Monday 1st July 2024

Super fund and limited license adviser losses prove a drag on numbers

The large advice provision models are holding up in terms of personnel, but super funds and tax advisers are repositioning their offerings as the cost to serve increases at a faster rate than revenue.

Adviser numbers took a significant fall in the past week, with 81 financial planners coming off the Australian Securities and Investments Commission’s registry, but the lion’s share of these losses came from outside holistic financial planning service divisions according to researcher Wealth Data.

Financial advisers at superannuation funds and those operating under a limited license are at the heart of the mini-exodus, Wealth Data managing director Colin Williams says, as both areas face evolving business challenges.

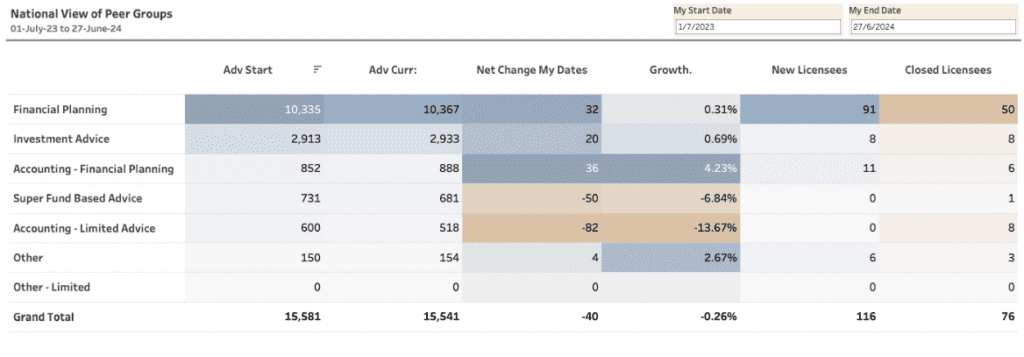

On the superannuation side, funds are repositioning their advice network to adjust for an increasing cost to serve. Advisers will need to pay between $6,000 and $8,000 combined for the Compensation Scheme of Last Resort and the ASIC Adviser Levy, this year, if estimates are accurate. The landscape for fund advice also faces regulatory uncertainty, with the government set to create a new class of advisers as part of the Delivering Better Financial Outcomes suite of reforms.

The country’s third biggest superannuation fund, the $265 billion Australian Retirement Trust (ART), shed 20 advisers who were marked as not ‘member facing’ and remained employed by the fund, suggesting they have been deployed into alternative service areas or placed in different roles. “The changes reflect the strategic repositioning of advice delivery at ART,” Williams said. “A lot of funds are repositioning their model.”

Financial Planners still providing SMSF tax advice under legacy limited license arrangements also declined markedly, which continues a trend that has seen around 80 per cent of advisers in this category disappear since 2017. Again, increased costs are a factor; accountants usually provide SMSF tax advice as only a small section of their wider service offering, with the attendant revenue slice not big enough to justify the high cost to serve.

Count Limited lost 11 advisers this week, Wealth Data reports, with 9 of those coming from Merit Wealth. “All the Merit Wealth advisers were restricted to SMSF Advice and could not offer broad based investment advice,” Williams said.

Williams said it was becoming increasingly difficult for advisers operating under a limited license to justify the practice form a business perspective. “It’s questionable whether the cost to income ratio makes sense any more.”

Apart from limited license advice and super fund providers, the larger advice provision models actually stayed relatively flat during the financial year (to June 27). While limited license advisers fell 13.67 per cent and fund advisers 6.84 per cent, straight financial planning groups and investment advice practices both increased personnel, albeit by less than one percentage point.

Total adviser numbers are down by 40 (0.26 per cent) for the financial year to June 27.