Thursday 28th April 2022

Will the your future four super test be applied to SMSFs?

In 2021 the “Your Future Your Super” (YFYS) performance test was introduced to gauge whether default super funds, which collected billions in guaranteed contributions, were up-to-scratch in terms of their investment performance.

Speaking at the SMSF Association’s National Conference 2022, Philip La Greca, executive manager of SMSF Technical & Strategic Solutions at Super Concepts, who discussed in detail why this measure was introduced and why it should matter to advisers.

La Greca gave a first-hand account of when nearly one million people were informed that their existing super fund was not up-to-scratch following the first YFYS performance test. “Firstly, why is there the Your Future Your Super?” he says. “It really came down to the 2018 productivity commission report on superannuation which assessed efficiency and competitiveness. It also examined the efficiency of the superannuation system, particularly default and MySuper funds.”

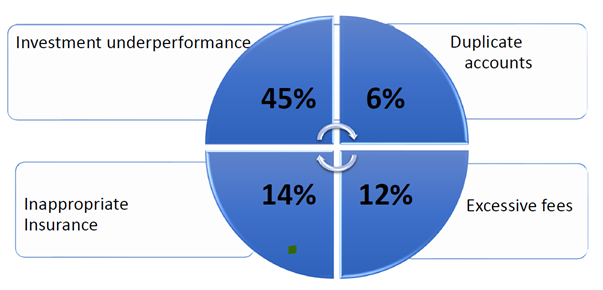

While MySuper funds were put under the spotlight, the ramifications for all superannuation funds including SMSFs are critically important. The government agenda was to address four target areas: excessive fees, duplicate accounts, inappropriate insurance, and investment underperformance. Of the detriment to clients, 45 percent was due to investment underperformance. It was found to be the main contributor to poor retirement savings, followed by inappropriate insurance. The end result; more people are drawing on the old-age pension.

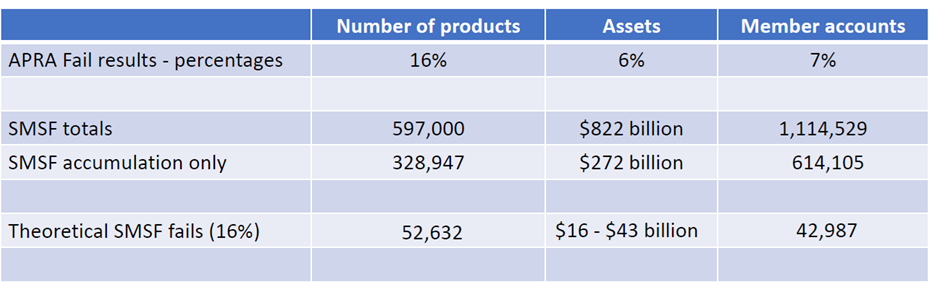

Every APRA fund sends net investment, fee data and asset allocation data to the regulator on a quarterly basis. Using this data, the YFYS performance test compares the actual investment performance, minus costs, versus the benchmark performance based on strategic asset allocation. The results showed that only 84 per cent of $900 billion in APRA-regulated funds passed the test. There were 13 funds that failed the test. This underperformance affected one million super fund members out of 14 million.

The government firstly tackled excessive fees in MySuper and default funds. SMSF fees were left as is, for now at least. The primary objectives proposed was to provide income in retirement, to substitute or supplement the age pension.

Underperformance saw APRA-regulated funds given a red card. “Funds that failed the test were forced to write to their members advising of the underperformance, and what they were going to do to fix the underperformance. Ones that failed the test two years in a row, as an APRA fund, could no longer accept new members,” says Le Greca.

The big question remains, what about SMSFs?

“Is it possible to put them through a similar sort of test? Potentially yes, but only for a subclass of SMSFs. The big problem is the data. From an SMSF viewpoint, no data is provided to the regulator. The data collected by the ATO is tax data and not investment data,” says La Greca. “With the YFYS performance test, software providers were the ones that provided the data.”

For advisers, the underperformance of a client’s SMSF becomes a real problem: it could fail the best interest duty. The super fund performance test has the potential to become a real part of the financial advice process, with advisers needing to consider the implications of repeated failure by the fund to meet the test’s annual benchmarks.

Similarly, advisers recommending an underperforming My Super product that fail to alert the regulator of a fund’s performance test failure to a client could also come into breach of the best-interests duty. At same fail rate of 16 per cent, about 53,000 SMSFs funds are underperforming in the sector. That adds up to almost 43,000 SMSF members being affected by underperformance.

According to La Greca, the way forward is to collect real investment data from SMSFs. There needs to be uniformity of classification, so asset allocation categories are the same across the board and to accrue a history of performance data.

This means the SMSF sector needs to understand the YFYS performance test measures and how to make comparable measures for SMSFs that will align with both the trustee outcomes from a measurable and comparable investment strategy and financial advisers’ obligation for clients’ best interest.

With the SMSF sector being larger than the MySuper sector, and proposals to extend the performance test to “Choice” funds, the possibility of something similar applying to SMSFs cannot be ruled out.

It’s more a question of “when,” not “if.”

Ishan is an experienced journalist covering The Insider Adviser publication.