Tuesday 9th March 2021

Will 2021 be the year for infrastructure?

Let’s get real

The financial chatter box is overflowing on bond movements and the potential impact on valuation of risk assets. Inevitably the long-duration equities are front of mind. Most are focused on the FAGAM (Facebook, Amazon, Google, Apple, Microsoft) or other similar stocks where the valuation is considered to reflect long-term thematic growth.

On the other side are the lower profile sectors such as REITs and infrastructure. At one level these two sectors are linked by their increasingly unusual nature – a balance sheet of fixed assets, nowadays absent in many service-based companies. Otherwise, there are clear differences.

REITs are skewed towards household behaviour via participation in retail, attendance in offices, housing rental and bits of communications. Some of infrastructure is similar, but dials down the household weight towards inputs such as utilities and rail. Infrastructure can have a regulatory framework, but also often has monopoly characteristics or high barriers to entry. A shopping centre or office building can be replicated within eyesight whereas a railroad, airport or toll road rarely is.

Intuitively, many of the assets in infrastructure have better long-term characteristics than REITs, though both have stranded assets where changes in usage is likely to undermine their viability. In REITs the office landscape is expected to experience a step-change post COVID, whereas the demise of fossil fuel energy assets seems certain.

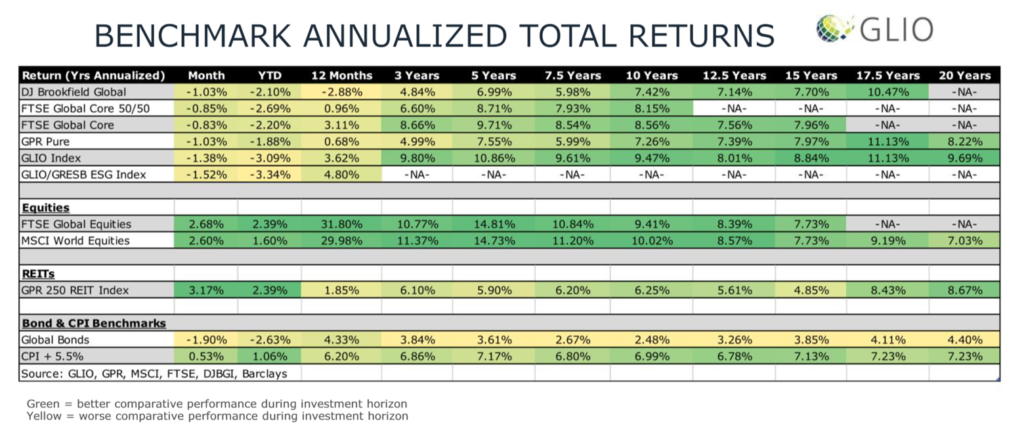

Australian investors have a decent breadth of choice in listed global equity infrastructure managers with most offering hedged and unhedged options. The first hurdle in judging performance is the benchmark. DJ Brookfield, S&P, FTSE and GLIO all have varying definitions of what constitutes infrastructure and how it is weighted in their respective indices. Some funds chose to report against a CPI+ benchmark, a great idea when markets were rallying, not much fun today.

A quick peruse of the US$-based data in the table shows that infrastructure has underperformed global equities, but in large part due to the drag from the past year. REITs’ longer-term returns are behind equities by a wider margin. Long-term volatility favours infrastructure, some 3% below that of global equities, while REITs’ volatility has been higher than both.

The discount rate did little to alleviate concerns on economic activity that is embedded in infrastructure, obviously on those most affected such as airports, while even relatively stable-cash-flow utility stocks had sluggish share price performance over the past year.

There is a case that infrastructure investment could be the sleeping performer in the coming year. Rising rates and inflation does not herald a poor outcome given that the sector has not been a rate beneficiary in the past 12 months. A return to travel later in the year would be a notable positive outcome, while a pickup in the industrial sector is broadly represented across the sector. Then there is a consistent pattern of M&A with listed assets often priced below their unlisted comparison. Last, but not least, is the long-awaited infrastructure building boom, especially in the US. Well-capitalised companies could be the natural owner of new assets.

The quality of the assets in the sector is essentially the same as it was in 2019, yet equity pricing is still well below. For those looking to diversify from momentum-based growth companies, listed infrastructure may be better alternative than a simple switch into value.

Giselle Roux is one of Australia's most well-known and highly regarded investment strategists, having held the role of chief investment officer at Escala Partners and JB Were.