Monday 4th July 2022

What will another rate hike mean for markets?

This week marks the start of a fresh new year. 'Out with the old, and in with the new' is the old adage. Unfortunately, it's not so straightforward with the Reserve Bank of Australia.

This week marks the start of a fresh new year. ‘Out with the old, and in with the new’ is the old adage. Unfortunately, it’s not so straightforward with the Reserve Bank of Australia (RBA). Inflation remains stubborn, hovering around the 5.1 per cent mark, but there are fears are that it could very quickly balloon to 7 per cent. In its last commentary, the RBA said: “Headline inflation is forecast to peak around 6 per cent in the second half of this year. Underlying inflation has also risen strongly and is forecast to increase further to 4.75 per cent in the second half of 2022, largely reflecting further pass-through of upstream cost pressures.”

In Australia today, the RBA board meets again for its Statement on Monetary Policy. With last month’s surprise 50-basis-points rate hike taking the cash rate to 0.85 per cent, markets are bracing for another 50bps rise, taking the cash rate to 1.35 percent. This would make it the third consecutive rise in as many months. One thing is for certain, the RBA has said that a 75bps rate rise is not on the table this time around; unlike the US Federal Reserve, which upped its key rate by 75bps, its biggest move in almost 30 years.

Have the interest rate hikes so far worked?

Off the cuff, they have worked, but there’s a long road to go until inflation is within the RBA’s target band of 2-3 per cent. Data published by the Australia Bureau of Statistics (ABS) will show how the economy was impacted by Australia’s first interest rate hikes in over a decade. An unexpected drop in housing approvals in April had many fearing construction companies will collapse over the coming months. However, mildly positive housing data has dispelled these concerns. Data released this week:

The value of new loan commitments:

- for total housing rose 1.7% to $32.4b, after a revised fall of of 2.8% in April

- for owner-occupier housing rose 2.1% to $21.2b, after a revised fall of 1.7% in April

- for investor housing rose 0.9% to $11.2b, after a fall of 4.8% in April

In May 2022 in seasonally adjusted terms for owner-occupier first home buyers, the number of new loan commitments:

- rose 2.3% at the national level but was 31.6% lower compared to a year ago

- in Victoria rose 8.6%, in New South Wales rose 1.9%

The May 2022 trend estimate for building approvals:

- Total dwellings approved fell 1.5%.

- Private sector houses approved fell 0.5%, while private sector dwellings excluding houses fell 2.5%.

- The value of non-residential building fell 1.5%.

Katherine Keenan, ABS head of finance and wealth, said: “The rise in May followed a revised fall of 2.8 per cent in April, when the proximity of Easter and ANZAC day public holidays reduced the processing of loan applications. Key lenders attributed the rise in May to a clearing of processing backlogs.”

The disappointing lending figures in April reflect households being hit with higher interest rates and rising costs. Given the backlog of work and rise in commodity prices, these weak figures look set to continue into the next financial year.

According to Bloomberg, “All but one of 26 economists surveyed by Bloomberg expect the Reserve Bank of Australia to raise its cash target rate by half a percentage point on Tuesday to 1.35% — a level not seen since May 2019. Market Economics is forecasting a larger 75-basis-point move.”

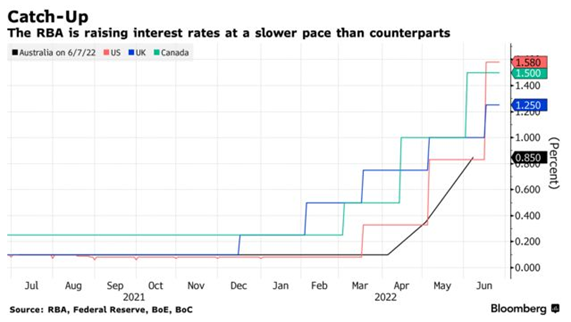

With Australia facing similar inflationary pressures as other global economies, the RBA is well behind the 8 ball, having only lifted its rates to 0.85 percent. Other developed economics are well above. United Kingdom at 1.25 percent, Canada at 1.50 percent, US at 1.75 percent and China on 3.70 percent.

Morgan Stanley are tipping the RBA to hike by 50bps tomorrow and August, followed by a 25bps raise through to November, which takes rates to 2.6 percent. That’s an equivalent standard variable mortgage rate of 6.4 per cent to 6.9 per cent. According to the AFR, “The median forecaster expects economic growth to slow to an annual rate of 3.2 per cent by the end of this year, from 3.3 per cent in the March quarter. GDP is then expected to fall to 2.5 per cent by mid-2023 before ending next year at 1.8 per cent.”

With Australia’s household debt-to-income ratio at a record high 187%, aggressive rate hikes by the RBA together with lower house prices could see a deceleration in growth over the next coming years.

Ishan is an experienced journalist covering The Insider Adviser publication.