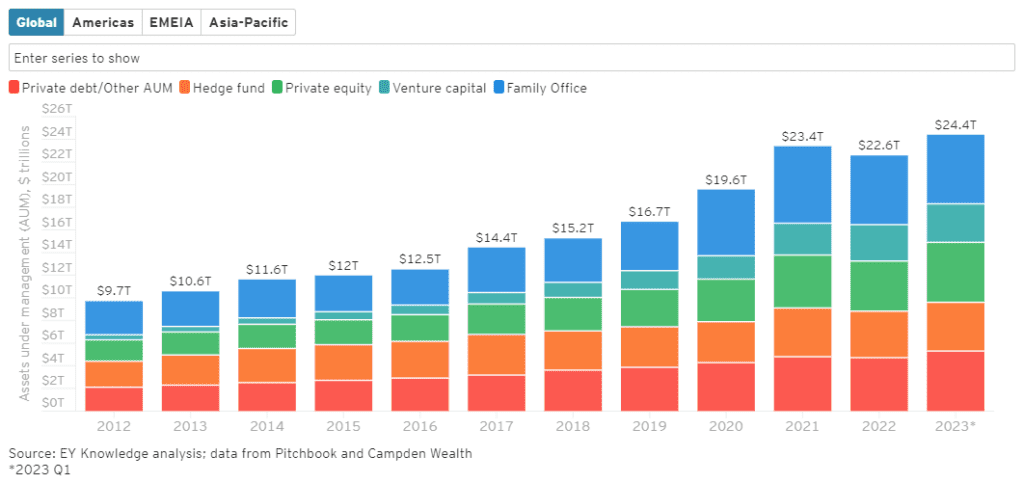

The private capital market has more than doubled in the last decade, from US$9.7 trillion in assets under management (AUM) in 2012 to an estimated $24.4 trillion AUM by the end of 2023.

Both private equity and private debt contributed $5.3 trillion each to the private capital arena in 2023.

Private equity and private debt (otherwise known as private credit) have fuelled this growth amidst a global trend towards delisting due to companies’ reluctance to face into the scrutiny of regular reporting, as well as a tighter lending conditions and the reluctance of banks to lend money through traditional means.

“For many larger private companies, the option of staying private has also become more appealing,” EY’s Are you harnessing the growth and resilience of private capital? report states. “This is partly due to the reassurance of higher regulation standards in private company governance models. However, conditions in the public market have also played a part. These include increasing costs, and the daily, quarterly and annual public market disclosure requirements, which discourage companies from going and staying public.”

The largest slice of the pie, however, came from the burgeoning family office sector, as wealthy family networks searched for alternative assets with a healthy risk/return profile. In 2023 there was $6.1 trillion in family office AUM across the globe, EY reports, with much of its growth driven by an increasing number of high-net-worth individuals, plus the largest transfer of intergenerational wealth in history taking place.

Somewhat surprisingly, given it has encountered intermittent lean years, venture capitalism has also been a significant contributor with the largest annual growth since 2012.

But while these factors have contributed to the rise of private capital, it is the very nature and the performance of the sector itself that EY believes will keep it perched at the top of the alternatives pile.

“The 10-year picture also reveals that the performance of private markets has been consistently stronger and less volatile than that of public markets, especially since 2016,” the report states, noting that while “slowing global economy, high inflation and increased uncertainty” in the wake of the pandemic pulled markets back significantly in 2022, private capital showed its resistance by only declining 3.5 per cent.

“Global equities, on the other hand, experienced a double-digit drop in value, with both developed and developing markets undergoing sell-offs. Even traditional go-to assets in troubled times, such as US Treasuries, suffered, while alternative assets like cryptocurrency fell sharply.”

The prognostication for the future of private markets looks strong, too, with several positive tailwinds including more companies indicating a preference to stay private for longer and a burgeoning pile of cash coming from increasingly capitalised pension/superannuation funds.

Not forgotten, either, should be the improved performance of fund managers who are becoming more agile an more experienced as the market matures and attracts talent.

“Private capital growth is no short-term phenomenon,” the report states. “The dynamics that drove expansion in the last decade are likely to persist, with a significant market size increase expected over the next few years and PE and family office predicted to take a sizeable share of these assets.”