Thursday 16th December 2021

Performance dispersion expands amid growth sell off

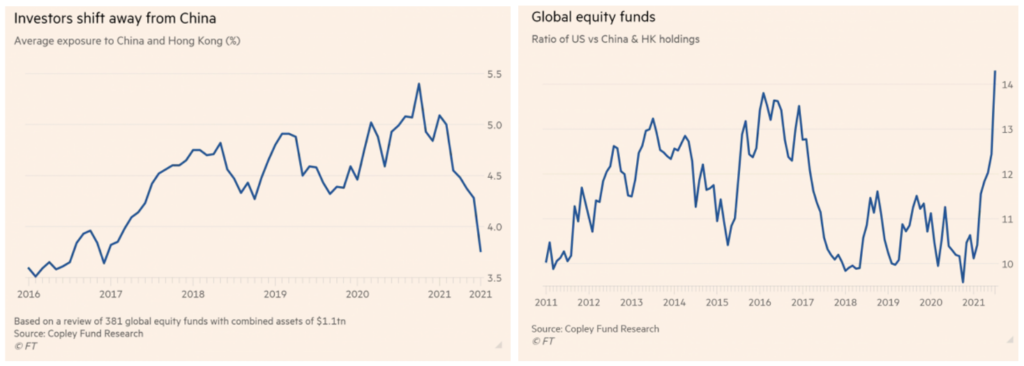

The second half of 2021 has produced a mixed bag of results for global growth equity funds. A mass rotation away from China and high bond rates impacting valuations saw global growth funds skewed towards Asia and US tech, underperform. Those tilted towards the US more generally outperformed.

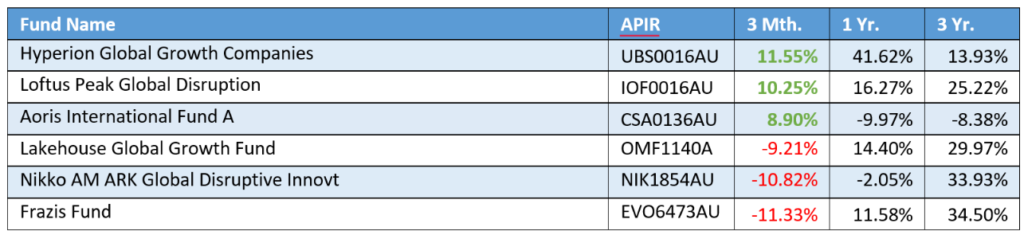

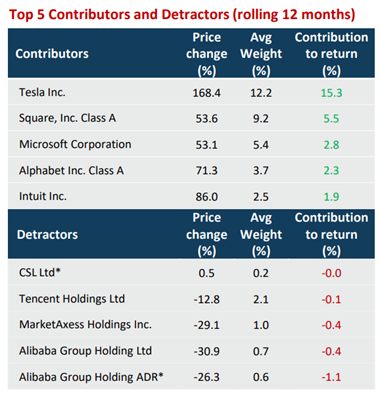

Looking at the Hyperion Global Growth Fund, 67.1% of the fund is weighted to the US, while only 20.7% is in Asia Pacific. Looking at the Top 5 contributors and detractors for the Hyperion Global Growth fund, being skewed to the US stocks has paid off. The fund returning 11.55% for the September quarter.

On the flip side, the Lakehouse Global Growth Fund contracted by -9.21% according to publicly available data. In the monthly commentary the team said, “the Fund isn’t as US-heavy as it might look at first blush, though, with 59% of the revenue from the Fund’s portfolio companies coming from outside the US and holdings headquartered in the UK, Netherlands, Canada, Argentina, France, China, Japan, and Norway.”

Nikko Asset Management’s ARK Global Disruptive Innovation fund tumbled by -10.82% and the Frazis Fund recorded the largest decline of -11.33% for the quarter. ARK Invest has been well known for its willingness to back hypergrowth companies, whilst Frazis is a relative newcomer who delivered strong returns amid the pandemic.

During the quarter global markets tumbled giving back the solid gains achieved in the first two months of the quarter. Despite September quarter’s losses, global equities resumed their upward trajectory in October and still in positive territory year to date. Investors are seeing the September quarter rout as a opportunity rather than change in trend. The global market pause needed to happen as markets have been running hot since the lows of March 2020. The sell-off came on the back of a number of negative media headlines which prompted investors to lock in profits. Here are some of the reasons:

- The S&P 500 had its worst monthly performance since March 2020.

- A shift to renewable energy has caused an energy crunch sending oil, gas and coal prices higher as well as inflation. Thing is that renewables haven’t been able to pick up the slack.

- Inflation fears are a major concern for investors with Fed chair Jerome Powell saying inflation isn’t transitory as the supply chain is in crisis.

- Rhetoric by the US Federal Reserve suggesting an earlier than expected tapering in bond purchases and an increase in interest rates in late 2022.

- Economic data was soft. China’s services PMI has fallen below 50 (services sector is contracting), plagued by rising costs, supply/production bottlenecks and electricity rationing.

- Fears of a possible debt default by Chinese property developer Evergrande Group

- New regulations on Chinese technology companies habve resulted in a tech sell-off.

Developed economies have begun tapering their bond purchase programs. Bond yields rose while share markets fell. Raw material and metals prices rose, as well as semiconductor prices, which placed immense pressure on profit margins for manufacturers.

In the S&P 500 Index – Financials and utilities performed well while industrials, business services and materials recorded the biggest losses. MSCI China Index of US-listed stocks was down 18% – Beijing unleashed a regulatory offensive against major tech firms to ensure “social stability” and national security. It’s always a concern when the Chinese Communist Party unleash a torrent of new rules and regulations. Investors do not like uncertainty and will move to calmer waters. It spreads throughout the market and negatively impacts a variety of sectors.

In this case the sectors affected are: Internet platforms, private education, online gaming, video streaming, food delivery, ride sharing, pharmaceuticals, and alcohol producers.

Ishan is an experienced journalist covering The Insider Adviser publication.