Craig Brooke from KeyInvest speaks to James Dunn from The Inside Network for our IN60 videos. The Inside Adviser

David Chan from MLC shares insights with Laurence Parker-Brown from The Inside Network on how access to the larger pool of secondaries in PE helps diversification. The Inside Adviser

What goes up, must come down – depending on the time horizon.

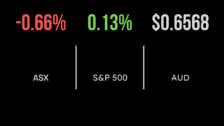

The S&P/ASX 200 fell by -1.3%, and the All Ordinaries declined by -1.2% as markets consolidated gains and absorbed news across borders of US treasury downgrades by Fitch. Interestingly all 11 sectors finished in the red (whilst the day earlier all sectors finished in the green) with the largest detractors being utilities, financials, and real estate. In line with the downbeat performance of the S&P/ASX 200, Asian markets didn’t fare better, as investors remain jittery, following the lack of “stimulus” through China. The Australian dollar also experienced a -1.5% decline overnight, trading at approximately US65.69c, following the Reserve Bank of Australia’s decision on Tuesday to keep interest rates unchanged for a second month in a row/along with US Treasury downgrades. As mentioned, the utilities sector recorded the weakest performance on the ASX, experiencing a notable drop of -2.2%. AGL Energy shares slumped by 4.8% to $11.69 after Macquarie downgraded the shares to neutral. This marked the most substantial decline since February. Additionally, Meridian Energy fell by -1.2% to $5.18, while APA Group lost 1.4% and traded at $9.80.

Real estate, materials, financials, and gold.

Real estate shares experienced a sell-off, with Goodman and Charter Hall down more than -2% to $20.17 and $10.96. BWP Trust, the landlord for Bunnings, saw its shares sink by -3.3% to $3.55 after reporting a 1% decline in full-year profit and writing down asset values across its retail portfolio. However, the major drag on the benchmark was the weakness in mining giants and the big four banks. BHP Group, accounting for over 10% of the index, lost -1.1% and traded at $45.85. Fortescue Metals slumped by -2% to $21.55, while Rio Tinto declined by -0.9% to $115.82. Copper experienced a -2.3% drop on the London Metal Exchange, and Tin declined by -3.2%. Additionally, iron ore prices traded lower in Singapore due to weak manufacturing data from China. In the financial sector, Commonwealth Bank declined by -2.3% to $103.46, National Australia Bank fell by -1.6% to $28.11, Westpac dropped by -2% to $29.98, and ANZ slid by -2.1% to $25.35. In other company news, Gold miner Westgold faced a significant decline of -8.8% to $1.56 after publishing its full-year production and cost guidance for 2024. Other gold miners also ended the day with losses, with Ramelius Resources down by -3.1% to $1.26. On a positive note, Incitec Pivot rose by +1% to $3.06 after announcing Indonesia’s Pupuk Kaltim as the preferred buyer for its fertilisers business, raising expectations of a deal worth about $1.5 billion.

US Treasury downgrades, Advanced Micro Devices, and Starbucks.

US indices took a hit as rating agency Fitch, downgraded the US government’s credit rating from AAA to AA+, citing “erosion of governance” and “expected fiscal deterioration”. Why is this important? Because the U.S. Treasury market serves as a worldwide standard, influencing numerous financial products, making investors anxious about the stability of the US market in light of downgrades. This downgrade had a flow-on effect, impacting global markets, and was an indirect but contributing factor to the weakness in the Australian dollar. In company news, Advanced Micro Devices posted second-quarter earnings that exceeded analysts’ expectations and provided revenue guidance for the third quarter of $5.7 billion, slightly below the consensus of $5.8 billion. The stock rose by +1% in premarket trading, boosted by the chip maker’s latest update on its artificial intelligence portfolio and positive predictions about the AI market. Whilst Starbucks reported fiscal third-quarter earnings that surpassed Wall Street estimates, but its sales fell short of expectations, leading to a -1.9% decline in premarket trading.