Monday 28th October 2024

'Still weak': Listed asset managers need to evolve rapidly to escape ETF obliteration

With traditional equity managers losing the fight against passive product providers, diversification into more specialist classes of asset management may provide a more sustainable path. But that's a pricey endeavour, and easier said than done.

There have been recent bright spots in the performance of Australian listed asset managers, but traditional, high-fee, fixed income and equity stock pickers will need to change the way they operate if they are to avoid being bullied out of the ecosystem by ETFs according to Morningstar.

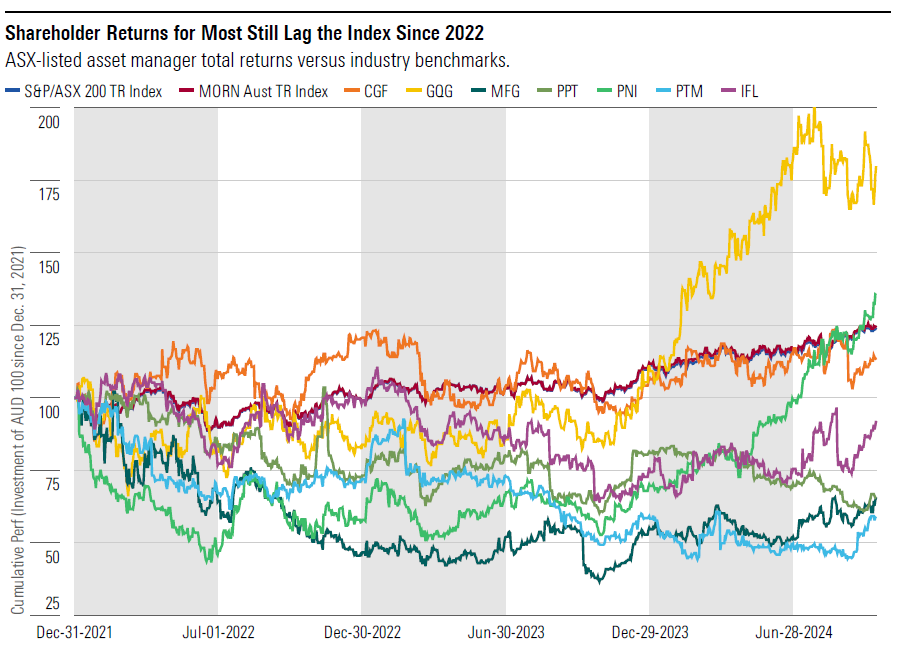

Money managers like GQG and more recently, Pinnacle, have managed to post encouraging shareholder return numbers, with both lifting cumulative shareholder returns significantly (at roughly 175 per cent and 140 per cent, respectively) from a negative start in 2023.

Others, however, including Challenger, Perpetual, Platinum and Insignia, have been less impressive, with structural and embedded challenges eating away at share prices. For listed equity managers, fee compression, wage inflation and the need to constantly invest in business development continue to make turning a healthy profit a problematic endeavour.

Some, like Perpetual and Platinum, have been further buffeted by the prospect of merger activity, which rarely bodes well in the funds management industry. The potential of consolidation and ‘synergies’ to arrest the misfortunes of flagging fund managers has been tried and tested, with sustainable success uncommon.

There are tailwinds for listed asset managers, of course, with Australia’s burgeoning superannuation coffers a honeypot for investment teams that have the scale to attract wholesale and institutional mandates. But this attraction is muted by the larger problem; the penchant of investors across the entire spectrum for low cost ETF investment products.

That problem is felt more keenly in the equities space than any other, where all but the savviest managers have been unable to match the market over the last decade. According to Morningstar, that trend will not abate.

“The shift toward low-cost exchange-traded funds is likely to continue, particularly in traditional asset classes like equities,” Morningstar said in its recent Australian Asset Managers: 2024 Q3 report. “Flows into ETFs have been rising in recent months, driven by prospects of falling interest rates in 2024-25.”

To combat the incursion, active managers – in particular listed teams that manage equities – need to “fight hard” to arrest outflows and win mandates to manage money, Morningstar explains. “Traditional active managers, including many of our covered firms, will need to win business by attracting off-platform cash or outperforming peers,” the report notes.

The bright side

The prospect of increased flows is brighter for those that ply their trade in other asset classes.

The rise of private capital, especially private equity and private debt, is a beacon for active management. There is a perceived validation in paying for the fees charged by providers of these investment due to the expertise and research involved, and they have significant non-correlative benefits to equites which means they traditionally pair well against equity ETFs.

It’s these kind of corners in the investment product universe that Morningstar believes traditional managers should move towards.

“We believe traditional active managers’ competitive position is weakening overall,” Morningstar says. “However, they can partially mitigate share losses to ETFs and industry funds by diversifying into more niche or exotic products that are harder to replicate through passive options. Recent business wins mainly reflect flows into nontraditional asset classes like private debt, private equity, and specialized fixed-income strategies. In contrast, flows into equities managed by traditional active managers remain weak and are likely to stay subdued in the long term.”

The sticking point is that the kind of expertise to diversify into specialised areas is expensive. A lot of resources need to be allocated before an initial mandate is won, and gaining trust from the market in a new area takes time. Branching out into private capital arms no easy transition for an equity manager, but it may be the only way out of a slow and inevitable decline.

“Flow prospects are greater in other categories, such as private debt, private equity, or systematic trend strategies, but it is difficult to build up such expertise,” Morningstar says.

Tahn is former managing editor across The Inside Network's three publications.