Thursday 16th June 2022

Hit to banks to come from higher rates

Following the Reserve Bank of Australia's decision to increase the cash rate by 50 basis point this month, the big banks have quickly raised interest rates on their mortgages, as well as interest rates on some savings accounts.

Following the Reserve Bank of Australia’s decision to increase the cash rate by 50 basis point this month, the big banks have quickly raised interest rates on their mortgages, as well as interest rates on some savings accounts. But with a slowdown in the property market, their profits could be hurt.

A slowing housing market means fewer mortgages will be written for the big banks, and therefore, their profits could suffer as the central bank is expected to keep raising interest rates this year, expert say.

Generally, a rising interest rate environment is positive for bank stocks because of better profitability resulting from wider interest rate margins, according to Diana Mousina, senior economist with AMP Australia. However, “the concern now is that a more aggressive RBA will hit the housing market more significantly in Australia which will be worse for banks than any increase in net interest margins,” she said.

Mousina has revised down economic growth forecasts based on more aggressive near-term RBA interest rate hikes. She now expects economic growth of 2.7 per cent over the year to December (down from 3.5 per cent and well below initial expectations earlier this year of 4.5 per cent) December 2023 year-on-year growth of just 2.4 per cent.

“We still see home prices falling by 10 per cent to 15 per cent peak to trough (reaching a bottom in late 2023). The risk is that the RBA decides it is behind the curve and hikes rates more than we expect and closer to market pricing of a 3.8 per cent cash rate in a year’s time, which would likely cause a recession,” she said.

Rise in bad debts seen

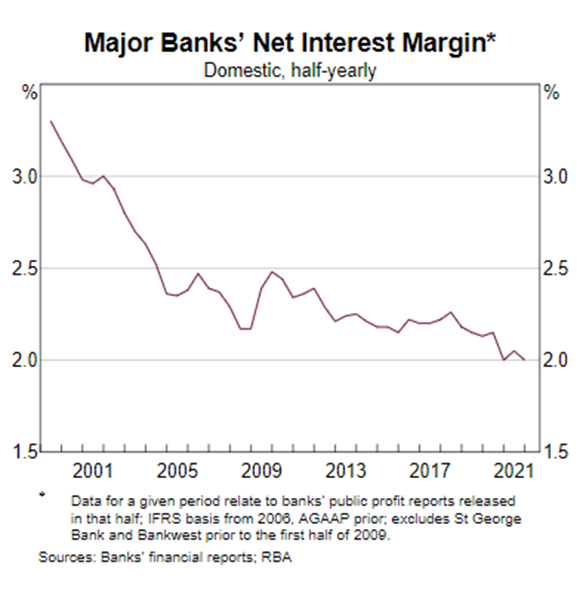

According to a recent Reserve Bank report, a sustained increase in official and market interest rates should see net interest margins (NIMs) increase from historical low levels of around 2 per cent, as lending rates rise, supporting profitability.

“However, rising interest rates could be a risk to the credit quality of banks’ assets if higher debt servicing costs are not matched by higher incomes. Rising interest rates could also lower demand for loans, capital market activity and investment-related advisory services (including mergers and acquisitions), which have been important sources of revenue for banks in recent times,” the RBA said in its recent Financial Stability Review.

According to stockbroking house Morgans, elevated household savings and buoyant employment conditions will go some way to cushioning the impact of higher interest rates on big banks’ profitability, but there will still be a hit. As monetary policy changes operate with a lag, Morgans expect to see higher interest rates eventually place downward pressure on asset prices and credit growth, and also increase the risk of bad loans, say Morgans bank analysts Azib Khan and Steven Sassine. Other headwinds include higher funding costs as existing loans are refinanced at higher interest rates and deposits potentially flow out from the banking system into other more attractive investments.

“From a dividend yield perspective, we expect downward pressure on valuations as we expect dividend yields to become less attractive relative to rising risk-free rates,” say Khan and Sassine.

Not all the big banks the same

However, Nathan Zaia, senior equity analyst with Morningstar, says big bank shares sold off sharply following the RBA’s surprising 50-basis point increase to the cash rate target and are now undervalued.

“The potential for larger-than-expected loan losses is real, but we think the market is now overemphasising the downside risk. Westpac and ANZ Bank now trade at 30 per cent discounts to our fair value estimates, National Australia Bank at a 7 per cent discount, and Commonwealth Bank 8 per cent overvalued,” he said.

“We have already assumed both slower credit growth and higher loan losses, in comparison to recent years, and while economic conditions have increased uncertainty around both in the short term, we do not believe the share price selloff is proportionate to those risks,” Zaia said.

In contrast, Morgans has downgraded its recommendations on Westpac and ANZ to ‘Hold’ from ‘Add’ and elevated National Australia Bank to its preferred big bank. It has a ‘Reduce’ call on the Commonwealth Bank.

“We continue to believe that Westpac’s stock offers compelling long-term value despite share price strength over the last five months. However, it has been disappointing to see that Westpac’s Australian investor home loan book has continued to shrink post FY21 according to APRA statistics,” say Khan and Sassine.

“We believe this contraction is being partially driven by Westpac’s business bankers being focused on remediation issues … We suspect the remediation issues are also hampering Westpac’s Australian business loan growth. This is of particular concern in the near term as investor and business lending are two relatively high-margin areas of lending. We expect Westpac’s share price to broadly track sideways until these issues are resolved,” they said.

“ANZ’s Australian home lending continues to disappoint in terms of growth. Moreover, it appears the limited growth ANZ is achieving is being driven by less complex, low-margin home loans. We consequently see risk of ANZ disappointing in the near term by way of loan growth and margin performance.

“Although we believe NAB is being priced for perfection at this point in time, good operational performance relative to peers will likely be supportive of relatively stretched valuation multiples in the near term. We remain mindful of the risk of an AUSTRAC-related civil penalty for NAB,” they said.

Nicki is an experienced journalist writing across three publications.