Friday 22nd July 2022

Fixed mortgages cliff coming, economy could slow

As fixed mortgages expire in Australia, households will be hit by higher interest costs on variable mortgages which will threaten consumer spending and economic growth, according to new research.

As fixed mortgages expire in Australia, households will be hit by higher interest costs on variable mortgages which will threaten consumer spending and economic growth, according to new research from AMP Investments.

A large number of home loans in Australia were fixed at ultra-low interest rates during the pandemic. Many of these will roll-onto variable mortgages in 2023 at much higher interest rates, which presents a significant downside risk for consumer spending and economic growth, according to Diana Mousina, senior economist with AMP.

She notes a significant shift to fixed-rate home loans in 2020 and 2021 when the Reserve Bank of Australia (RBA) introduced a term funding facility in 2020 to provide low-cost three-year funding to banks, and also introduced a 0.1 per cent three-year bond yield target. This encouraged banks to lower fixed rates on mortgages, with the three-year fixed rate bottoming at 2.1 per cent in mid-2021. While fixed lending typically accounts for 10 to 15 per cent of total outstanding lending, this lifted to over 40 per cent in 2021, as the chart below shows.

According to separate RBA data, the average interest rate on fixed-rate loans of three years or less duration fell to a low of 1.95 per cent in May 2021. That rate had jumped to 3.31 per cent as at May 2022. In contrast, variable interest rates on home loans fell to 2.76 per cent in May 2021, but had risen to 2.63 per cent as at May 2022, less than the rise in average fixed rates.

Now, analysts expect variable to keep on rising faster than fixed rates, in line with official interest rate increases expected later this year and in 2023.

“With the employment market continuing to tighten markedly, and no signs of inflation easing, the RBA is likely to raise interest rates by 50 basis points at its August meeting, with several increases potentially following after that depending on how the economy reacts to the mega rate rises of June and July,” said Russel Chesler, head of investments and capital markets at VanEck.

Consumer spending to drop as fixed terms expire

Analysis by the Commonwealth Bank of its mortgage book suggests that many of its fixed loans will expire in the second half of 2023 and roll-onto variable mortgages, with interest rates that could be two to three times higher than borrowers’ current fixed rates. As this happens, Mousina expects a drop in consumer spending.

“The households impacted make up around 30 per cent of the total housing loan stock according to bank data, which is a significant downside risk for consumer spending. We see consumer spending growth declining to just over 1 per cent per annum in late 2023, well down from 4 per cent over the year to March 2022.”

According to Mousina, some potential offsets to a drop in spending include the accumulated savings of households, with research from the central bank suggesting 75 per cent of variable mortgages are more than three months ahead on repayments, which reduces the risk of missed payments/bad loans in the short-term and rising wages growth.

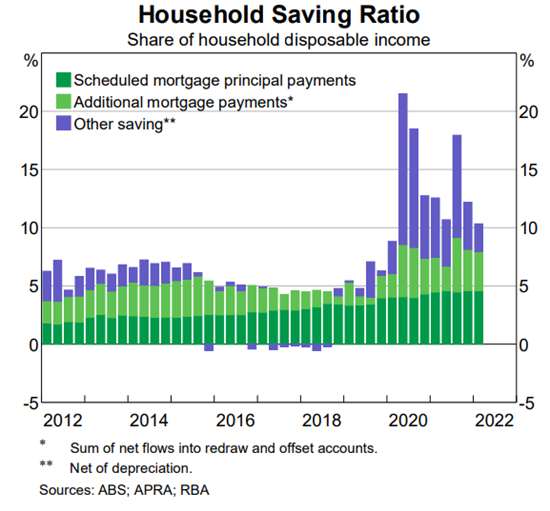

RBA deputy governor Michele Bullock also said this week that since the start of the pandemic, payments into offset and redraw accounts have been substantial, totalling around 3½ per cent of household disposable income (see the graph below). “The accumulated stock of these savings could help to ease the transition to higher mortgage payments for many borrowers, allowing them to sustain higher levels of consumption than otherwise,” she said.

Nevertheless, according to Bullock, some households are more likely to face financial stress than others. Highly indebted households are especially vulnerable in the event of a loss of real income through higher inflation, particularly if combined with rising interest rates, and a decrease in housing prices.

“Recent borrowers are more vulnerable than earlier cohorts, as they are more likely to have borrowed at high debt-to-income ratios, have had their serviceability assessed at lower interest rates (albeit with larger interest rate buffers) and have had less time to accumulate equity and liquidity buffers,” she said.

Nicki is an experienced journalist writing across three publications.