Consumer trust isn’t something to be taken for granted, but reports from the UK, US and here at home are all pointing towards an uplift in trust levels around financial advice, which can only be a welcome development.

There are significant tailwinds behind the financial advice industry at the moment, but some major obstacles are still preventing advice practices from taking advantage of surging demand according to a new study from CFS.

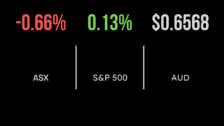

Market declines for second week with ASX down 0.8%

ASX flat despite iron ore falls, IRESS deal pulled, AMP’s new low

The S&P/ASX200 fell 0.8% on Friday erasing the week’s gains and ultimately leaving the index down three points for the week.

After being the hottest sector for most of the year, the materials and mining companies continue to drag the market lower.

On Friday it was all about iron ore with a 6% fall in the iron ore price overnight sending Fortescue (ASX: FMG) 11% lower and Rio Tinto (ASX: RIO) down close to 5%.

Iress (ASX: IRE) owner of the XPLAN system we use at Wattle Partners fell 11% after Swedish private equity firm EQT pulled out of their takeover bid, however, given the state of markets I wouldn’t be surprised if someone else comes up with a bid.

AMP (ASX: AMP) has reached a new low falling below $1 for the first time in its history as the recovery gets another step harder.

Cimic’s (ASX: CIM) shares fell 2% despite winning a $265 million contract for construction of the Western Sydney Airport.

The story was similar over the five days with materials falling 3.7%, the biggest detractor, and the more defensive healthcare and IT sectors up 1.7 and 2.2% respectively.

Altium (ASX: ALU) and Pilbara were the top performers over the five days with CSL (ASX: CSL) also gaining 2.5%.

Some older ‘blue chips’ are facing selling pressure with AGL (ASX: AGL) and Brambles (ASX: BXB) both down close to double figures on concerns for growth.

Lack of catalysts sends US lower, casinos, miners struggle, confidence boost

US markets struggled to another negative week, the first such fall with the Nasdaq and S&P 500 both down 0.9%. The Dow Jones outperformed by companies, falling 0.5% as the energy sector benefitted from a stronger oil price.

Friday marked the expiry day for options used to either leverage exposure to the market or protect portfolios, which typically sees greater levels of volatility. That said, 1% moves are far from volatile.

On Friday only healthcare was higher with the market seemingly struggling to find any positive catalysts after another strong year.

On the positive side, there are limited negative catalysts and a wall of cash is building up on the side-lines as the end of the year nears.

Over the week technology and energy outperformed, the latter gaining over 4% with consumer cyclicals benefitted from a recovery in consumer confidence and a higher-than-expected retail sales result.

The crackdown in Macau pushed the casino sector lower whilst Evergrande’s issues are putting a cap on commodity prices for the time being.

Stay at home business outperformed on Friday, with Zoom (NASDAQ:ZM) and Netflix (NYSE: NFLX) rare gainers amid the worsening Delta outbreak.

Money on the sidelines, death of forecasting, reinvesting in yourself

My first takeaway leans on the comments of ‘Coppo’ the well-known stockbroker in investment circles.

In his daily newsletter he highlighted that as much as $84 billion could be looking for a home on the ASX in the next six months.

The combination of takeovers, buybacks and special dividends suggests investors will be flush with cash.

One of the less appreciated events in markets is the fact that the institutional investors who own a company being taken over are ultimately forced to reinvest that capital into the equity market, which should see some support if the market continues to weaken.

This week’s unemployment rate continues to evidence the great divide between the real world and the financial statistics.

It is abundantly clear to those in the ‘real economy’ that there is significant pain, yet economic statistics continue to show incredibly low unemployment rates and a strong economy.

There remains a consensus among ‘experts’ that spending will snap back quickly after lockdowns, but I wouldn’t be so sure.

Bramble’s (ASX: BXB) double digit fall this week once again highlights the issue of short-term management and a focus on dividends.

The CEO who had been in place for five years admitted to focusing too much on short-term performance targets, leading to higher dividends and buybacks, and not reinvesting in the company. A lesson for many Australian businesses.