Thursday 5th May 2022

Some market neutral funds don't live up to promises

Amid ongoing elevated volatility, some financial advisers are recommending that investors hold alternative investments, including market neutral funds, which could help cushion portfolios against a broad market sell-off.

Amid ongoing elevated volatility, some financial advisers are recommending that investors hold alternative investments, including market neutral funds, which could help cushion portfolios against a broad market sell-off. However, research by Morningstar finds that market neutral funds have large factor tilts and do not always live up to their promise of guarding against equity market losses.

According to Simon Scott, director of alternative ratings at Morningstar, it is common for many alternatives portfolio managers to attempt to construct portfolios labelled as ‘market neutral’, but some US funds have exposed investors to large losses in recent years, his analysis reveals.

“These managers eschew directional trading and so aim to provide a more stable return profile, reducing the large infrequent negative events incurred by directional investors. The process is simple—buying one stock and short-selling another closely related one, reducing the equity market sensitivity, or beta, to zero.

“The portfolio should then only move according to factors specific to those individual stocks. In this way, success is dependent on strong alpha prediction skills as we let go of the helping hand of the market,” says Scott. “Investors need to ensure they are not switching one risk for another and taking on large style exposures.”

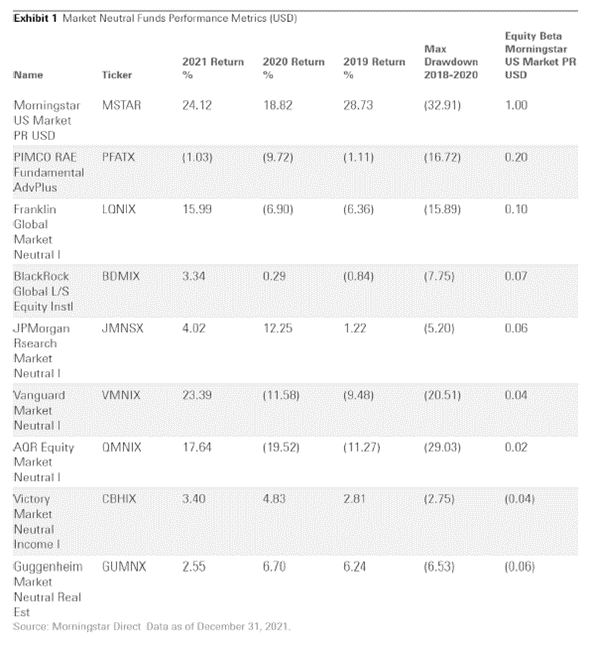

However, Scott concludes that contrary to expectations, “market-neutral funds are a varied bunch. As Exhibit 1 shows, there is significant performance dispersion in our US fund equity market neutral Morningstar category despite the cohort maintaining next to no sensitivity to broad equity markets.”

“Investors are right to question how Vanguard Market Neutral I fund in the US, which has a Morningstar analyst rating of ‘neutral’, can return 23.29 per cent in 2021, just shy of the Morningstar Market PR Index return of 24.12 per cent, while maintaining a beta of only 0.04.

“In a similar vein, neutral-rated AQR Market Neutral I suffered a 19.52 per cent US dollar loss in 2020, a year when broad equities rose just under per cent.”

Morningstar does not maintain a dedicated equity market neutral category in Australia due to not enough funds existing, therefore, any averages would be too volatile and skewed by outliers to be much use, Scott explains.

Market neutral includes several different strategies. At the most basic level are dollar-neutral strategies. These match the long side and short side of related stocks in notional terms—for example, being long US$10,000 on Microsoft and short US$10,000 on Apple. However, this approach does not consider the relationship or the volatility of the individual stocks. The investor can end up being either positively or negatively correlated to the market. Each day, the balances change, and the positions require rehedging to give equal dollar exposures, says Scott.

“To avoid this, market-neutral managers instead choose to weight each individual stock against each other based on their relative betas to the index. As it is rare to find two related stocks with the same beta at the same point in time, an adjustment is required,” he says.

Financial adviser Scott Keely doesn’t use market neutral funds or recommend them. He says they are too complex and expensive for clients. “A combination of the difficulty of explaining them to clients, as well as the strategy of essentially betting against yourself and your own stock picking ability that these fund managers use doesn’t really arm me with confidence,” says Keeley.

Nicki is an experienced journalist writing across three publications.