Thursday 19th August 2021

Netwealth invests in tech to reassert dominance

Netwealth (ASX: NWL) – The leading platform provider delivered a FY21 net profit of $54.1 million, which was up 24 per cent, but below the analysts’ consensus forecast, of $55 million. Shares in the stock dropped by 4.8 per cent, to $14.24, but were down as much as 10 per cent during the day, as the company told shareholders it expected to spend more.

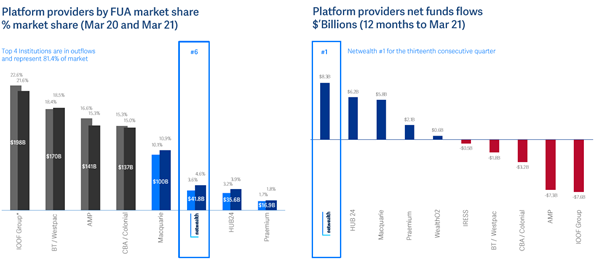

The all-important figure by which platforms rank themselves is funds under administration, or FUA. Netwealth said its FUA rose by 49.6 per cent over the year, to $47.1 billion, and it expects it to grow by $10 billion in the current financial year. Total revenue increased by 17 per cent, to $144.9 million. Platform revenue was up 17 per cent, to $142 million. The board declared a 9.5c dividend taking the total dividend to 18.56 cents, up 26.3%.

Netwealth saw its managed accounts business boosted by 70 per cent during the financial year, with $9.8 billion funds under management (FUM), while the average wrap account was over $1 million. The average account size had increased to $481,000, which was $1,082,000 for wrap and $240,000 for superannuation accounts.

The platform is well-regarded by advisors and ranked number 1 for overall satisfaction among primary users for the tenth year in a row, according to Research Trends.

Whilst Netwealth is still a small player when compared to the big bank platforms, net funds are flowing consistently out of the big bank-owned platforms such as IOOF and AMP, and into Netwealth. The FUA growth is driven by continued migration of accounts from existing financial intermediaries and new financial intermediaries.

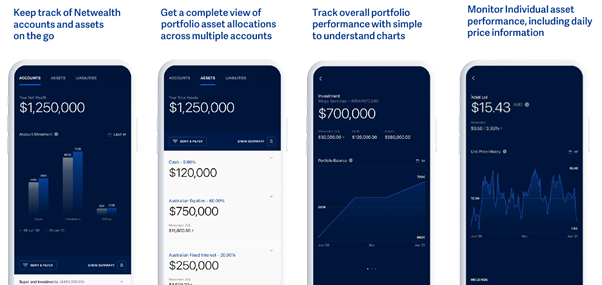

Netwealth also introduced its enhanced client experience smartphone app called Xwrap.

Netwealth’s growing tech platform saw it increase its headcount by 63 during the year, to 402 including an additional 43 in the technology team.

So why did the shares fall?

Firstly, the headline NPAT figure was below expectations, and the platform provider did flag higher-than-expected costs looking out into the future. But to add to the growing headwinds, platform providers generate a spread between the interest paid to customers received from the banks, and this is subject to interest rates.

A significant portion of their income comes from cash margins. With interest rates falling to near-zero levels with no prospect of rising anytime soon, the platform has seen its main revenue source dry-up. According to the Australian Financial Review, Netwealth did send interest rates paid to investors to zero (March 4) following the Reserve Bank’s historic cut to the official rate. Thousands of clients using Netwealth were left earning no return on their cash accounts, despite paying minimum fees.

So, suffice to say, some of the share price fall has come from investors seeing the platform provider’s profits coming under pressure with falling margins due to the spread charged on interest earned. However, according to the RBA, longer-term rates are projected to trend around 0.10 per cent in 2022 and 0.25 per cent in 2023. That should see cash margins back on the mend. Looking forward, Netwealth has an enviable track record and has consistently been rated as the number 1 platform provider.

On the other hand, the much -aunted release and migration of BT Panorama, which has seen multiple outages and stumbles thus far, has seen a compression in platform fees. Netwealth’s latest report showed that it had begun reducing platform fees for existing customers to match those of the new advisers joining the platform.

Morgans has released its post-result report on the stock, with a ‘hold’ recommendation and a target price of $16.20. The broker says underlying profit growth of 23.5% was slightly below its expectations, due to a lower second-half revenue margin. Morgans sees upside emerging with the improvement of the platform’s operating infrastructure allowing scale efficiencies.

As we saw with the Powerwrap and Praemium merger, the platform world is in a state of flux and transition. Many of the big bank platforms are facing heavy fund outflows and declining financial adviser numbers. While the changing landscape will provide Netwealth with new opportunities, it also provides shareholders with upside potential from a M&A consolidation tilt by any of the bigger players.

Ishan is an experienced journalist covering The Insider Adviser publication.