Friday 13th November 2020

Beyond the horizon - listed infrastructure in a mid-pandemic economy

2020 will go down as a wild ride in the markets for a multitude of reasons. Heightened volatility and drawdown events have put capital preservation, absolute return, and downside management back in focus. Global infrastructure & utility stocks have been front and centre of that volatility – and a new product to launch next month in the local market aims to focus on exactly these attributes.

Global listed infrastructure (GLI) and utility stocks have traditionally been seen as defensive safe-haven assets – particularly in times of market stress. This has been due to their underlying asset characteristics – long-term and predictable cashflows, monopolistic assets and inflation-linked revenue streams. However, according to Tim Snelgrove, portfolio manager of the Horizon Fund, a global listed infrastructure long-short strategy, relying purely on the underlying asset cashflow profile for protection isn’t enough.

“Relying on these underlying attributes alone when you are in a fully invested long-only strategy can only protect you so much,” Snelgrove notes. This is because in periods of market-wide shocks and selloffs, often beta and correlation go to one – regardless of the underlying asset characteristics. This was evident in the COVID-19 induced sell-off in March, in which share prices of regulated utilities in the US, which had highly regulated, stable earnings growth over the next five years of 5%-7%, dropped between 25% and 50%. Before COVID-19, there were similar drawdown events such as the “Taper Tantrum” of 2013, the “Trump Bump” of 2016 and the “Fed pivot” of 2018. These surprises are not limited to macro events, with a host of other risks often impacting the sector across various regions and sectors, such as regulatory and political intervention. “The UK Labour Party pledge to nationalise the water industry if it won the 2019 election saw share prices trade at multiples not seen since the credit crisis,” Snelgrove notes.

Traditional GLI funds rely on sector and region diversification to manage risk. “The only real tool at the manager’s disposal to portray a negative view is to increase cash, which for most funds rarely averages above 5%-10%. We think there are other ways to protect the portfolio against drawdowns, and thus, compound returns. At the end of the day, drawdowns kill compounding returns,” Snelgrove adds. The long-short approach to GLI means the fund can take an active view to risk management, by managing net and gross exposure actively. The Horizon Fund that Snelgrove manages at Coaster Capital targets net market exposure of 20%-40%.

The strategy also approaches portfolio construction uniquely. Similar to traditional GLI funds is its appreciation of both the fundamental bottom-up stock drivers as well as the impact of top-down macro drivers on the space, but Snelgrove says Horizon doesn’t build a portfolio based purely on value and what’s cheap. “The fund builds a portfolio across three buckets of return; thematic trades, opportunistic trades and pair trades. Each trade we put in the portfolio is there for a reason. There is a trade thesis, return target and catalyst why we think it should get to our target return or spread. This allows us to track its progress, and makes us agnostic to trade time frame,” Snelgrove adds.

Core to the investment philosophy is the belief that trade time-frames and turnover are an output of the trade rationale – not an input, which can often limit opportunities. “I view active long-only managers being in two rather opposite camps when it comes to trade time-frames and turnover. Active managers with ten per cent turnover and low tracking error to their benchmark are vulnerable to low-fee passive ETFs. On the other hand, managers with turnover over 40% have difficulty reconciling their argument that they invest on a five-year time-frame.”

A long-short approach to GLI, such as the Horizon Fund, doesn’t only benefit from the ability to manage net exposure to the market and drawdown risk. “The extra tools available to us, such as short-selling and using exchange-traded options (ETOs) to express trade ideas, opens up a whole new set of potential opportunities for generating alpha,” Snelgrove explains. For example, this includes the ability to exploit the relative value between two stocks without taking any directional market risk. Pair trades allow the manager to explicitly make a call that one stock is trading at a premium to another, and that that gap will narrow. Even if both stocks go down, the manager can generate a positive return if the call is correct and that premium closes. “In a long-only fund, if you hold both names and that gap closes, you still lose money if both stocks go down,” Snelgrove adds. North American utilities in particular is a vast opportunity set for the new strategy, with the ability to make calls between those states that have strong regulation versus those that are more politically influenced, as well as those states rewarding renewable energy capex plans versus those companies that are in renewable-unfriendly jurisdictions.

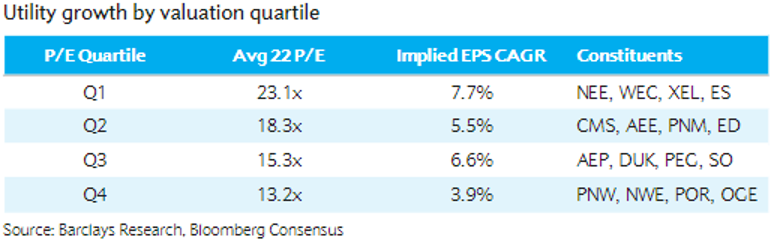

“The PE spread between the upper and lower quartile is now 50%, even though there is less than 5% differential in EPS growth between the two”.

“At Horizon, all we do is invest in infrastructure and utilities across the globe. But that shouldn’t mean we have to restrict ourselves – we should utilise all the tools we can, both to manage risk and expand opportunities for generating alpha, to achieve the ultimate goal for our clients, which is compounding, positive absolute returns,” Snelgrove says.

As second and third waves hit parts of the US and Europe, it is hard to see a straight line out for the markets – especially those infrastructure stocks, such as toll roads and airports, that are in the eye of the storm. But for Snelgrove, and the Horizon Fund, the best way to navigate the sector, at this time or any, is with the most tools available.