Monday 19th October 2020

Yarra Capital's view on corporate hybrids

Return of the A$ Corporate Hybrid Market

Many of us who are old enough will remember the once-thriving ASX-listed corporate hybrid market as a constant feature of the pre-GFC Australian credit landscape, with the innovatively named Multiplex SITES, Fairfax PRESSES and Dexus RENTS securities (among others) offering returns and features to meet the risk appetites of many credit investors.

Post-GFC, the souring of Australian investor sentiment towards corporate hybrids and reduced capital needs from issuers generally have gradually seen most corporate hybrids redeemed, leaving bank and insurance names as the hybrid mainstays, particularly on the ASX.

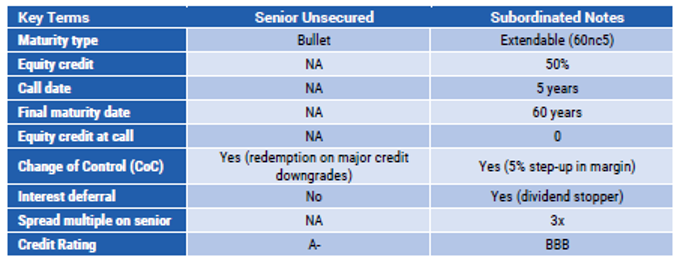

Fast-forwarding to 2020, and if we are marking the return of the corporate hybrid market in ‘Star Wars’ terms, the recent issue of the A$ AusNet Services (AST) 60-year non-call five-year (60nc5) corporate hybrid would best be described as The New Hope. Oversubscribed, the $650 million deal was issued in the over-the-counter (OTC) market at an attractive credit margin of +310 basis points (bps), roughly 3 times the comparable senior bond credit margin.

So why are investors being paid three times the credit margin of AST’s senior bonds, and does this corporate hybrid represent attractive risk adjusted returns?

Overall, the margin is much higher to compensate investors for the inclusion of some equity-like features, such as the ability to extend maturity well beyond the call date and to defer coupons, which enables half of the $650 million to count as equity in credit rating calculations from S&P.

While these features provide AST management with flexibility and reduce the amount of equity capital required to fund the company’s capital requirements, the 60nc5 subordinated note, in our view, remains ostensibly a fixed income security, underpinned by low credit risk and with little likelihood of coupons being deferred or the notes not being called at ithe 2025 call date.

Our confidence in this regard is based on:

- Strong dependable cash flow generated from AST’s regulated utility businesses across Australian electricity and gas transmission markets, underpinning investment-grade credit quality;

- A commitment to maintain shareholder distributions, reducing the likelihood of coupon deferral given any payments to shareholders would be prohibited if coupons to noteholders were deferred; and

- Loss of equity credit from major rating agencies if these securities are not called in 2025, which would render them uneconomic from a weighted average cost of capital (WACC) perspective.

Given the high degree of confidence on credit quality, the likelihood of coupons being paid and the call being exercised, the new AST subordinated note at a credit margin of +310bps (or three times that of the senior bonds) offers compelling risk adjusted returns in the current environment.

We’ve added the AST 60nc5 subordinated notes across all our dedicated Australian credit portfolios, with this security contributing to very attractive investment-grade portfolio yields of 3.5%-4.0%. We hope other Australian issuers will follow in AST’s wake, adding further diversification to the pool of available opportunities for Australian credit investors.

Written by Phil Strano, Yarra Capital Management.

Disclaimer

To the extent that this document discusses general market activity, industry or sector trends, or other broad based economic or political conditions, it should be construed as general advice only. To the extent it includes references to specific securities, those references do not constitute a recommendation to buy, sell or hold such security. Yarra Funds Management Limited (ABN 63 005 885 567, AFSL 230 251) believes that the information contained in this document is correct and that any estimates, opinions, conclusions or recommendations contained in this document are reasonably held or made as at the time of publication.

Phil Strano has had a distinguished career in the Australian fixed-income market. He is head of Australian credit research and portfolio manager at Yarra Capital Management.